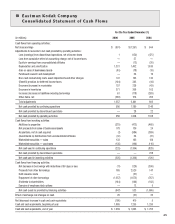

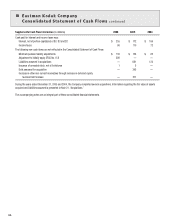

Kodak 2006 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2006 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

Goodwill

Goodwill represents the excess of purchase price of an acquisition over the fair value of net assets acquired. The Company applies the provisions of

SFAS No. 142, “Goodwill and Other Intangible Assets.” In accordance with SFAS No. 142, goodwill is not amortized, but is required to be assessed

for impairment at least annually. The Company has elected to make September 30 the annual impairment assessment date for all of its reporting

units, and will perform additional impairment tests when events or changes in circumstances occur that would more likely than not reduce the fair

value of the reporting unit below its carrying amount. SFAS No. 142 defines a reporting unit as an operating segment or one level below an operat-

ing segment. The Company estimates the fair value of its reporting units through internal analyses and external valuations, which utilize income and

market approaches through the application of discounted cash flow and market comparable methods. The assessment is required to be performed in

two steps, step one to test for a potential impairment of goodwill and, if potential losses are identified, step two to measure the impairment loss. The

Company completed step one in its fourth quarter and determined that there were no such impairments. Accordingly, the performance of step two was

not required.

Revenue

The Company’s revenue transactions include sales of the following: products; equipment; software; services; equipment bundled with products and/or

services and/or software; integrated solutions; and intellectual property licensing. The Company recognizes revenue when realized or realizable and

earned, which is when the following criteria are met: persuasive evidence of an arrangement exists; delivery has occurred; the sales price is fixed or

determinable; and collectibility is reasonably assured. At the time revenue is recognized, the Company provides for the estimated costs of customer

incentive programs, warranties and estimated returns and reduces revenue accordingly.

For product sales, the recognition criteria are generally met when title and risk of loss have transferred from the Company to the buyer, which may

be upon shipment or upon delivery to the customer site, based on contract terms or legal requirements in foreign jurisdictions. Service revenues are

recognized as such services are rendered.

For equipment sales, the recognition criteria are generally met when the equipment is delivered and installed at the customer site. Revenue is recog-

nized for equipment upon delivery as opposed to upon installation when there is objective and reliable evidence of fair value for the installation, and

the amount of revenue allocable to the equipment is not legally contingent upon the completion of the installation. In instances in which the agree-

ment with the customer contains a customer acceptance clause, revenue is deferred until customer acceptance is obtained, provided the customer

acceptance clause is considered to be substantive. For certain agreements, the Company does not consider these customer acceptance clauses to be

substantive because the Company can and does replicate the customer acceptance test environment and performs the agreed upon product testing

prior to shipment. In these instances, revenue is recognized upon installation of the equipment.

Revenue for the sale of software licenses is recognized when: (1) the Company enters into a legally binding arrangement with a customer for the

license of software; (2) the Company delivers the software; (3) customer payment is deemed fixed or determinable and free of contingencies or sig-

nificant uncertainties; and (4) collection from the customer is reasonably assured. If the Company determines that collection of a fee is not reasonably

assured, the fee is deferred and revenue is recognized at the time collection becomes reasonably assured, which is generally upon receipt of payment.

Software maintenance and support revenue is recognized ratably over the term of the related maintenance period.

The Company’s transactions may involve the sale of equipment, software, and related services under multiple element arrangements. The Company

allocates revenue to the various elements based on their fair value. Revenue allocated to an individual element is recognized when all other revenue

recognition criteria are met for that element.

Revenue from the sale of integrated solutions, which includes transactions that require significant production, modification or customization of

software, is recognized in accordance with contract accounting. Under contract accounting, revenue is recognized by utilizing either the percent-

age-of-completion or completed-contract method. The Company currently utilizes the completed-contract method for all solution sales, as sufficient

history does not currently exist to allow the Company to accurately estimate total costs to complete these transactions. Revenue from other long-term

contracts, primarily government contracts, is generally recognized using the percentage-of-completion method.

The timing and the amount of revenue recognized from the licensing of intellectual property depend upon a variety of factors, including the specific

terms of each agreement and the nature of the deliverables and obligations. When the Company has continuing obligations related to a licensing

arrangement, revenue related to the ongoing arrangement is recognized over the period of the obligation. Revenue is only recognized after all of the

following criteria are met: (1) the Company enters into a legally binding arrangement with a licensee of Kodak’s intellectual property, (2) the Company

delivers the technology or intellectual property rights, (3) licensee payment is deemed fixed or determinable and free of contingencies or significant

uncertainties, and (4) collection from the licensee is reasonably assured.

At the time revenue is recognized, the Company also records reductions to revenue for customer incentive programs in accordance with the provisions

of Emerging Issues Task Force (EITF) Issue No. 01-09, “Accounting for Consideration Given from a Vendor to a Customer (Including a Reseller of the

Vendor’s Products).” Such incentive programs include cash and volume discounts, price protection, promotional, cooperative and other advertising al-

lowances, and coupons. For those incentives that require the estimation of sales volumes or redemption rates, such as for volume rebates or coupons,

the Company uses historical experience and internal and customer data to estimate the sales incentive at the time revenue is recognized.