Kodak 2006 Annual Report Download - page 214

Download and view the complete annual report

Please find page 214 of the 2006 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

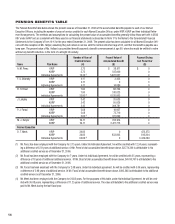

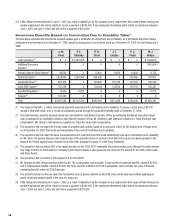

Retirement Plan (KRIP)

The Company funds a tax-qualified defined benefit pension plan for virtually all U.S. employees. Effective January 1, 2000, the Company amended

the plan to include a cash balance component. The cash balance portion of the plan covers all new employees hired after March 31, 1999, including

Messrs. Perez, Sklarsky, Brust, Langley and Faraci. Ms. Hellyar is the only Named Executive Officer who participates in the traditional defined benefit

portion of the plan. Prior to his termination of employment, Mr. Meek also participated in the traditional defined benefit portion of the plan.

Cash Balance Component

Under the cash balance component of the Company’s pension plan, the Company establishes a hypothetical account for each participating employee.

For every month the employee works, the Company credits the employee’s account with an amount equal to 4% of the employee’s monthly pay (i.e.,

base salary and EXCEL awards, including allowances in lieu of salary for authorized periods of absence, such as illness, vacation or holidays). In

addition, the ongoing balance of the employee’s account earns interest at the 30-year Treasury bond rate. Employees vest in their account balance

after completing five years of service. Benefits under the cash balance component are payable upon normal retirement (age 65), vested termination

or death. Participants in the cash balance component of the plan may choose from among optional forms of benefits such as a lump sum, a joint and

survivor annuity, and a straight life annuity. All optional forms of annuity benefits are actuarially equivalent to the lump-sum benefit.

Traditional Defined Benefit Component

Under the traditional defined benefit component of KRIP, benefits are based upon an employee’s average participating compensation (APC). The plan

defines APC as one-third of the sum of the employee’s participating compensation for the highest consecutive 39 periods of earnings over the 10 years

ending immediately prior to retirement or termination of employment. Participating compensation, in the case of the Named Executive Officers, is base

salary and any EXCEL award, including allowances in lieu of salary for authorized periods of absence, such as illness, vacation or holidays.

For an employee with up to 35 years of accrued service, the annual normal retirement income benefit is calculated by multiplying the employee’s years

of accrued service by the sum of 1) 1.3% of APC, plus 2) 1.6% of APC in excess of the average Social Security wage base. For an employee with more

than 35 years of accrued service, the amount is increased by 1% for each year in excess of 35 years.

The retirement income benefit is not subject to any deductions for Social Security benefits or other offsets. Participants in the traditional defined

benefit component of the plan may choose from among optional forms of benefits such as a straight life annuity, a qualified joint and 50% survivor

annuity, other forms of annuity, or a lump sum. The lump-sum benefit is actuarially equivalent to the participant’s normal retirement benefit.

An employee may be eligible for normal retirement, early retirement benefits, vested benefits or disability retirement benefits under the traditional

defined benefit component depending on the employee’s age and total service when employment with the Company ends. An employee is entitled

to normal retirement benefits at age 65. For early retirement benefits, an employee must have reached age 55 and have at least 10 years of service

or have a combined age and total service equal to 75. Generally, the benefit is reduced if payment begins before age 65. An employee who has five

or more years of vesting service with the Company will be entitled to a reduced vested benefit if employment with the Company is terminated before

becoming eligible for normal retirement or early retirement benefits.

In connection with his termination of employment, Mr. Meek received a lump-sum payment of his benefit under the traditional defined benefit compo-

nent of KRIP in 2006. As of December 31, 2006, Ms. Hellyar is the only Named Executive Officer eligible for an early retirement benefit under the plan.

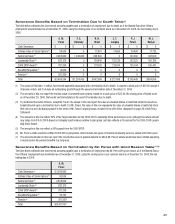

Unfunded Supplemental Retirement Plan (KURIP)

Each of our Named Executive Officers is entitled to receive benefits under the Kodak Unfunded Retirement Income Plan (KURIP). KURIP is an unfunded

non-contributory plan. It provides retirement benefits where benefits cannot be paid under KRIP and matching contributions cannot be made to the

Company’s Savings and Investment Plan (SIP)(a 401(k) defined contribution plan), because of the limitation on the inclusion of earnings in excess of

limits contained in Section 401(a)(17) of the Internal Revenue Code (for 2006 and 2007, $220,000 and $225,000, respectively) and because deferred

compensation is ignored when calculating benefits under KRIP and SIP.

For Named Executive Officers participating in the traditional defined benefit component of KRIP, the annual benefit is calculated by determining the

amount of the retirement benefit to which the employee would otherwise be entitled to under KRIP if deferred compensation were considered when

calculating such benefit and the limits under Section 401(a)(17) of the Internal Revenue Code were ignored, less any benefits earned under KRIP or

under the Company’s excess benefit plan (KERIP). The KERIP plan is further described in the CD&A. As of December 31, 2006, none of our Named

Executive Officers had any accrued benefit under the KERIP plan.

For Named Executive Officers participating in the cash balance component of KRIP, the annual benefit under KURIP is calculated by crediting an execu-

tive’s account with an amount equal to 7% of an employee’s compensation that is ignored under KRIP because it is either deferred compensation or in

excess of the Section 401(a)(17) compensation limit. The ongoing balance of the executive’s account earns interest at the 30-year Treasury bond rate.

Benefits due under KURIP are payable upon an employee’s termination of employment or death, as the plan administrator may determine. For benefits

not subject to Section 409A of the Internal Revenue Code, the plan administrator may select, in his sole discretion, the form of payment options