Kodak 2006 Annual Report Download - page 215

Download and view the complete annual report

Please find page 215 of the 2006 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

60

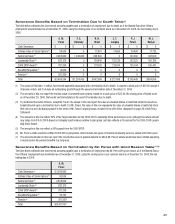

available under KURIP. For benefi ts subject to Section 409A of the Internal Revenue Code, participants elect the form of distribution. If an employee’s

benefi t under KRIP is subject to actuarial reduction, then any benefi t payable under KURIP will also be subject to actuarial reduction.

In connection with his termination of employment in 2006, Mr. Meek received a lump-sum payment of any amounts under KURIP that were not subject

to Section 409A of the Internal Revenue Code. He will be eligible to receive the remaining portion of his benefi t under KURIP that is subject to Section

409A in a lump-sum payment as soon as administratively practicable following the six-month anniversary of his termination of employment.

Individual Retirement Arrangements

Antonio M. Perez

Mr. Perez is eligible for a supplemental unfunded pension benefi t under the terms of his March 3, 2003 offer letter, as amended February 27, 2007.

Under this arrangement, because Mr. Perez has been employed for three years, he will be treated as if eligible for the traditional defi ned benefi t

component of the Company’s pension plan. For this purpose, he will be considered to have completed eight years of service with the Company and

attained age 65. If, instead, Mr. Perez actually remains employed until age 65, he will be considered to have completed 25 years of service with the

Company. Mr. Perez’s supplemental pension benefi t will be offset by his cash balance benefi t under KRIP, KERIP and KURIP, and any Company match-

ing contributions contributed to his account under SIP. The amended letter agreement also provides that if Mr. Perez is terminated before June 1, 2007,

he will receive his enhanced pension benefi t in a monthly annuity, with payments beginning the fi rst month following the six month anniversary of Mr.

Perez’s termination and continuing until the end of 2007, with the remainder paid in a lump sum on or after January 1, 2008. However, if Mr. Perez is

terminated after January 1, 2008, he will receive his enhanced pension benefi t in a lump sum following the six-month anniversary of his termination.

The amount of any supplemental benefi t will be payable to Mr. Perez in a lump sum as soon as practicable following the six-month anniversary of his

termination of employment.

Frank S. Sklarsky

In addition to the benefi t Mr. Sklarsky may be eligible for under the cash balance component, he is covered under a supplemental unfunded retirement

benefi t under the terms of his offer letter dated September 19, 2006, as amended. Under this arrangement, the Company established a phantom cash

balance account on behalf of Mr. Sklarsky. The Company agreed to credit the account by $100,000 each year for up to fi ve years, beginning October

30, 2007. Any amounts credited to this account will earn interest at the same interest rate that amounts accrue interest under the cash balance ben-

efi t. In order to receive any of the amounts credited to this account, Mr. Sklarsky must remain continuously employed for at least fi ve years unless his

employment terminates for a reason other than cause. Upon termination of employment, any vested amount will be payable in a lump sum within four

weeks after the six-month waiting period required for compliance under Section 409A of the Internal Revenue Code.

Robert H. Brust

While he was employed, Mr. Brust was covered under a supplemental unfunded pension arrangement established under his amended offer letter. This

arrangement provided Mr. Brust a single life annuity of $12,500 per month upon his retirement if he remained employed with the Company for at least

fi ve years. If Mr. Brust remained employed until January 3, 2006, he, in lieu of receiving the $12,500-per-month annuity, was to be treated as if he

was eligible for the traditional defi ned benefi t portion of the Company’s pension plan. For this purpose, Mr. Brust was credited with 14 years of extra

service in addition to his actual service. Since Mr. Brust remained employed until January 31, 2007, he was credited with a total of 18 years of extra

service in addition to his actual service for purposes of determining his benefi t under the traditional defi ned benefi t component of the plan. Mr. Brust’s

supplemental benefi t will be offset by his cash balance benefi t under KRIP, KERIP and KURIP. The amount of any supplemental benefi t will be payable

to Mr. Brust in a lump sum as soon as practicable following the six-month anniversary of his termination of employment.

James T. Langley

In addition to the benefi t Mr. Langley may be eligible for under the cash balance component, he is also eligible for a supplemental unfunded retire-

ment benefi t under the terms of his August 12, 2003 offer letter. Under this arrangement, the Company established a phantom cash balance account

on behalf of Mr. Langley. For each full year of service he remains employed (up to a maximum of six years), the Company will credit the account with

$100,000. The maximum the Company is obligated to credit to the account is $600,000. Any amounts credited to the account earn interest at the

same rate that amounts accrue interest under the cash balance component. In order to receive any of the amounts credited to this account, Mr. Lang-

ley must remain continuously employed for at least three years unless his employment terminates for certain specifi ed reasons. On February 28, 2007,

Mr. Langley’s letter agreement was amended to provide for a lump-sum payment of his enhanced pension benefi ts.

Philip J. Faraci

In addition to the benefi t Mr. Faraci may be eligible for under the cash balance component, he also is eligible for a supplemental unfunded retirement

benefi t under the terms of his November 3, 2004 offer letter. Under this arrangement, he is eligible to receive an extra 1.5 years of credited service for

each year he is employed, up to a maximum of 20 years of enhanced credited service. If Mr. Faraci remains employed for fi ve years, he will be treated

as if eligible for the traditional defi ned benefi t portion of the Company’s pension plan, and will be considered to have completed 12.5 years of service

with the Company. If, instead, he remains employed for 12 years, he will be considered to have completed 30 years’ total of service with the Company.

Mr. Faraci’s supplemental pension benefi t will be offset by his cash balance benefi t under KRIP, KERIP and KURIP, any Company matching contribu-

tions contributed to his account under SIP, and any retirement benefi ts provided to him pursuant to the retirement plan of any former employer.