IBM 2012 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2012 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

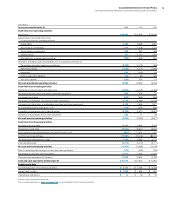

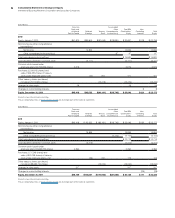

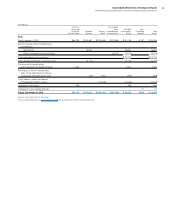

Notes to Consolidated Financial Statements

International Business Machines Corporation and Subsidiary Companies

83

Translation of Non-U.S. Currency Amounts

Assets and liabilities of non-U.S. subsidiaries that have a local func-

tional currency are translated to United States (U.S.) dollars at

year-end exchange rates. Translation adjustments are recorded

in OCI. Income and expense items are translated at weighted-aver-

age rates of exchange prevailing during the year.

Inventories, property, plant and equipment—net and other non-

monetary assets and liabilities of non-U.S. subsidiaries and

branches that operate in U.S. dollars are translated at the approxi-

mate exchange rates prevailing when the company acquired the

assets or liabilities. All other assets and liabilities denominated in a

currency other than U.S. dollars are translated at year-end exchange

rates with the transaction gain or loss recognized in other (income)

and expense. Income and expense items are translated at the

weighted-average rates of exchange prevailing during the year.

These translation gains and losses are included in net income for

the period in which exchange rates change.

Derivative Financial Instruments

All derivatives are recognized in the Consolidated Statement of

Financial Position at fair value and are reported in prepaid expenses

and other current assets, investments and sundry assets, other

accrued expenses and liabilities or other liabilities. Classification

of each derivative as current or noncurrent is based upon whether

the maturity of the instrument is less than or greater than 12 months.

To qualify for hedge accounting, the company requires that the

instruments be effective in reducing the risk exposure that they are

designated to hedge. For instruments that hedge cash flows, hedge

designation criteria also require that it be probable that the under-

lying transaction will occur. Instruments that meet established

accounting criteria are formally designated as hedges. These criteria

demonstrate that the derivative is expected to be highly effective

at offsetting changes in fair value or cash flows of the underlying

exposure both at inception of the hedging relationship and on an

ongoing basis. The method of assessing hedge effectiveness and

measuring hedge ineffectiveness is formally documented at hedge

inception. The company assesses hedge effectiveness and measures

hedge ineffectiveness at least quarterly throughout the designated

hedge period.

Where the company applies hedge accounting, the company

designates each derivative as a hedge of: (1) the fair value of a rec-

ognized financial asset or liability, or of an unrecognized firm

commitment (fair value hedge attributable to interest rate or foreign

currency risk); (2) the variability of anticipated cash flows of a

forecasted transaction, or the cash flows to be received or paid

related to a recognized financial asset or liability (cash flow hedge

attributable to interest rate or foreign currency risk); or (3) a hedge

of a long-term investment (net investment hedge) in a foreign opera-

tion. In addition, the company may enter into derivative contracts

that economically hedge certain of its risks, even though hedge

accounting does not apply or the company elects not to apply

hedge accounting. In these cases, there exists a natural hedging

relationship in which changes in the fair value of the derivative, which

are recognized currently in net income, act as an economic offset

to changes in the fair value of the underlying hedged item(s).

Changes in the fair value of a derivative that is designated as a fair

value hedge, along with offsetting changes in the fair value of the

underlying hedged exposure, are recorded in earnings each period.

For hedges of interest rate risk, the fair value adjustments are recorded

as adjustments to interest expense and cost of financing in the

Consolidated Statement of Earnings. For hedges of currency risk

associated with recorded financial assets or liabilities, derivative fair

value adjustments are recognized in other (income) and expense in

the Consolidated Statement of Earnings. Changes in the fair value of

a derivative that is designated as a cash flow hedge are recorded, net

of applicable taxes, in OCI, in the Consolidated Statement of Com-

prehensive Income. When net income is affected by the variability of

the underlying cash flow, the applicable offsetting amount of the gain

or loss from the derivative that is deferred in AOCI is released to net

income and reported in interest expense, cost, SG&A expense or

other (income) and expense in the Consolidated Statement of Earn-

ings based on the nature of the underlying cash flow hedged.

Effectiveness for net investment hedging derivatives is measured on

a spot-to-spot basis. The effective portion of changes in the fair value

of net investment hedging derivatives and other non-derivative finan-

cial instruments designated as net investment hedges are recorded

as foreign currency translation adjustments in OCI. Changes in the

fair value of the portion of a net investment hedging derivative

excluded from the effectiveness assessment are recorded in interest

expense. If the underlying hedged item in a fair value hedge ceases

to exist, all changes in the fair value of the derivative are included in

net income each period until the instrument matures. When the

derivative transaction ceases to exist, a hedged asset or liability is no

longer adjusted for changes in its fair value except as required under

other relevant accounting standards. Derivatives that are not desig-

nated as hedges, as well as changes in the fair value of derivatives

that do not effectively offset changes in the fair value of the underlying

hedged item throughout the designated hedge period (collectively,

“ineffectiveness”), are recorded in net income each period and are

reported in other (income) and expense. When a cash flow hedging

relationship is discontinued, the net gain or loss in AOCI must gener-

ally remain in AOCI until the item that was hedged affects earnings.

However, when it is probable that a forecasted transaction will not

occur by the end of the originally specified time period or within an

additional two-month period thereafter, the net gain or loss in AOCI

must be reclassified into earnings immediately. The company reports

cash flows arising from derivative financial instruments designated as

fair value or cash flow hedges consistent with the classification of cash

flows from the underlying hedged items that these derivatives are

hedging. Accordingly, the cash flows associated with derivatives des-

ignated as fair value or cash flow hedges are classified in cash flows

from operating activities in the Consolidated Statement of Cash Flows.

Cash flows from derivatives designated as net investment hedges

and derivatives that do not qualify as hedges are reported in cash

flows from investing activities. For currency swaps designated as

hedges of foreign currency denominated debt (included in the com-

pany’s debt risk management program as addressed in note D,

“Financial Instruments,” on pages 94 to 98), cash flows directly asso-

ciated with the settlement of the principal element of these swaps

are reported in payments to settle debt in cash flows from financing

activities in the Consolidated Statement of Cash Flows.