IBM 2005 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2005 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

|

|

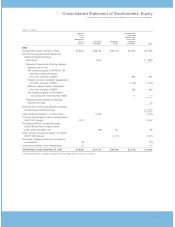

NotestoConsolidatedFinancialStatements

INTERNATIONALBUSINESSMACHINESCORPORATION ANDSUBSIDIARYCOMPANIES

_63

toapplytheguidanceofFIN46toallofitsinterestsinspecial-pur-

pose entities(SPEs)asdefinedwithinFIN46(R)andallnon-SPE

VIEs that were created after January 31, 2003. Also in accor-

dance with the transition provisionsof FIN 46(R),thecompany

adoptedFIN 46(R)forallVIEsandSPEsas ofMarch31,2004.

Theseaccountingpronouncementsdidnothaveamaterialeffect

onthecompany’sConsolidatedFinancialStatements.

In 2003, the Emerging Issues Task Force (EITF) reached

a consensus on two revenue recognition issues relating to

the accounting for multiple-element arrangements: Issue No.

00-21, “Accounting for Revenue Arrangements with Multiple

Deliverables (EITF No. 00-21)” and Issue No. 03-05,

“ApplicabilityofAICPASOP97-2toNon-SoftwareDeliverables

in an Arrangement Containing More Than Incidental Software

(EITF No. 03-05).” The consensus opinion in EITF No. 03-05

clarifiesthe scope ofbothEITF No. 00-21 and SOP97-2and

wasreachedonJuly31,2003.Thetransitionprovisionsallowed

either prospective application or a cumulative effect adjust-

ment upon adoption. The company adopted the issues

prospectivelyasofJuly1,2003.EITFNo.00-21 andNo.03-05

didnothaveamaterialeffectonthecompany’sConsolidated

FinancialStatements.

InMay2003,theFASBissuedSFASNo.150,“Accountingfor

Certain Financial Instruments with Characteristics of both

LiabilitiesandEquity.” Itestablishesclassificationandmeasure-

ment standards for three types of freestanding financial instru-

ments that have characteristics of both liabilities and equity.

InstrumentswithinthescopeofSFASNo.150mustbeclassified

as liabilities within the company’s Consolidated Financial

Statementsandbereportedatsettlementdatevalue.Theprovi-

sionsofSFASNo.150areeffectivefor(1)instrumentsenteredinto

ormodifiedafterMay31,2003,and(2)pre-existinginstrumentsas

ofJuly1,2003.InNovember2003,throughtheissuanceofFSP

No.FAS150-3,theFASBindefinitelydeferredtheeffectivedateof

certain provisions of SFAS No. 150, including mandatorily

redeemableinstrumentsastheyrelatetominorityinterestsincon-

solidated finite-lived entities. The adoption of SFAS No. 150, as

modifiedbyFSPNo.FAS150-3,didnothaveamaterialeffecton

the company’s ConsolidatedFinancialStatements.

InApril2003,theFASBissuedSFASNo.149,“Amendment

of Statement 133 on Derivative Instruments and Hedging

Activities.” SFAS No.149 clarifies under what circumstances a

contractwithaninitialnetinvestmentmeetsthecharacteristicsof

aderivativeasdiscussedinSFASNo.133.Italsospecifieswhen

aderivativecontainsafinancingcomponentthatrequiresspecial

reportingintheConsolidatedStatementofCashFlows.SFASNo.

149 amends certain other existing pronouncements in order to

improveconsistencyinreportingthesetypesoftransactions.The

newguidancewaseffectiveforcontractsenteredintoormodified

after June 30, 2003, and for hedging relationships designated

afterJune30,2003.SFASNo.149didnothaveamaterialeffect

onthecompany’sConsolidatedFinancialStatements.

InNovember 2002,the FASBissued InterpretationNo. 45

(FIN45),“Guarantor’sAccountingandDisclosureRequirements

forGuarantees,IncludingIndirectGuaranteesofIndebtedness

ofOthers,” whichaddressesthe disclosurestobe madebya

guarantorinits interim and annualfinancialstatementsabout

its obligations under guarantees. FIN 45 also requires the

recognitionofaliabilitybyaguarantorattheinceptionofcer-

tain guarantees that are entered into or modified after

December 31, 2002. The company adopted the disclosure

requirements of FIN 45 (see note A, “Significant Accounting

Policies,” onpage 57 under“ProductWarranties,” andnote O,

“Contingencies and Commitments,” on page 78) and applied

the recognition and measurement provisions for all material

guarantees entered into or modified in periods beginning

January1,2003.Theadoptionoftherecognitionandmeasure-

mentprovisionsofFIN45didnothaveamaterialeffectonthe

company’sConsolidatedFinancialStatements.

InJuly2002,theFASB issued SFASNo.146,“Accounting

forCostsAssociatedwithExitorDisposalActivities.” SFASNo.

146supersedesEITFNo.94-3,“LiabilityRecognitionforCertain

Employee Termination Benefits and Other Costs to Exit an

Activity (Including Certain Costs Incurred in a Restructuring),”

andrequiresthataliabilityforacostassociatedwithanexitor

disposalactivityberecognizedwhentheliabilityisincurred.The

companyadoptedthisstatementeffectiveJanuary1,2003,and

itsadoptiondidnothaveamaterialeffectontheConsolidated

FinancialStatements.

OnJanuary1, 2003,the companyadoptedSFAS No.143,

“Accounting for Asset Retirement Obligations,” which was

issued in June 2001. SFAS No. 143 provides accounting and

reporting guidance for legal obligations associated with the

retirement of long-lived assets that result from the acquisition,

constructionornormaloperationofalong-livedasset.SFASNo.

143requirestherecordingofanassetandaliabilityequaltothe

presentvalueoftheestimatedcostsassociatedwiththeretire-

mentoflong-livedassetsforwhichalegalobligationexists.The

assetis requiredto bedepreciatedover the life ofthe related

equipmentorfacility,andtheliabilityisrequiredtobeaccreted

each year using a risk-adjusted interest rate. The adoption of

thisstatementdidnothaveamaterialeffectonthecompany’s

ConsolidatedFinancialStatements.

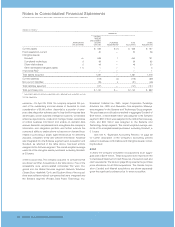

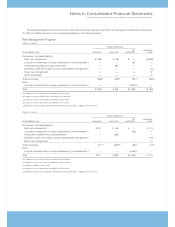

C.Acquisitions/Divestitures

Acquisitions

2005

In2005,thecompany completed16acquisitions at anaggre-

gate cost of $2,022 million, which was paid in cash. These

acquisitionsarereportedintheConsolidatedStatementofCash

Flowsnetofacquiredcashandcashequivalents.Thetable on

page64 representsthepurchasepriceallocationsforallofthe

2005acquisitions.TheAscentialCorporation(Ascential)acqui-

sitionisshownseparatelygivenitssignificantpurchaseprice.