IBM 2005 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2005 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

|

|

ManagementDiscussion

INTERNATIONALBUSINESSMACHINESCORPORATION ANDSUBSIDIARYCOMPANIES

28_ ManagementDiscussion

growthrateduetotheimpactof highlevelsofbacklog erosion

experiencedin2004andthecumulativeeffectoflowersignings,

starting in 2004 through the first quarter of 2005. SO revenue

growthwasdrivenbytheAmericas (2 percent)andEMEA(6per-

cent),withadecline yeartoyearinAsiaPacific (2percent).

BCSrevenueincreasedin2005versus2004ledbygrowth

intheAmericas (7percent)andEMEA(5percent),partiallyoff-

setby declinesinAsiaPacific (6percent).BCS signingswere

up 19 percent over last year, with Consulting and Systems

Integration up 3 percent and Business Transformation

Outsourcing up 126 percent. The company’s Consulting and

Systems Integration business had many areas of growth, with

strong performance in the Strategy and Change and Supply

ChainManagementpractices.Thisoverallgrowthwasmitigated

by weakness year to year in Japan, Germany, and the com-

pany’s Federal Business in the U.S. However, across all prac-

tices, the company drove improved resource utilization and

pricing trends remained stable to improving. The company is

takingactionstoimproveitsgrowthinConsultingandSystems

Integration. The company is increasing the level of dedicated

sales resources to drive its Business and Web Services and

SystemOrientedArchitecture(SOA) solutions,furtherinvesting

in resources to address mid-market opportunities, increasing

the level of brand resources in Asia Pacific and leveraging its

globalend-to-enddesign,build,andruncapabilities.

Thecompany’s BTO businesscontinueditsstrongyear-to-

yeargrowth.BTOisanimportantofferingtoaddressthe BPTS

opportunity. Other elements include the Strategy and Change

practice,E&TS,andBusinessPerformanceSoftware.Fortheyear,

BPTSrevenuewas$4billion,up28percentyeartoyear.

ITSsigningsweredown7percentin2005versus2004. The

ITS business is more dependent upon short-term signings for

revenue growth and signings declines in the third and fourth

quarterimpactedtheoverallrevenuegrowthratefor2005. The

companybegantorebalanceitsITS offerings portfolio andshift

itsbusinessdevelopmentanddeliverycapabilitiesandskillsto

highergrowthareasinthethirdquarterof2005.Theinitialport-

folio rebalancing work is completed. The company is adding

businessdevelopmentskillsandthesalescoveragemodelhas

beenalignedtotherevisedportfolio.

year. Inaddition,sinceGlobalServicesisprimarilyaresource-

based business, the resulting Global Services margins were

impacted more by pension expense increases, partially miti-

gatedbylower stock-based compensationexpense.

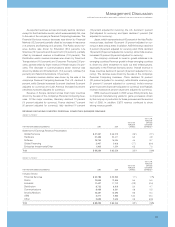

GLOBALSERVICESSIGNINGS

(Dollarsinmillions)

FORTHEYEARENDEDDECEMBER31: 2005 2004 2003

Longer-term* $«27,180 $«22,857 $«34,608

Shorter-term* 19,901 20,146 20,854

Total $«47,081 $«43,003 $«55,462

* Longer-termsigningsincludeSOandBTOcontracts,aswellastheU.S.federal

governmentcontractswithinBCS.Shorter-termsigningsincludeITSandallother

BCScontracts.Theseamountshavebeenadjustedtoexcludetheimpactofyear-

to-yearcurrencychanges.

In2005,totalGlobalServicessigningsincreased9percentyear

toyear,drivenbya19percentincreaseinlonger-termsignings,

whileshorter-termsigningswereessentiallyflat.

GlobalServicessigningsaremanagement’sinitialestimateof

the value of a client’s commitment under a Global Services

contract. Signings are used by management to assess period

performanceofGlobalServicesmanagement.Therearenothird-

party standards or requirements governing the calculation of

signings. The calculation used by management involves esti-

mates and judgments to gauge the extent of a client’s commit-

ment, including the type and duration of the agreement, and

the presence of termination charges or wind-down costs. For

example,forlonger-termcontractsthatrequiresignificantup-front

investmentbythecompany,the portionsofthese contractsthat

are counted as a signing are those periods in which there is a

significanteconomicimpactontheclientifthecommitmentisnot

achieved,usuallythroughaterminationchargeorthe client incur-

ringsignificantwind-downcostsasaresultofthetermination.For

shorter-term contracts that do not require significant up-front

investments,asigningisusuallyequaltothefullcontractvalue.

Signings includes SO, BCS and ITS contracts. Contract

extensionsandincreasesinscopearetreatedassigningsonly

totheextentoftheincrementalnewvalue.Maintenanceisnot

includedinsigningsasmaintenancecontractstendtobemore

steady-state, where revenues equal renewals, and therefore,

the company does not think they are as useful a predictor of

futureperformance.

BacklogincludesSO,BCS,ITS,andMaintenance.Backlog

isintendedtobeastatementofoverallworkundercontractand

therefore does include Maintenance. Backlog estimates are

subjecttochangeandareaffectedbyseveralfactors,including

terminations,changesin the scopeofcontracts,periodicreval-

idations,adjustmentsforrevenuenotmaterializedandcurrency

assumptionsusedtoapproximateconstantcurrency.

Contractportfoliospurchasedinanacquisitionaretreated

aspositivebacklogadjustmentsprovidedthosecontractsmeet

thecompany’s requirementsfor initialsignings.A new signing

willberecognizedif a new services agreementissignedinci-

dentalorcoincidenttoanacquisition.

(Dollarsinmillions)

YR. TOYR.

FORTHEYEARENDEDDECEMBER31: 2005 2004 CHANGE

GlobalServices:

Grossprofit $«12,287 $«11,175 9.9%

Grossprofitmargin 25.9% 24.2% 1.7 pts.

GlobalServices grossprofitdollarsincreasedprimarilydue to

the corresponding increase in revenue and improved gross

profit margins across all categories of Global Services. The

grossprofitmarginimprovementwas primarily duetobenefits

fromthesecond-quarter2005 restructuringand productivityini-

tiatives (see note R, “2005 Actions,” on pages 80 and 81 for

additional information), improved utilization levels, primarily

withinBCS,andabetter overall contractprofileversustheprior