IBM 2005 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2005 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

|

|

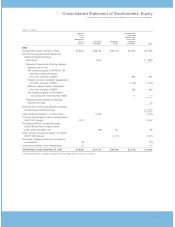

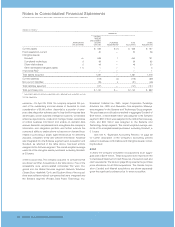

NotestoConsolidatedFinancialStatements

INTERNATIONALBUSINESSMACHINESCORPORATION ANDSUBSIDIARYCOMPANIES

_55

56) on whether and/or how to separate multiple-deliverable

arrangements into separate units of accounting (separability)

and how to allocate the arrangement consideration among

thoseseparateunitsofaccounting(allocation),thatdeliverable

isaccountedforinaccordancewithsuchspecificguidance.For

all other deliverables in multiple-element arrangements, the

guidancebelowisappliedforseparabilityandallocation.Amul-

tiple-elementarrangementisseparatedintomorethanoneunit

ofaccountingifallofthefollowingcriteriaaremet:

• The delivered item(s) has value to the client on a stand-

alonebasis.

• Thereisobjectiveandreliableevidenceof thefairvalueof

theundelivereditem(s).

• Ifthearrangementincludesageneralrightofreturnrelative

tothedelivereditem(s),deliveryorperformanceoftheunde-

livered item(s) is considered probable and substantially in

thecontrolofthecompany.

Ifthesecriteriaarenotmet, thearrangementisaccountedforas

oneunitofaccountingwhich would resultinrevenuebeingrec-

ognizedonastraight-linebasisor beingdeferreduntiltheearlier

ofwhensuchcriteriaaremet orwhenthelastundeliveredele-

mentisdelivered.If thesecriteriaaremetforeachelementand

thereisobjectiveandreliableevidenceoffairvalueforallunitsof

accountinginanarrangement,thearrangementconsiderationis

allocated to the separate units of accounting based on each

unit’srelativefairvalue.Theremaybecases,however,inwhich

thereisobjectiveandreliableevidenceoffairvalueoftheunde-

livereditem(s)butnosuchevidenceforthedelivereditem(s).In

thosecases,theresidualmethodisusedtoallocatethearrange-

ment consideration. Under the residual method, the amount of

considerationallocatedtothedelivereditem(s)equalsthetotal

arrangement consideration less the aggregate fair value of the

undelivered item(s). The revenue policies described below are

thenappliedtoeachunitofaccounting,asapplicable.

Iftheallocationofconsiderationinaprofitablearrangement

results in a loss on an element, that loss is recognized at the

earlierof(a)delivery ofthatelement,(b)whenthe first dollar of

revenueisrecognizedonthatelement,or(c)whenthereareno

remainingprofitableelementsinthearrangementtobedelivered.

SERVICES

The company’s primary services offerings include information

technology (IT) datacenter and business process transforma-

tionoutsourcing,applicationmanagementservices,technology

infrastructure and system maintenance, Web hosting, and the

design and development of complex IT systems to a client’s

specifications(DesignandBuild).Theseservicesareprovided

onatime-and-materialbasis,asafixed-price contract or asa

fixed-price per measure of output contract, and the contract

termsrangefromlessthanoneyeartotenyears.

Revenue from IT datacenter and business process out-

sourcingcontractsisrecognizedintheperiodtheservicesare

provided using either an objective measure of output or a

straight-linebasisoverthetermofthecontract.Undertheoutput

method, the amount of revenue recognized is based on the

servicesdeliveredintheperiodasstatedinthecontract.

Revenue from application management services, technol-

ogy infrastructure and system maintenance, and Web hosting

contractsisrecognizedonastraight-linebasisoverthetermof

thecontract.Revenuefromtime-and-materialcontractsisrec-

ognized at the contractual rates as labor hours are delivered

anddirectexpensesareincurred.Revenuerelatedtoextended

warrantyandproductmaintenancecontractsis recognizedona

straight-linebasisoverthedeliveryperiod.

Revenuefromfixed-priceDesignandBuildcontractsisrec-

ognized in accordance with SOP No. 81-1, “Accounting for

PerformanceofConstruction-TypeandCertainProduction-Type

Contracts,” underthepercentage-of-completion(POC)method.

Under the POC method, revenue is recognized based on the

costs incurred to date as a percentage of the total estimated

costs to fulfill the contract. If circumstances arise that change

theoriginalestimatesofrevenues,costs,orextentofprogress

toward completion, then revisions to the estimates are made.

These revisions may result in increases or decreases in esti-

mated revenues or costs, and such revisions are reflected in

incomeintheperiodinwhichthecircumstancesthatgiveriseto

the revision become known by management. While the com-

panyusesthePOCmethodasitsbasicaccountingpolicyunder

SOP81-1,thecompanyusesthecompleted-contractmethodif

reasonableestimatesforacontractorgroupofcontractscannot

bedeveloped.

Thecompanyperformsongoingprofitabilityanalysesofits

servicescontractsinordertodeterminewhetherthelatestesti-

mates-revenue, costs, profits-require updating. If, at any time,

these estimates indicate that the contract will be unprofitable,

the entire estimated loss for the remainder of the contract is

recordedimmediately.

Insomeofthecompany’sservicescontracts,thecompany

billstheclientpriortoperformingtheservices.Deferredincome

of$4.3 billionand$3.9billionatDecember31,2005and2004,

respectively, is included in the Consolidated Statement of

FinancialPosition.Inotherservicescontracts,thecompanyper-

formstheservicespriortobillingtheclient.Unbilled accounts

receivableof$1.7 billionand$1.9billionatDecember31,2005

and 2004, respectively, are included in Notes and accounts

receivable-trade in the Consolidated Statement of Financial

Position.Billingsusuallyoccurinthemonth afterthecompany

performstheservicesorinaccordancewithspecificcontractual

provisions.Unbilledreceivablesareexpectedtobebilledand

collectedwithinfourmonths,rarelyexceedingninemonths.

HARDWARE

Revenuefromhardwaresales and sales-typeleasesis recog-

nizedwhenriskoflosshastransferredtotheclientandthereare

no unfulfilled company obligations that affect the client’s final

acceptance of the arrangement. Any cost of warranties and

remaining obligations that are inconsequential or perfunctory

are accrued when the corresponding revenue is recognized.

Revenuefromrentalsandoperatingleasesisrecognizedona

straight-linebasisoverthetermoftherentalorlease.