Holiday Inn 2013 Annual Report Download - page 144

Download and view the complete annual report

Please find page 144 of the 2013 Holiday Inn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

|

|

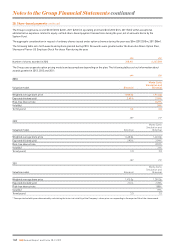

26. Retirement benefits

UK

UK retirement and death in service benefits are provided for eligible Group employees in the UK principally by the InterContinental Hotels UK

Pension Plan, which is HM Revenue & Customs registered. The defined benefit section of the plan, which provides benefits based on final salary

and is funded, closed to new entrants in 2002 and closed to future accrual for current members with effect from 1 July 2013. New members,

including those who have been auto-enrolled since 1 September 2013, are provided with defined contribution arrangements as are members

of the defined benefit section since 1 July 2013. The assets of the plan are held in a self-administered trust fund which is governed by a

Trustee Board who are responsible for the administration and investment strategy of the plan. The Trustee Board comprises a combination of

independent, company nominated and member nominated trustees, and is assisted by professional advisers as and when required. As required

by the Pensions Act 2004, the plan is required to meet a Statutory Funding Objective in respect of its defined benefit obligations and a formal

recovery plan is required to meet a funding shortfall. The overall operation of the plan is subject to the oversight of The Pensions Regulator.

On 15 August 2013, the Trustee Board completed a buy-in transaction whereby the assets of the plan were invested in a bulk purchase annuity

policy with the insurer Rothesay Life, under which the benefits payable to defined benefit members are now fully insured. The insurance policy

was purchased using the existing assets of the plan and a final company contribution of £5m. It is the intention of the Trustee Board that the

plan will move to a full buy-out as soon as practical, following which the insurance company will become directly responsible for pension

payments. Under the most recent recovery plan, the company agreed to make additional contributions of £130m by 31 July 2014; inaddition to

the £5m referred to above, £55m was paid in 2012 and a further amount of £60m was paid into a funding trust (the IHG Funding Trust) during

the year. £30m of the funding trust payments occurred on the sale of the InterContinental London Park Lane in May 2013, over which there was

previously a charge for the same amount in favour of the pension plan. As the buy-in transaction has resulted in the defined benefit obligations

being fully insured, the company has no further contributions to make and £57m has been returned to the company from the funding trust. It is

expected that the remaining £3m held in the funding trust will be returned to the company on completion of the planned buy-out.

In addition to the above, additional benefits are provided to certain members of the defined benefit section of the plan who are affected by

lifetime or annual allowances through an unfunded pension arrangement. The unfunded pension arrangement also held a charge over the

InterContinental London Park Lane which, on sale of the hotel, was replaced with a charge over certain ring-fenced bank accounts

totalling £31m (see note 15).

US and other

The Group also maintains the following US-based defined benefit plans; the funded Inter-Continental Hotels Pension Plan, unfunded

Inter-Continental Hotels Non-qualified Pension Plans and unfunded Inter-Continental Hotels Corporation Postretirement Medical,

Dental, Vision and Death Benefit Plan. All plans are closed to new members. In respect of the funded plan, an Investment Committee has

responsibility for the oversight and management of the Plan’s assets, which are held in a separate trust. The Committee comprises senior

company employees and is assisted by professional advisers as and when required. The company currently makes contributions that equal

or exceed the minimum funding amounts required by the Employee Retirement Income and Security Act of 1974 (‘ERISA’). The investment

objective is to achieve full funding over time by following a specified ‘glide path approach’ which results in a progressive switching from

return seeking assets to liability-matching assets as the funded status of the plan increases. During the year, the funded status reached

80% which triggered a further de-risking of the investment portfolio.

The Group also operates a number of smaller pension schemes outside the UK, themost significant of which is a defined contribution

scheme in the US; there is no material difference between the pension costs of, and contributions to, these schemes.

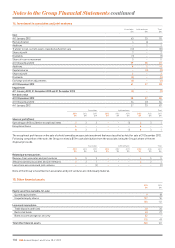

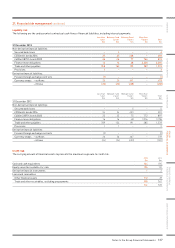

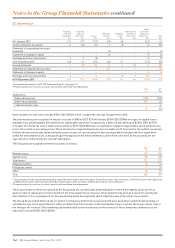

In respect of the defined benefit plans, the amounts recognised in the Group income statement, in administrative expenses, are:

Pension plans

UK

US and

other

Post-employment

benefits Total

2013

$m

2012

(restated1)

$m

2011

(restated1)

$m

2013

$m

2012

(restated1)

$m

2011

(restated1)

$m

2013

$m

2012

$m

2011

$m

2013

$m

2012

(restated1)

$m

2011

(restated1)

$m

Current service cost 25 6 11 1 –– – 36 7

Past service cost –– – 1– – –– – 1– –

Net interest expense –1 6 33 3 11 1 4510

Administration costs 11 1 11 1 –– – 22 2

Operating profit before exceptional items 3713 65 5 11 1 10 13 19

Exceptional items:

Settlement loss 147 – – –– – –– – 147 – –

Past service gain ––(28) –– – –– – ––(28)

150 7(15) 65 5 11 1 157 13 (9)

1 Restated for the adoption of IAS 19R ‘Employee Benefits’ (see page 111).

The settlement loss results from the buy-in transaction described above and comprises a past service cost of $5m relating to additional

benefits secured by the transaction, the difference between the cost of the insurance policy and the accounting value of the liabilities secured

of $137m and transaction costs of $5m. As the policy has been structured to enable the planto move to a buy-out and the intention is to

proceed on this basis, the buy-in transaction has been accounted for as a settlement with the loss arising recorded in the income statement.

The past service gain in 2011 arose in respect of the UK pension plan and from the decision to close the defined benefit section to future

accrual with effect from 1 July 2013. The plan rules were formally amended to reflect this change in September 2011.

142 IHG Annual Report and Form 20-F 2013

Notes to the Group Financial Statements continued