Holiday Inn 2013 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2013 Holiday Inn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

|

|

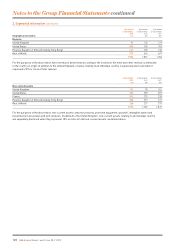

Documentation outlining the measurement and effectiveness of

any hedging arrangements is maintained throughout the life of the

hedge relationship.

Interest arising from currency derivatives and interest rate swaps

isrecorded in either financial income or expenses over the term of

the agreement, unless the accounting treatment for the hedging

relationship requires the interest to be taken to reserves.

Self insurance

Liabilities in respect of self insured risks include projected settlements

for known and incurred but not reported claims. Projected settlements

are estimated based on historical trends and actuarial data.

Provisions

Provisions are recognised when the Group has a present obligationas

a result of a past event, it is probable that a payment will be made and

a reliable estimate of the amount payable can bemade. If the effect of

the time value of money is material, theprovision is discounted.

An onerous contract provision is recognised when the unavoidable

costs of meeting the obligations under a contract exceed the

economic benefits expected to be received under it.

In respect of litigation, provision is made when management consider

it probable that payment may occur even though the defence of the

related claim may still be ongoing through the court process.

Taxes

Current tax

Current income tax assets and liabilities for the current and prior

periods are measured at the amount expected to be recovered

from or paid to the tax authorities including interest. The tax rates

and tax laws used to compute the amount are those that are

enacted or substantively enacted at the end of the reporting period.

Deferred tax

Deferred tax assets and liabilities are recognised in respect of

temporary differences between the tax base and carrying value

of assets and liabilities including accelerated capital allowances,

unrelieved tax losses, unremitted profits from subsidiaries,

gains rolled over into replacement assets, gains on previously

revalued properties and other short-term temporary differences.

Deferred tax assets are recognised to the extent that it is regarded

as probable that the deductible temporary differences can be

realised. The recoverability of all deferred tax assets is re-assessed

at the end of each reporting period.

Deferred tax is calculated at the tax rates that are expected to apply in

the periods in which the asset or liability will be settled, based on rates

enacted or substantively enacted at the end of the reporting period.

Retirement benefits

Defined contribution plans

Payments to defined contribution schemes are charged to the income

statement as they fall due.

Defined benefit plans

Plan assets, including qualifying insurance policies, are measured at

fair value and plan liabilities are measured on an actuarial basis, using

the projected unit credit method and discounting at an interest rate

equivalent to the current rate of return on a high-quality corporate bond

of equivalent currency and term to the plan liabilities. The difference

between the value of plan assets and liabilities at the period-end date is

the amount of surplus or deficit recorded in the statement of financial

position as an asset or liability. An asset is recognised when the

employer has an unconditional right to use the surplus at some point

during the life of the plan or on its wind-up. If a refund would be subject

to a tax other than income tax, as is the case in the UK, the asset is

recorded at the amount net of the tax. A liability is also recorded for

any such tax that would be payable in respect of funding commitments

based on the accounting assumption that the related payments

increase the asset.

The service cost of providing pension benefits to employees, together

with the net interest expense or income for the year, is charged to the

income statement within ‘administration expenses’. Net interest is

calculated by applying the discount rate to the net defined benefit asset

or liability, after any asset restriction. Past service costs and gains,

which are the change in the present value of the defined benefit

obligation for employee service in prior periods resulting from plan

amendments, are recognised immediately the plan amendment occurs.

Re-measurements comprise actuarial gains and losses, the return on

plan assets (excluding amounts included in net interest) and changes

in the amount of any asset restrictions. Actuarial gains and losses

may result from: differences between the actuarial assumptions

underlying the plan liabilities and actual experience during the year

or changes in the actuarial assumptions used in the valuation of the

plan liabilities. Re-measurement gains and losses, and taxation

thereon, are recognised in other comprehensive income and are not

reclassified to profit or loss in subsequent periods.

Actuarial valuations are normally carried out every three years and

are updated for material transactions and other material changes in

circumstances (including changes in market prices and interest rates)

up to the end of the reporting period.

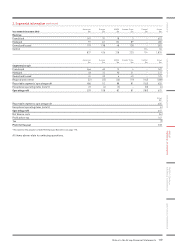

Revenue recognition

Revenue arises from the sale of goods and provision of services

where these activities give rise to economic benefits received and

receivable by the Group on its own account and result in increases

in equity.

Revenue is derived from the following sources: franchise fees;

management fees; owned and leased properties and other

revenues which are ancillary to the Group’s operations,

including technology fee income.

Generally, revenue represents sales (excluding VAT and similar

taxes) of goods and services, net of discounts, provided in the

normal course of business and recognised when services have

been rendered. The following is a description of the composition

of revenues of the Group.

Franchise fees – received in connection with the license of the

Group’s brand names, usually under long-term contracts with

the hotel owner. The Group charges franchise royalty fees as a

percentage of rooms revenue. Revenue is earned and recognised

on a monthly basis.

Management fees – earned from hotels managed by the Group,

usually under long-term contracts with the hotel owner.

Management fees include a base fee, generally a percentage of

hotel revenue, which is earned and recognised on a monthly basis

and an incentive fee, generally based on the hotel’s profitability or

cash flows and recognised when the related performance criteria

are met under the terms of the contract.

Owned and leased – primarily derived from hotel operations,

including the rental of rooms and food and beverage sales from

owned and leased hotels operated under the Group’s brand names.

Revenue is recognised when rooms are occupied and food and

beverages are sold.

Franchise fees and management fees include liquidated damages

received from the early termination of contracts.

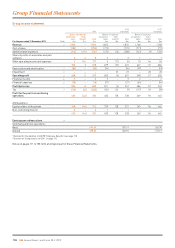

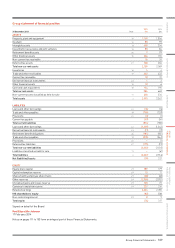

114 IHG Annual Report and Form 20-F 2013

Accounting policies continued