Holiday Inn 2013 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2013 Holiday Inn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

|

|

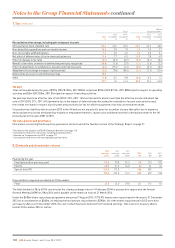

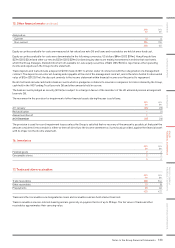

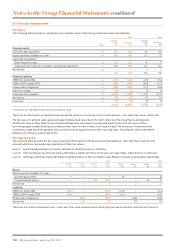

Liquidity risk exposure

The treasury function ensures that the Group has access to

sufficient funds to allow the implementation of the strategy set

by the Board. Medium and long-term borrowing requirements

are met through the $1.07bn Syndicated Facility which expires in

November 2016, through the £250m 6% bonds that are repayable on

9December 2016 and through the £400m 3.875% bonds repayable

on 28 November 2022. The bonds were issued under the Group’s

£750m Medium Term Notes programme. Short-term borrowing

requirements are met from drawings under bilateral bank facilities.

The $1.07bn Syndicated Facility was undrawn at the year end.

The Syndicated Facility contains two financial covenants: interest cover

and net debt divided by earnings before interest, tax, depreciation

and amortisation (EBITDA). The Group is in compliance with all of the

financial covenants in its loan documents, none of which is expected

to present a material restriction on funding in the near future.

At the year end, the Group had cash of $134m which is predominantly

held in short-term deposits and cash funds which allow daily

withdrawals of cash. Most of the Group’s funds are held in the UK or

US, although $12m (2012 $7m) is held in countries where repatriation

is restricted as a result of foreign exchange regulations.

The Group had net liabilities of $74m at 31 December 2013

reflecting that its brands, in accordance with accounting standards,

are not recorded on the balance sheet.

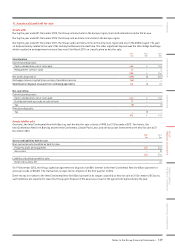

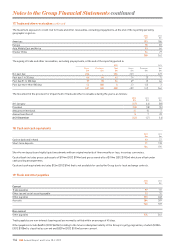

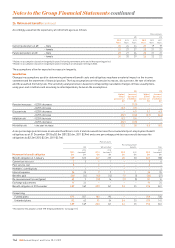

Credit risk exposure

Credit risk on treasury transactions is minimised by operating a

policy on the investment of surplus cash that generally restricts

counterparties to those with an A credit rating or better or those

providing adequate security.

Notwithstanding that counterparties must have an A credit rating

orbetter, during periods of significant financial market turmoil,

counterparty exposure limits are significantly reduced and

counterparty credit exposure reviews are broadened to include

therelative placing of credit default swap pricings.

The Group trades only with recognised, creditworthy third parties.

Itis the Group’s policy that all customers who wish to trade on

credit terms are subject to credit verification procedures.

In respect of credit risk arising from financial assets, the Group’s

exposure to credit risk arises from default of the counterparty,

witha maximum exposure equal to the carrying amount of

theseinstruments.

Capital risk management

The Group manages its capital to ensure that it will be able to

continue as a going concern. The capital structure consists of net

debt, issued share capital and reserves totalling $1,071m at

31December 2013 (2012 $1,382m). The structure is managed to

maintain an investment grade credit rating, to provide ongoing

returns to shareholders and to service debt obligations, whilst

maintaining maximum operational flexibility. A key characteristic

ofIHG’s managed and franchised business model is that it is

highlycash generative, with a high return on capital employed.

Surplus cash is either reinvested in the business, used to repay debt

or returned to shareholders. The Group’s debt is monitored on the

basis of a cash flow leverage ratio, being net debt divided by EBITDA,

with the objective of maintaining an investment grade credit rating.

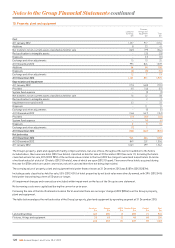

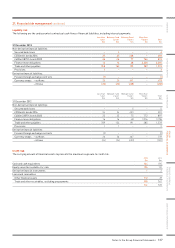

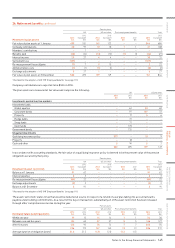

Hedging

Interest rate risk

The Group hedges its interest rate risk by ensuring that interest

flows are fixed on at least 25% of its borrowings inmajor

currencies. If required, the Group uses interest rate swaps

to manage the exposure although none were held at either

31 December 2013 or 31 December 2012. The Group designates

interest rate swaps as cash flow hedges. At both 31 December

2013 and 31 December 2012, the Group’s interest flows were

100% fixed due to the low interest environment and profile of the

Group’s debt.

Foreign currency risk

The Group is exposed to foreign currency risk on income streams

denominated in foreign currencies. From time to time, the Group

hedges a portion of forecast foreign currency income by taking

out forward exchange contracts. The designated risk is the spot

foreign exchange risk. There were no such contracts in place at

either 31December 2013 or 31 December 2012.

Hedge of net investment in foreign operations

The Group designates its foreign currency bank borrowings

and currencyderivatives as net investment hedges of foreign

operations. Thedesignated risk is the spot foreign exchange

risk for loans and shortdated derivatives and the forward risk

for the seven-year currency swaps. The interest on these financial

instruments is taken through financial income or expense except

for the seven-year currency swaps where interest is taken to the

currency translation reserve.

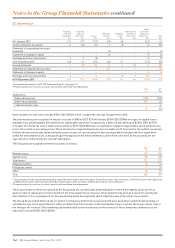

At 31 December 2013, the Group held currency swaps with

a principal of $415m (2012 $415m) and short dated foreign

exchange swaps with principals of €75m (2012 €75m) and $100m

(2012 $170m) (see note 23 for further details). The maximum

amount of foreign exchange derivatives held during the year as

net investment hedges and measured at calendar quarter ends

were currency swaps with a principal of $415m (2012 $415m)

and short dated foreign exchange swaps with principals of €75m

(2012 €75m) and $310m (2012 $350m).

Hedge effectiveness is measured at calendar quarter ends.

Noineffectiveness arose in respect of either the Group’s cash flow

ornet investment hedges during the current or prior year.

21. Financial risk management continued

136 IHG Annual Report and Form 20-F 2013

Notes to the Group Financial Statements continued