HSBC 2010 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

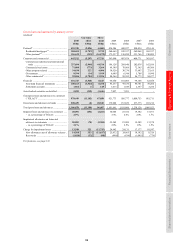

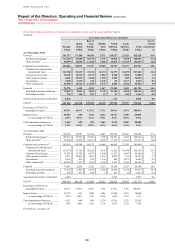

Report of the Directors: Operating and Financial Review (continued)

Risk > Challenges and uncertainties > Macro-prudential and regulatory

90

We have significant exposure to

counterparty risk within our portfolio

We have exposure to virtually all major industries

and counterparties, and we routinely execute

transactions with counterparties in financial services,

including brokers and dealers, commercial banks,

investment banks, mutual and hedge funds, and other

institutional clients. Many of these transactions

expose us to credit risk in the event of default by our

counterparty or client. Financial institutions are

necessarily interdependent because of trading,

clearing, counterparty or other relationships. As a

consequence, a default by, or decline in market

confidence in, individual institutions, or anxiety

about the financial services industry generally, can

lead to further individual and/or systemic losses. Our

credit risk may remain high if the collateral taken to

mitigate counterparty risk cannot be realised or has

to be liquidated at prices which are insufficient to

recover the full amount of our loan or derivative

exposure. For further information relating to the

major risk areas, see ‘Areas of Special Interest’ on

page 103.

Macro-prudential and regulatory

We face a number of challenges in

regulation and supervision

Financial services providers face increased

regulation and supervision, with more stringent and

costly requirements in the areas of capital and

liquidity management and of compliance relating to

conduct of business and the integrity of financial

services delivery. Increased government intervention

and control over financial institutions, together with

measures to reduce systemic risk, could significantly

alter the competitive landscape.

Recent regulatory and supervisory

developments have largely been shaped by the

leaders, Finance Ministers and Central Bank

Governors of the Group of Twenty nations (‘the

G20’), who delegated the development and issuance

of standards to the Basel Committee of Banking

Supervisors (‘the Basel Committee’). The G20 also

established the Financial Stability Board (‘FSB’) to

assess vulnerabilities affecting the financial system

as a whole, as well as to monitor and advise on

market developments and best practice in meeting

regulatory standards.

In looking to address the systemic failures that

caused the financial crisis of 2007-8, the authorities

asserted two primary objectives: to establish a

resilient system to reduce substantially the risks of

failure of financial institutions and, in case failure in

the end proved unavoidable, to have in place

measures to achieve orderly resolution without cost

to taxpayers. Governments and regulators have

embarked on significant change in the regulation of

the financial system, highlighting the following

priorities:

• a stronger international framework for

prudential regulation, ensuring significantly

increased liquidity and regulatory capital buffers

and enhanced quality of capital;

• convergence towards a single set of high-

quality, global, independent accounting

standards, with particular focus on accounting

for financial instruments and off-balance sheet

exposures;

• strengthening the regulation of hedge funds

and credit rating agencies, and improving the

infrastructure for derivative transactions,

including central counterparty clearing of over-

the-counter derivatives;

• design and implementation of a system which

will allow for the restructuring or resolution of

financial institutions, without taxpayers

ultimately bearing the burden;

• an increased role for colleges of supervisors to

coordinate oversight of systemically significant

institutions such as HSBC, and effective

coordination of resolution regimes for failed

banks;

• measures on financial sector compensation

arrangements to prevent excessive short-term

risk taking and mitigate systemic risk on a

globally consistent basis; and

• a fair and substantial contribution by the

financial sector towards paying for any burden

associated with government interventions,

where they occur, to repair and reduce risks

from the financial system or to fund the

resolution of problems.

Measures proposed by the Basel Committee to

increase resilience in the financial system

The Basel Committee, following consultation,

impact analyses and draft proposals during 2010,

issued final proposals in December 2010, known as

Basel III, on the twin areas of capital and liquidity,

the key aspects of which are set out below.

• Risk weightings: increased weightings for the

trading book and re-securitisations are planned

for implementation by the end of 2011. A

fundamental review of the trading book will

continue during 2011.