HSBC 2010 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

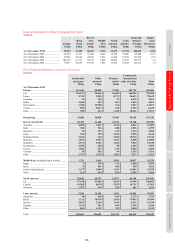

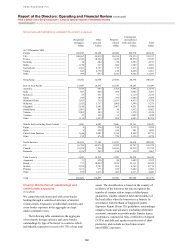

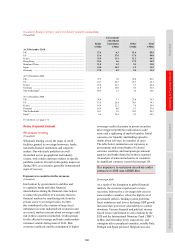

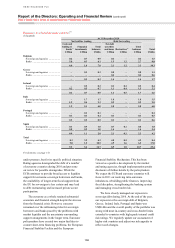

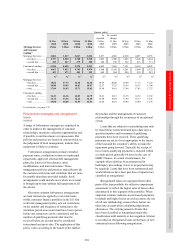

Risk > Credit risk > Areas of special interest > Personal lending

106

Across our portfolios, credit risk is mitigated by

long-standing and conservative policies on asset

origination which focus on relationships with long-

term customers and limited initial leverage. We also

set and monitor sector risk appetite limits at Group

and regional levels to detect and prevent higher risk

concentrations. While individual regions differ in

their approach, typically origination loan to value

ratios would be less than 65% across the Group.

Personal lending

(Unaudited)

We provide a broad range of secured and unsecured

personal lending products to meet customer needs.

Given the diverse nature of the markets in which

we operate, the range is not standard across

all countries but is tailored to meet the demands

of individual markets while using appropriate

distribution channels and, wherever possible, global

IT platforms.

Personal lending includes advances to customers

for asset purchases, such as residential property and

motor vehicles, where the loans are typically secured

by the assets being acquired. We also offer loans

secured on existing assets, such as first and second

liens on residential property; unsecured lending

products such as overdrafts, credit cards and payroll

loans; and debt consolidation loans which may be

secured or unsecured.

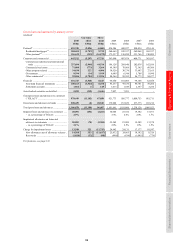

In 2010, credit quality in our personal lending

portfolios improved, reflecting a recovery of

economic conditions in most markets. Delinquency

levels and loan impairment charges declined,

particularly in those countries which had previously

been most affected by rising unemployment and

house price depreciation.

The commentary that follows is on an

underlying basis.

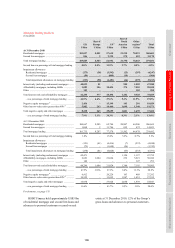

At 31 December 2010, total personal lending

was US$425bn, a decline of 2% from 31 December

2009 as the reduction in our US run-off portfolios

continued, partly offset by notable growth in Hong

Kong and the UK. Within our PFS business, total

loan impairment charges and other credit risk

provisions of US$11.3bn were 44% lower than in

2009, and were concentrated in North America

(US$8.2bn) and, to a lesser extent, Europe

(US$1.2bn) and Latin America (US$1.2bn).

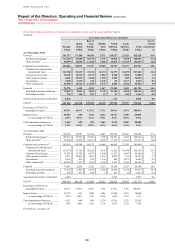

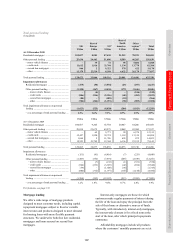

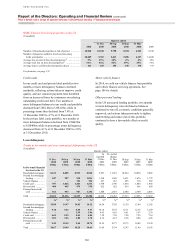

In the UK, total personal lending was

US$129bn, an increase of 4% compared with the end

of 2009. The increase was due to growth in mortgage

lending as a result of the enhancement of our product

offerings, successful marketing and competitive

pricing (UK mortgage lending is discussed in greater

detail on page 108). This was partly offset by an 8%

fall in other personal lending balances, reflecting a

reduction in unsecured lending products as we

tightened our underwriting criteria and some

consumers reduced their indebtedness.

Total personal lending balances in the US at

31 December 2010 were US$109bn, a decrease of

19% compared with the end of 2009, reflecting the

continued reduction in balances in our consumer

finance run-off portfolios and lower balances in our

Card and Retail Services business.

US residential mortgage lending balances fell by

12% to US$58bn, driven by the decisions taken in

2007 to close the Mortgage Services business and in

March 2009 to close all Consumer Lending branches

and run off the residual consumer finance balances.

US mortgage lending is discussed in greater detail on

page 108.

In PFS, total loan impairment charges and

other credit risk provisions were 44% down

on 2009.

Other personal lending balances in the US were

US$52bn at 31 December 2010, 25% lower than at

the end of 2009. Credit card balances declined by

14% reflecting a reduction in active customer

accounts and an increased focus by our customers

on reducing outstanding credit card debt.

In March we sold US$1.0bn of vehicle finance

loans. This was followed in August by the sale of the

residual vehicle finance loans (US$4.3bn) to the

same purchaser.

In Hong Kong, total personal lending grew by

20% to US$57bn as a result of strong growth in

residential mortgage lending. In the Rest of Asia-

Pacific region, personal lending also grew strongly

across many countries, notably Australia, Singapore

and Malaysia, through successful marketing. This

growth was partly offset by a managed reduction in

unsecured personal lending balances in India.

In Latin America, total personal lending was

broadly flat at US$22bn as moderate growth in

residential mortgage lending, particularly in Brazil,

was more than offset by a decline in other personal

lending. The latter reflected falls in credit card

lending in Mexico and other higher-risk portfolios in

Mexico and Brazil as we continued to reduce higher-

risk portfolios in the region and tighten our

underwriting criteria.

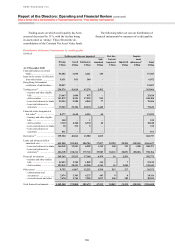

For an analysis of loan impairment allowances

and impaired loans, see page 119.