HSBC 2010 Annual Report Download - page 148

Download and view the complete annual report

Please find page 148 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Risk > Market risk > Sensitivity analysis / Trading and non-trading portfolios

146

We routinely validate the accuracy of our VAR

models by back-testing the actual daily profit and

loss results, adjusted to remove non-modelled

items such as fees and commissions, against the

corresponding VAR numbers. Statistically, we would

expect to see losses in excess of VAR only 1% of the

time over a one-year period. The actual number of

excesses over this period can therefore be used to

gauge how well the models are performing.

Stress testing

(Audited)

In recognition of VAR’s limitations, we augment it

with stress testing to evaluate the potential impact on

portfolio values of more extreme, although plausible,

events or movements in a set of financial variables.

The process is governed by the Stress Testing

Review Group forum which, in conjunction with

regional risk managers, determines the scenarios to

be applied at portfolio and consolidated levels, as

follows:

• sensitivity scenarios consider the impact of any

single risk factor or set of factors that are

unlikely to be captured within the VAR models,

such as the break of a currency peg;

• technical scenarios consider the largest move in

each risk factor, without consideration of any

underlying market correlation;

• hypothetical scenarios consider potential macro

economic events, for example, a global flu

pandemic; and

• historical scenarios incorporate historical

observations of market movements during

previous periods of stress which would not be

captured within VAR.

Stress testing results provide senior management

with an assessment of the financial effect such

events would have on our profit.

Trading and non-trading portfolios

(Audited)

The following table provides an overview of the

reporting of risks within this section:

Portfolio

Trading Non-trading

Risk type

Foreign exchange and

commodity ........................ VAR VAR63

Interest rate ........................... VAR VAR64

Equity .................................... VAR Sensitivity

Credit spread ......................... VAR VAR65

For footnotes, see page 174.

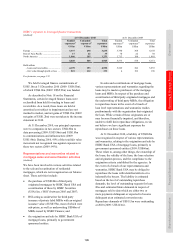

Value at risk of the trading and non-trading

portfolios

Our Group VAR, both trading and non-trading, was

as follows:

Value at risk (excluding credit spread VAR)

(Audited)

2010 2009

US$m US$m

At 31 December ................... 266.6 204.5

Average ................................ 199.8 156.1

Minimum ............................. 139.5 105.7

Maximum ............................. 285.7 204.5

The rise in interest rate volatility, coupled with a

modest increase in underlying interest rate exposure,

resulted in a higher VAR and higher maximum VAR

at the end of 2010 compared with the end of 2009.

The volatility in the other asset classes in 2010 was

lower than in 2009.

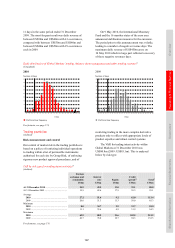

Our Group daily VAR, both trading and non-

trading, was as follows:

Daily VAR (excluding credit spread) (US$m)

(Unaudited)

0

50

100

150

200

250

300

Dec-08 Apr-09 Aug-09 Dec-09 Apr-10 Aug-10 Dec-10

The major contributor to our Group trading and

non-trading VAR was Global Markets.

The histogram below illustrates the frequency of

daily revenue arising from Global Markets’ trading,

balance sheet management and other trading

activities.

Daily revenue

(Unaudited)

2010 2009

US$m US$m

Average daily revenue ......... 49.3 59.9

Standard deviation66 ............. 37.8 38.4

For footnote, see page 174.

An analysis of the frequency distribution of

daily revenue shows that there were nine days with

negative revenues during 2010 compared with