HSBC 2010 Annual Report Download - page 167

Download and view the complete annual report

Please find page 167 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

165

Overview Operating & Financial Review Governance Financial Statements Shareholder Information

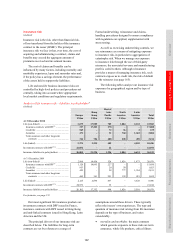

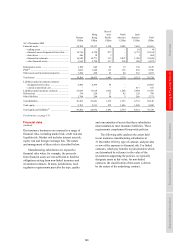

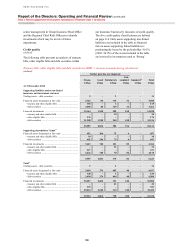

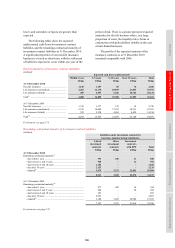

Sensitivity of HSBC’s insurance manufacturing subsidiaries to risk factors

(Audited)

2010 2009

Effect on

profit for

the year

Effect on

total

equity

Effect on

profit for

the year

Effect on

total

equity

US$m US$m US$m US$m

+ 100 basis points parallel shift in yield curves ........................... 72 (132) 68 (82)

– 100 basis points parallel shift in yield curves ........................... (86) 131 (69) 92

10% increase in equity prices ....................................................... 76 76 19 19

10% decrease in equity prices ...................................................... (76) (76) (20) (20)

10% increase in US dollar exchange rate

compared to all currencies ....................................................... 21 21 20 20

10% decrease in US dollar exchange rate

compared to all currencies ....................................................... (21) (21) (20) (20)

Sensitivity to credit spread increases ........................................... (31) (74) (36) (91)

Where appropriate, we include the impact of the

stress on the PVIF in the results of the stress tests.

The relationship between the values of certain assets

and liabilities and the risk factors may be non-linear

and, therefore, the results disclosed cannot be

extrapolated to measure sensitivities to different

levels of stress. The sensitivities are stated before

allowance for the effect of management actions

which may mitigate changes in market rates, and for

any factors such as policyholder behaviour that may

change in response to changes in market risk.

Credit risk

(Audited)

Description of credit risk

Credit risk can give rise to losses through default

and can lead to volatility in our income statement

and balance sheet figures through movements in

credit spreads, principally on the US$43.3bn (2009:

US$40.5bn) non-linked bond portfolio.

As tabulated above, the sensitivity of the net

profit after tax of our insurance subsidiaries to the

effects of increases in credit spreads is a fall of

US$31m (2009: US$36m fall). This is small because

51.4% of the financial assets held by our insurance

subsidiaries are classified as either held to maturity

or available for sale, and consequently any changes

in the fair value of these financial investments,

absent impairment, would have no impact on the

profit after tax. We calculate the sensitivity using

simplified assumptions based on a one-day

movement in credit spreads over a two-year period.

A confidence level of 99%, consistent with our

Group VAR, is applied. While credit spreads have

generally widened from the levels observed at the

end of 2009, the volatility experienced during 2010

was lower than that seen in 2009, leading to a

reduction in our sensitivity to credit spread

movements.

We used to sell certain unit-linked life insurance

contracts which were reinsured with a third-party

counterparty, who also underwrote market return

guarantees. We are exposed to credit risk to the

extent that the counterparty is unable to meet the

terms of the guaranteed benefits. The cost to us of

market return guarantees increases when interest

rates fall, equity markets fall or market volatility

increases. In addition, when determined by reference

to a discounted cash flow model in which the

discount rate is based on current interest rates,

guarantee costs increase in a falling interest rate

environment. The sale of these contracts ceased in

2008, reflecting our adjusted risk appetite.

How credit risk is managed

Our exposure to credit risk products is included in

the tables showing exposures to life and non-life

insurance risk on pages 157 to 159. Our insurance

manufacturing subsidiaries are responsible for the

credit risk, quality and performance of their

investment portfolios. Our assessment of the

creditworthiness of issuers and counterparties is

based primarily upon internationally recognised

credit ratings and other publicly available

information.

Investment credit exposures are monitored

against limits by our local insurance manufacturing

subsidiaries, and are aggregated and reported to

Group Credit Risk, the Group Insurance Credit Risk

Meeting and the Group Insurance Risk Committee.

Stress testing is performed by Group Insurance Head

Office on the investment credit exposures using

credit spread sensitivities and default probabilities.

The stresses are reported to the Group Insurance

Risk Committee.

We use a number of tools to manage and

monitor credit risk. These include an Early Warning

Report and a watch list of investments with current

credit concerns which are circulated fortnightly to