HSBC 2010 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

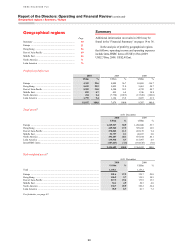

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

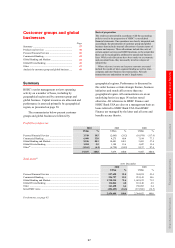

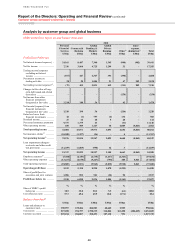

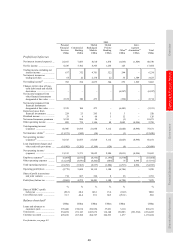

Customer groups and global businesses > PFS

40

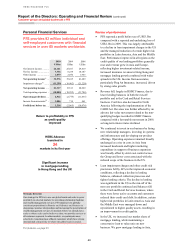

Personal Financial Services

PFS provides 92 million individual and

self-employed customers with financial

services in over 60 markets worldwide.

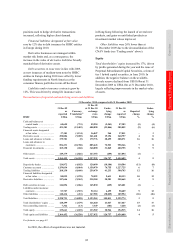

2010 2009 2008

US$m US$m US$m

Net interest income ........... 24,161 25,107 29,419

Net fee income .................. 7,336 8,238 10,107

Other income .................... 1,079 2,070 1,963

Net operating income46 ... 32,576 35,415 41,489

Impairment charges47 ........ (11,259) (19,902) (21,220)

Net operating income ..... 21,317 15,513 20,269

Total operating expenses .. (18,805) (18,292) (31,704)

Operating profit/(loss) .... 2,512 (2,779) (11,435)

Income from associates48 .. 1,006 714 461

Profit/(loss) before tax .... 3,518 (2,065) (10,974)

Return to profitability in PFS

as credit quality

improved

HSBC Advance

launched in

34

markets in its first year

Significant increase

in mortgage lending

in Hong Kong and the UK

Strategic direction

Our strategy for PFS is to use our global reach and scale to grow

profitably in selected markets by providing relationship banking

and wealth management services. PFS employs two globally

consistent propositions in Premier and Advance and focuses on

deepening customer relationships and increasing the penetration of

wealth management services. In markets where we already have

scale or where scale can be built over time, we provide services to

all customer segments. In other markets, we participate more

selectively, targeting mass affluent customers which have strong

international connectivity or where our global scale is crucial.

For footnotes, see page 83.

Review of performance

• PFS reported a profit before tax of US$3.5bn

compared with a reported and underlying loss of

US$2.1bn in 2009. This was largely attributable

to a decline in loan impairment charges in the US

and the managed reduction of certain higher risk

portfolios in Latin America, Asia and the Middle

East. Performance improved in all regions as the

credit quality of our lending portfolios generally

rose and revenue grew in Asia and Europe,

reflecting higher investment-related income,

increased insurance revenue in Hong Kong and

mortgage lending growth combined with wider

spreads in the UK. Income from associates,

particularly Ping An Insurance, increased, driven

by strong sales growth.

• Revenue fell, largely in HSBC Finance, due to

lower lending balances in both the run-off

portfolio and in the Card and Retail Services

business. Card fees also decreased in North

America following the implementation of the

CARD Act. Revenue was further affected by an

adverse fair value movement related to the non-

qualifying hedges recorded in HSBC Finance

compared with a favourable movement in 2009,

as long-term interest rates declined.

• We continued to invest in our business by hiring

new relationship managers, investing in systems

and infrastructure and developing our product

offerings. Operating expenses remained broadly

unchanged as a rise in costs in Asia from

increased headcount and higher marketing

expenditure in support of business expansion

was broadly offset by strict cost control across

the Group and lower costs associated with the

reduced scope of the business in the US.

• Loan impairment charges and other credit risk

provisions fell by 44% in the improved economic

conditions, reflecting a decline in lending

balances, enhanced collection processes and

tighter lending criteria. The decline in lending

was significant in the US as the run-off of the

non-core portfolio continued and balances fell

in the Card and Retail Services business, where

there were fewer active accounts and customers

reduced their credit card debt. In addition, certain

higher risk portfolios in Latin America, Asia and

the Middle East were managed down and

repositioned to higher quality assets, resulting in

an improvement in credit quality.

• In the UK, we increased our market share of

mortgage lending, while maintaining a

conservative loan to value ratio on new

business. We grew mortgage lending in Asia,