HSBC 2010 Annual Report Download - page 158

Download and view the complete annual report

Please find page 158 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

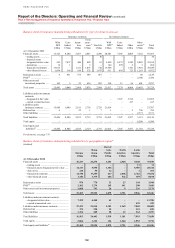

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Risk > Risk management of insurance operations > Overview of products / Nature and extent of risks / Insurance risk

156

Our manufacturing business concentrates on

personal lines, e.g. contracts written for individuals.

This focus on the higher volume, lower individual

value personal lines contributes to diversifying risk.

Overview of insurance products

(Audited)

The main contracts we manufacture are listed below:

Life insurance business

• Life insurance contracts with discretionary

participation features (‘DPF’);

• credit life insurance business;

• annuities;

• term assurance and critical illness policies;

• linked life insurance;

• investment contracts with DPF;

• unit-linked investment contracts; and

• other investment contracts (including pension

contracts written in Hong Kong).

Non-life insurance business

Non-life insurance contracts include motor, fire and

other damage to property, accident and health,

repayment protection and commercial insurance.

Credit non-life insurance is concentrated in

North America and Europe, and is originated in

conjunction with the provision of loans. Following

a decision taken to close the Consumer Lending

network in the US, insurance products written in

conjunction with this business are being run off.

In December 2007, we decided to stop selling

payment protection insurance (‘PPI’) products in the

UK and a phased withdrawal was completed across

the HSBC, first direct and M&S Money brands

during 2008. HFC ceased selling single premium

PPI in 2008 and sales of regular premium PPI

will reduce as HFC exits its remaining retail

relationships. HSBC continues to distribute its UK

short-term income protection (‘STIP’) product. In

January 2009, the Competition Commission (‘CC’)

published its report into the PPI market in which it

stipulated that STIP products will also be subject to

their remedies when sold in conjunction with or as a

result of a referral following the sale of a loan or

similar credit product. We have undertaken an

analysis of the required changes to the STIP product

and its sales processes resulting from the CC’s

remedies. Following an appeal to the Competition

Appeal Tribunal, the CC had to reconsider whether a

ban on firms selling PPI at the point of sale of the

credit product was an appropriate and justified

remedy for the deficiencies it identified in the PPI

market. On 14 October 2010, the CC confirmed that

it intended to proceed with a point of sale ban. It is

anticipated that the Order implementing the CC’s

remedies will be made in late March or early April,

and that the point of sale ban will then come into

effect 12 months after the date of the Order.

Nature and extent of risks

(Audited)

The majority of the risk in our insurance business

derives from manufacturing activities and can be

categorised as insurance risk and financial risks. The

following sections describe how these risks are

managed. Financial risks include market risk, credit

risk and liquidity risk. The assets of insurance

manufacturing subsidiaries are included within the

consolidated credit risk disclosures on pages 93

to 128, although separate disclosures in respect of

insurance manufacturing subsidiaries are provided

below. The consolidated liquidity risk and market

risk disclosures focus on banking entities and

disclosures specific to the insurance manufacturing

subsidiaries are provided in the sections below.

Operational risk is covered by the Group’s overall

operational risk management process.

The insurance manufacturers set their own

control procedures in addition to complying with

guidelines issued by the Group Insurance Head

Office. The control framework for monitoring risk

includes the Group Insurance Risk Committee,

which oversees the status of the significant risk

categories in the insurance operations. Five sub-

committees of this Committee focus on products

and pricing, market and liquidity risk, credit risk,

operational risk and insurance risk, respectively.

Similar risk committees exist at regional and entity

levels. Any issues requiring escalation from the

Group Insurance Risk Committee would be reported

to the GMB via the Risk Management Meeting.

In addition, local ALCOs and Risk Management

Committees monitor certain risk exposures, mainly

for life business where the duration and cash flow

matching of insurance assets and liabilities are

reviewed.

All insurance products, whether manufactured

internally or by a third party, are subjected to a

product approval process. Approval is provided

by the Regional Insurance Head Office or Group

Insurance Head Office depending on the type of

product and its risk profile. The approval process

is formalised through the Product and Pricing

Committee, which comprise the heads of the relevant

risk functions within insurance.