HSBC 2010 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

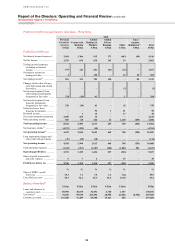

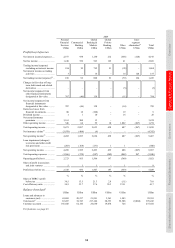

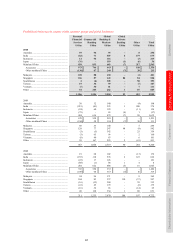

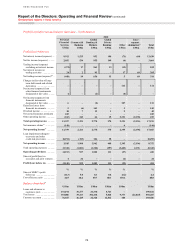

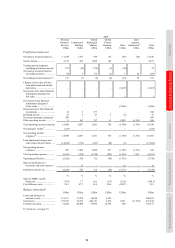

Geographical regions > Middle East

68

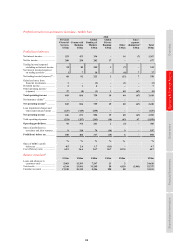

Net interest income decreased by 8% as average

lending balances declined in both PFS and CMB, the

proportion of higher yielding assets fell and the cost

of liquidity remained high.

In PFS, spreads narrowed as we focused new

lending on Premier and Advance customers, while

concurrently managing down higher risk unsecured

lending balances, mostly in the UAE.

In CMB, asset balances and net interest income

rose throughout the second half of 2010 as

increasing trade finance balances contributed to

growing revenues.

Average customer accounts declined as

corporate customers reduced their deposits in

response to tighter liquidity in the local markets.

This was partly offset by an increase in average

liability balances in PFS, which was driven by

successful deposit campaigns launched in 2010 and

by the acquisition of Premier and A dvance

customers. Our overall liquidity position improved

although the market returns on the deployment of

liquidity remained low.

Net fee income increased by 8%, primarily

driven by higher volumes of credit facilities related

to trade, guarantees and remittances in CMB. The

benefit was partly offset by lower advisory revenues

from equity capital markets in GB&M as a result of

limited issuances in the regional equity markets.

Net trading income fell by 6% to US$370m.

Subdued trading conditions and the non-recurrence

of gains which had resulted from the tightening of

credit spreads on certain positions in early 2009

resulted in lower Credit trading income. Foreign

exchange income decreased with the easing in

market volatility as speculation regarding the

unpegging of Gulf currencies from the US dollar

receded.

Other operating income declined by US$37m as

gains arising in 2009 from the buy-back and

extinguishment of own debt did not recur.

Loan impairment charges and other credit risk

provisions decreased by 53%. An overall

improvement in credit conditions in the region along

with enhanced collections processes, improvements

in the quality of our customer base and a reduction

in unsecured lending resulted in significantly lower

net collective impairment provisions, notably in the

UAE, and lower requirements for specific corporate

provisions.

In PFS, strengthened collections processes

and a repositioning of the loan book contributed to

lower delinquency rates. In CMB, loan impairment

charges and other credit risk provisions decreased

due to significantly lower net collectively assessed

impairment charges and fewer specific loan

impairment charges, with the majority of the charge

in 2010 relating to a small number of large corporate

customers.

Loan impairment charges and other credit risk

provisions in GB&M rose, mainly from restructuring

activity which drove UAE-related loan impairments

for a small number of large corporate customers in

the first half of 2010. The improvement in economic

conditions during the latter part of 2010 resulted in

lower loan impairment charges in the second half of

the year.

Operating expenses increased by 8%, driven by

increased investment in marketing and advertising,

including key sponsorship deals and the promotion

of the HSBC brand through strategic messaging in

the Abu Dhabi and Dubai airports, together with an

increase in premises and people costs, mainly from

the investment in the branch network expansion in

Egypt.

Profit from associates and joint ventures

decreased by 5%. The contribution from The

Saudi British Bank was lower as revenue fell in

challenging operating conditions.