HSBC 2010 Annual Report Download - page 110

Download and view the complete annual report

Please find page 110 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Risk > Credit risk > Areas of special interest > Personal lending

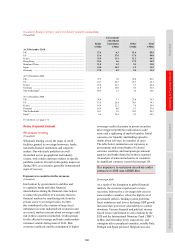

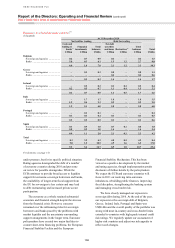

108

a low initial rate, either variable or fixed, before

resetting to a higher rate once the introductory period

is over. Offset mortgages are products linked to a

current or savings account, where interest earned is

used to repay mortgage debt.

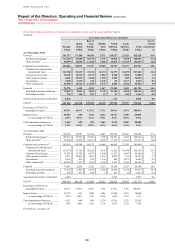

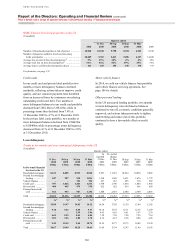

UK mortgage lending

On a constant currency basis, total mortgage lending

in the UK, comprising residential and second lien

lending, increased by 7% to US$104bn at

31 December 2010. Growth was achieved largely

through the enhancement of our product offerings,

successful marketing and competitive pricing.

Nonetheless, mortgage lending was constrained by

the decline in re-mortgage activity due to the low

interest rate environment and consumer concerns

over future employment and higher interest rates.

Our UK mortgage portfolio remained of high

quality, consisting primarily of lending to owner-

occupiers. We restricted lending to purchase

residential property for the purpose of rental and

almost all new business was originated through our

own salesforce, with the self-certification of income

not permitted. The majority of mortgage lending was

to existing customers holding current or savings

accounts with HSBC; this facilitated and

strengthened the underwriting process.

Loan impairment charges and delinquency

levels in our UK mortgage book declined despite

unemployment remaining high, mainly due to

improving economic conditions and low interest

rates, which helped make mortgages more affordable

for customers. Our continuing enhancements in

credit underwriting, credit policies and collection

processes contributed to the reduction in

delinquencies.

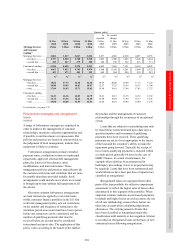

The percentage of loans that were 30 days or

more delinquent declined from 1.6% at 31 December

2009 to 1.4% in 2010 in the HSBC Bank mortgage

portfolio and remained at less than 1.0% in the First

Direct portfolio.

In 2010, the average loan-to-value ratio for

new business in the UK was 54%, an increase of a

single percentage point on the previous year.

Interest-only mortgage balances increased

by 4% to US$45bn compared with 2009. The

majority of these mortgages were offset mortgages

at First Direct for which delinquency rates remained

at very low levels.

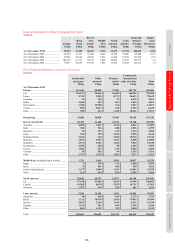

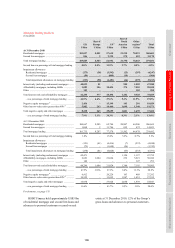

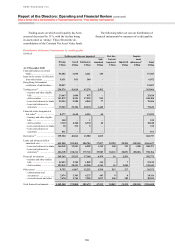

US mortgage lending

US mortgage lending balances, comprising

residential and second lien lending, were US$67bn at

31 December 2010, a decline of 14% compared with

the end of 2009.

Mortgage lending in HSBC Finance fell by 17%

to US$51bn with declines in both the Consumer

Lending and Mortgage Services portfolios from

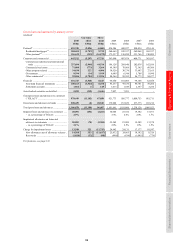

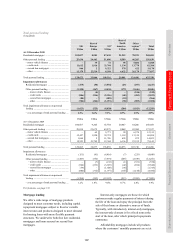

their planned run-off. See table on page 110 for a

breakdown of mortgage lending in HSBC Finance.

Mortgage lending in the UK rose by 7% to

US$104bn, while in the US balances

declined by 14% to US$67bn.

Mortgage lending balances in HSBC Bank USA

remained broadly unchanged at US$16bn. We

continue to sell the majority of new origination to

the secondary markets as a means of managing our

interest rate risk and improving structural liquidity.

This reduction was partly offset by an increase in

originations to Premier customers with whom we

already held a banking relationship. At 31 December

2010, approximately 32% of the HSBC Bank USA

mortgage portfolio were fixed rate loans and 77%

were first lien.

During 2010, state and federal officials

announced investigations into the procedures

followed by mortgage servicing companies and

banks, including HSBC Finance and its affiliates,

in relation to foreclosures. This included a joint

examination by the Federal Reserve and the Office

of the Comptroller of the Currency. Following the

examination, our examiners issued supervisory

letters noting deficiencies in our processing,

preparation and signing of affidavits and other

documents supporting foreclosures, and in the

governance of and resources devoted to our

foreclosure process. We have suspended foreclosures

pending correction of the weaknesses. Management

is reviewing all foreclosures which have not yet been

completed, and will correct deficient documentation

and refile documents where required.

As a result of the investigations, we expect that

the scrutiny of documents will increase, and in some

states additional verification of information may be

required. If these trends continue after we reinstitute

foreclosure, there could be additional delays in the

process.

A discussion of credit trends in the US mortgage

lending portfolio and the steps taken to mitigate risk

is provided in ‘US personal lending – credit quality’

on page 110.

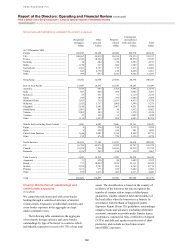

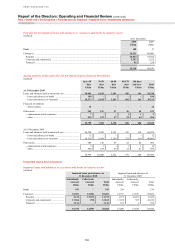

The following table shows the levels of

mortgage lending products in the various portfolios

in the US, the UK and the rest of the HSBC Group.