HSBC 2010 Annual Report Download - page 312

Download and view the complete annual report

Please find page 312 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

302 -

303

303 -

304

304 -

305

305 -

306

306 -

307

307 -

308

308 -

309

309 -

310

310 -

311

311 -

312

312 -

313

313 -

314

314 -

315

315 -

316

316 -

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

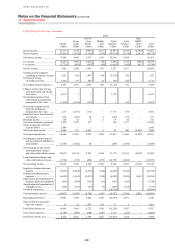

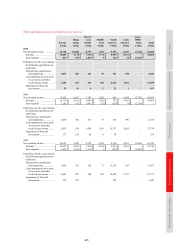

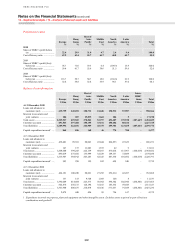

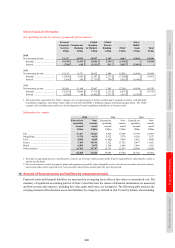

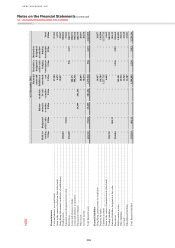

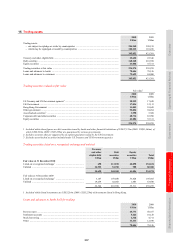

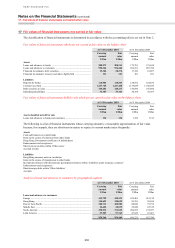

16 – Fair values of financial instruments carried at fair value

310

Valuation techniques incorporate assumptions about factors that other market participants would use in their

valuations, including interest rate yield curves, exchange rates, volatilities, and prepayment and default rates. During

the year, as a result of evolving market practice in the pricing of certain interest rate derivatives, HSBC has, for single

currency swaps with collateralised counterparties and in significant major currencies, adopted a discounting curve

that reflects the overnight interest rate (‘OIS discounting’). Previously, in line with market practice, discount curves

did not reflect this overnight interest rate component but were based on a term LIBOR rate. The financial effect of

this change was not significant.

The majority of valuation techniques employ only observable market data. However, certain financial instruments are

valued on the basis of valuation techniques that feature one or more significant market inputs that are unobservable,

and for them, the derivation of fair value is more judgemental. An instrument in its entirety is classified as valued

using significant unobservable inputs if, in the opinion of management, a significant proportion of the instrument’s

carrying amount and/or inception profit (‘day 1 gain or loss’) is driven by unobservable inputs. ‘Unobservable’ in this

context means that there is little or no current market data available from which to determine the price at which an

arm’s length transaction would be likely to occur. It generally does not mean that there is no data available at all upon

which to base a determination of fair value (consensus pricing data may, for example, be used).

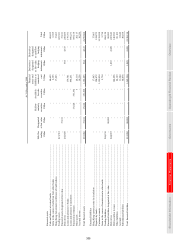

In certain circumstances, primarily where debt is hedged with interest rate derivatives, HSBC records its own debt in

issue at fair value, based on quoted prices in an active market for the specific instrument concerned, if available.

When quoted market prices are unavailable, the own debt in issue is valued using valuation techniques, the inputs for

which are either based upon quoted prices in an inactive market for the instrument, or are estimated by comparison

with quoted prices in an active market for similar instruments. In both cases, the fair value includes the effect of

applying the credit spread which is appropriate to HSBC’s liabilities. The change in fair value of issued debt

securities attributable to the Group’s own credit spread is computed as follows: for each security at each reporting

date, an externally verifiable price is obtained or a price is derived using credit spreads for similar securities for the

same issuer. Then, using discounted cash flow, each security is valued using a LIBOR-based discount curve. The

difference in the valuations is attributable to the Group’s own credit spread. This methodology is applied consistently

across all securities.

Structured notes issued and certain other hybrid instrument liabilities are included within trading liabilities and are

measured at fair value. The credit spread applied to these instruments is derived from the spreads at which HSBC

issues structured notes. These market spreads are smaller than credit spreads observed for plain vanilla debt or in the

credit default swap markets.

Gains and losses arising from changes in the credit spread of liabilities issued by HSBC reverse over the contractual

life of the debt, provided that the debt is not repaid at a premium or a discount.

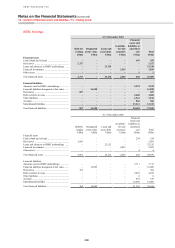

Fair value adjustments

Fair value adjustments are adopted when HSBC considers that there are additional factors that would be considered

by a market participant that are not incorporated within the valuation model. The magnitude of fair value adjustments

depends upon many entity-specific factors, and therefore fair value adjustments may not be comparable across the

banking industry.

HSBC classifies fair value adjustments as either ‘risk-related’ or ‘model-related’. The majority of these adjustments

relate to Global Banking and Markets.

Movements in the level of fair value adjustments do not necessarily result in the recognition of profits or losses

within the income statement. For example, as models are enhanced, fair value adjustments may no longer be required.

Similarly, fair value adjustments will decrease when the related positions are unwound, but this may not result in

profit or loss.