HSBC 2010 Annual Report Download - page 260

Download and view the complete annual report

Please find page 260 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

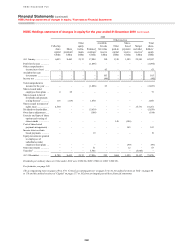

2 – Summary of significant accounting policies

258

from the realisation of security. In circumstances where the net realisable value of any collateral has been

determined and there is no reasonable expectation of further recovery, write off may be earlier.

Reversals of impairment

If the amount of an impairment loss decreases in a subsequent period, and the decrease can be related objectively

to an event occurring after the impairment was recognised, the excess is written back by reducing the loan

impairment allowance account accordingly. The write-back is recognised in the income statement.

Reclassified loans and advances

Where financial assets have been reclassified out of the fair value through profit or loss category to the loans and

receivables category, the effective interest rate determined at the date of reclassification is used to calculate any

impairment losses.

Following reclassification, where there is a subsequent increase in the estimates of future cash receipts as a result

of increased recoverability of those cash receipts, the effect of that increase is recognised as an adjustment to the

effective interest rate from the date of change in the estimate rather than as an adjustment to the carrying amount

of the asset at the date of change in the estimate.

Assets acquired in exchange for loans

Non-financial assets acquired in exchange for loans as part of an orderly realisation are recorded as assets held

for sale and reported in ‘Other assets’ if the carrying amounts of the assets are recovered principally through

sale, the assets are available for sale in their present condition and their sale is highly probable. The asset

acquired is recorded at the lower of its fair value less costs to sell and the carrying amount of the loan (net of

impairment allowance) at the date of exchange. No depreciation is charged in respect of assets held for sale. Any

subsequent write-down of the acquired asset to fair value less costs to sell is recognised in the income statement,

in ‘Other operating income’. Any subsequent increase in the fair value less costs to sell, to the extent this does

not exceed the cumulative write-down, is also recognised in ‘Other operating income’, together with any realised

gains or losses on disposal.

Renegotiated loans

Loans subject to collective impairment assessment whose terms have been renegotiated are no longer considered

past due, but are treated as up to date loans for measurement purposes once the minimum number of payments

required under the new arrangements have been received. These renegotiated loans are segregated from other

parts of the loan portfolio for the purposes of collective impairment assessment, to reflect their risk profile.

Loans subject to individual impairment assessment, whose terms have been renegotiated, are subject to ongoing

review to determine whether they remain impaired or should be considered past due. The carrying amount of

loans that have been classified as renegotiated retain this classification until maturity or derecognition. Interest is

recorded on renegotiated loans taking into account the new contractual terms following renegotiation.

(h) Trading assets and trading liabilities

Treasury bills, debt securities, equity securities, loans, deposits, debt securities in issue, and short positions in

securities are classified as held for trading if they have been acquired or incurred principally for the purpose of

selling or repurchasing in the near term, or they form part of a portfolio of identified financial instruments that

are managed together and for which there is evidence of a recent pattern of short-term profit-taking. These

financial assets or financial liabilities are recognised on trade date, when HSBC enters into contractual

arrangements with counterparties to purchase or sell the financial instruments, and are normally derecognised

when either sold (assets) or extinguished (liabilities). Measurement is initially at fair value, with transaction costs

taken to the income statement. Subsequently, the fair values are remeasured, and gains and losses from changes

therein are recognised in the income statement in ‘Net trading income’.