HSBC 2010 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

17

Overview Operating & Financial Review Governance Financial Statements Shareholder Information

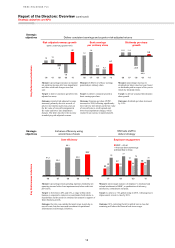

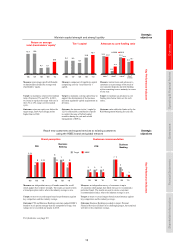

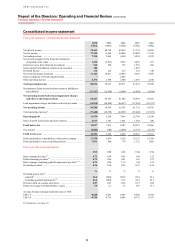

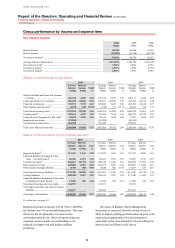

Reported profit before tax of US$19.0bn in 2010

was 169% higher than in 2009, and 36% higher on

an underlying basis. The difference between reported

and underlying results is explained on page 14.

Except where stated otherwise, the commentaries in

the Financial Summary are on an underlying basis

and references to HSBC Finance and HSBC Bank

USA are on a management basis, rather than a legal

entity basis (for details see page 37).

Net operating income before loan impairment

charges and other credit risk provisions (‘revenue’)

was lower than in 2009, notably due to a decline in

balances in North America, lower trading income

from adverse movements on non-qualifying hedges

and a fall in revenue from GB&M. In the former, we

continued to reposition our core businesses and we

remained focused on managing down our run-off

portfolios. As a consequence, revenue fell, reflecting

declining balances in the run-off portfolios and in the

Card and Retail Services business, where revenue

was also adversely affected by new regulations. In

GB&M, lower revenue was generated in Balance

Sheet Management as higher yielding positions

matured and funds were invested in lower yielding

assets. Trading income declined driven by increased

competition and reduced margins across core

products, and less favourable market conditions

caused by the European sovereign debt crisis. These

factors were partly offset by increased CMB revenue

from balance sheet growth, particularly in Asia, and

higher trade-related fees.

Loan impairment charges were significantly

lower than in 2009, with decreases across all regions

and customer groups as economic conditions

improved. The most significant decline in loan

impairment charges was in North America,

reflecting lower balances due to increased

repayments, an improvement in delinquency rates in

Card and Retail Services, and the continued run-off

of balances in the Consumer Finance business. There

were also marked declines in the Middle East and in

Latin America, primarily in Mexico and Brazil,

reflecting a reduction in personal lending balances

as selected portfolios were managed down, and an

improvement in credit quality as origination criteria

were tightened and collection practices improved. In

GB&M, loan impairment charges were significantly

lower, reflecting the improvement in the credit

environment which resulted in fewer significant

charges than those taken in 2009 in relation to a

small number of clients, notably in Europe and other

credit risk provisions fell in the available-for-sale

asset-backed securities (‘ABS’) portfolio due to a

slowing in the rate of anticipated losses in the

underlying collateral pools.

Underlying profit before tax rose by 36% as

a significant fall in impairment charges offset

a decline in revenue.

Operating expenses were higher than in 2009,

in part due to specific one-off items such as a

US$0.3bn charge for UK bank payroll tax in 2010

and the non-recurrence of a pension accounting gain

of US$0.5bn in 2009 relating to the treatment of staff

benefits. Excluding these items, operating expenses

rose in support of strategic growth initiatives in our

target markets to invest in operational infrastructure

and the selective recruitment of customer-facing

staff.

Income from associates increased, driven

by strong results in Asia which reflected robust

economic growth in mainland China.

In 2010, taxable profits were achieved in the

US, principally as the result of a gain from an

internal reorganisation that was not recognised for

accounting purposes which increased the effective

tax rate by 6.4 percentage points. If this were

excluded, the effective tax rate would be 19.1%

which is in line with our geographical range of

business activities. Reported profit after tax was

US$7.5bn higher than in 2009.