HSBC 2010 Annual Report Download - page 142

Download and view the complete annual report

Please find page 142 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

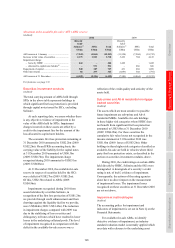

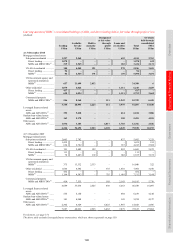

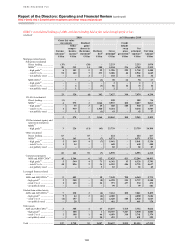

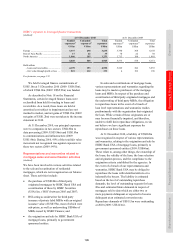

Risk > Liquidity and funding > Policies and procedures / Primary sources of funding

140

Liquidity and funding

(Audited)

HSBC expects its operating entities to manage

liquidity and funding risk on a standalone basis

employing a centrally imposed framework and limit

structure which is adapted to variations in business

mix and underlying markets. Our operating entities

are required to maintain strong liquidity positions

and to manage the liquidity profiles of their assets,

liabilities and commitments with the objective of

ensuring that their cash flows are balanced under

various severe stress scenarios and that all their

anticipated obligations can be met when due.

The objective of our liquidity framework is to

be very conservative and adaptable to

changing business models, markets and

regulation.

The objective of our liquidity and funding

management framework is to ensure that all

foreseeable funding commitments can be met when

due, and that access to the wholesale markets is

co-ordinated and cost-effective. To this end, we

maintain a diversified funding base comprising

core retail and corporate customer deposits and

institutional balances. We augment this with

wholesale funding and portfolios of highly liquid

assets diversified by currency and maturity which

are held to enable us to respond quickly and

smoothly to unforeseen liquidity requirements.

We adapt our liquidity and funding risk

management framework in response to changes

in the mix of business that we undertake, and to

changes in the nature of the markets in which

we operate. We also seek to continuously evolve

and strengthen our liquidity and funding risk

management framework. As part of this process,

we have refined the way in which we characterise

core deposits. The characterisation takes into

account the activities and operating environment in

the entity originating the deposit, the nature of the

customer and the size and pricing of the deposit.

This exercise has resulted in a revised internal

calculation of advances to core funding ratio

(discussed more fully below), and comparatives have

been restated accordingly. While total core deposits

at the Group consolidated level have not changed

materially, there have been some revisions to

individual entities.

We employ a number of measures to monitor

liquidity risk. The emphasis on the ‘ratio of net

liquid assets to customer deposits’, as reported in the

Annual Report and Accounts 2009, has been reduced

and a ‘stressed one month coverage ratio’, an

extension of our projected cash flow scenario

analysis, is now used as a simple and more useful

metric to express liquidity risk. The bank also

manages its intra-day liquidity positions so that it

is able to meet payment and settlement obligations

on a timely basis. Payment flows in real time gross

settlement systems, expected peak payment flows

and large time-critical payments are monitored

during the day and the intra-day collateral position is

managed so that there is liquidity available to meet

payments.

Policies and procedures

(Audited)

The management of liquidity and funding is

primarily undertaken locally in our operating entities

in compliance with practices and limits set by the

Risk Management Meeting. These limits vary

according to the depth and liquidity of the market in

which the entities operate. It is our policy that each

banking entity should be self-sufficient when

funding its own operations. Exceptions are permitted

for certain short-term treasury requirements and

start-up operations or for branches which do not

have access to local deposit markets. These entities

are funded from our largest banking operations and

within clearly defined internal and regulatory

guidelines and limits. The limits place formal

restrictions on the transfer of resources between our

entities and reflect the broad range of currencies,

markets and time zones within which we operate.

Elements of our liquidity and funding management process

• projecting cash flows by major currency under various

stress scenarios and considering the level of liquid assets

necessary in relation thereto;

• monitoring balance sheet liquidity and advances to core

funding ratios against internal and regulatory requirements;

• maintaining a diverse range of funding sources with back-up

facilities;

• managing the concentration and profile of debt maturities;

• managing contingent liquidity commitment exposures

within pre-determined caps;

• maintaining debt financing plans;

• monitoring depositor concentration in order to avoid undue

reliance on large individual depositors and ensure a

satisfactory overall funding mix; and

• maintaining liquidity and funding contingency plans. These

plans identify early indicators of stress conditions and

describe actions to be taken in the event of difficulties

arising from systemic or other crises, while minimising

adverse long-term implications for the business.