HSBC 2010 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

127

Overview Operating & Financial Review Governance Financial Statements Shareholder Information

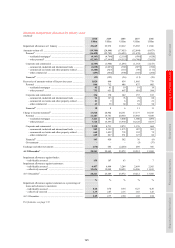

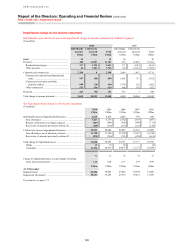

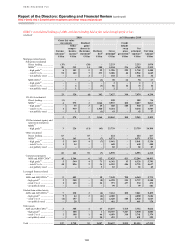

with the managing down of our exposure to higher

risk unsecured personal lending. The lower

allowances also reflected an overall improvement in

economic conditions across the region. There were

also declines in new individually assessed loan

impairment charges as new charges for 2010 were

restricted to a small number of large corporate

exposures. Impaired loans rose by 47% from

31 December 2009 to US$2.5bn due to credit

deterioration in a small number of specific

exposures, and debt restructuring in the UAE.

Releases and recoveries in the Middle East more

than doubled from 2009 to US$112m due to the

release of judgemental impairment allowances

reflecting improved economic conditions during

2010.

In North America, new loan impairment

allowances declined markedly, reducing by 44% to

US$8.7bn. In our HSBC Finance portfolios, lower

new loan impairment allowances in Card and Retail

Services reflected a reduction in lending balances

and an improvement in delinquency rates. In our

Consumer Lending and Mortgage Services

portfolios, new loan impairment allowances also fell

as the portfolio continued to run-off. In addition,

total loss severities on foreclosed loans improved

compared with 2009 reflecting the increase in the

number of properties for which we accepted a deed-

in-lieu of foreclosure, or a short sale, both of which

result in lower losses compared with loans which are

subjected to a formal foreclosure process.

In our corporate and commercial portfolios in

North America, new loan impairment allowances

declined, reflecting lower balances due to customer

deleveraging and improved credit quality which,

along with the improved economy, resulted in credit

upgrades on certain accounts and fewer customer

downgrades.

In North America, impaired loans decreased

by 19% from the end of 2009 to US$10.8bn, while

releases and recoveries rose by 80% compared with

2009 to US$378m.

In Latin America, new loan impairment

allowances declined by 42% to US$1.9bn, while

impaired loans declined by 23% to US$2.4bn as

economic conditions in the region improved. Lower

new loan impairment allowances in the personal

lending portfolios were due to lower credit card

balances in Mexico as we repositioned the portfolio

to target higher quality customers and, to a lesser

extent, in Brazil, due to the managed reduction in

consumer finance balances. In addition, in the

commercial lending portfolios in Brazil lower new

impairment allowances reflected an improvement

in economic conditions.

Releases and recoveries in Latin America

declined by 21% from 2009 to US$331m.

For an analysis of loan impairment charges and

other credit risk provisions by customer group, see

page 48.

HSBC Holdings

(Audited)

Credit risk in HSBC Holdings primarily arises from

transactions with Group subsidiaries and from

guarantees issued in support of obligations assumed

by certain Group operations in the normal conduct of

their business.

These risks are reviewed and managed within

regulatory and internal limits for exposures by our

Global Risk function, which provides high-level

centralised oversight and management of our credit

risks worldwide.

HSBC Holdings’ maximum exposure to credit

risk at 31 December 2010 is shown below. Its

financial assets principally represent claims on

Group subsidiaries in Europe and North America. No

collateral or other credit enhancements were held by

HSBC Holdings in respect of its transactions with

subsidiaries.

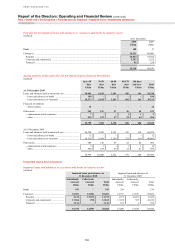

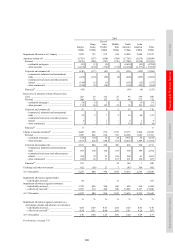

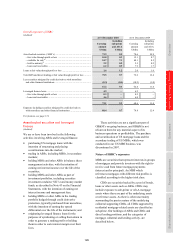

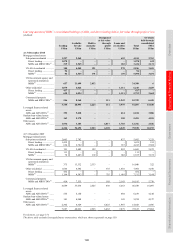

HSBC Holdings – maximum exposure to credit risk

(Audited)

2010 2009

US$m US$m

Cash at bank and in hand:

– balances with HSBC undertakings .................................................................................................... 459 224

Derivatives ................................................................................................................................................ 2,327 2,981

Loans and advances to HSBC undertakings ............................................................................................ 21,238 23,212

Financial investments ............................................................................................................................... 2,025 2,455

Financial guarantees and similar contracts .............................................................................................. 46,988 35,073

Loan and other credit-related commitments ............................................................................................ 2,720 3,240

75,757 67,185