HSBC 2010 Annual Report Download - page 113

Download and view the complete annual report

Please find page 113 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

111

Overview Operating & Financial Review Governance Financial Statements Shareholder Information

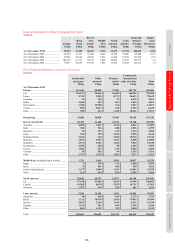

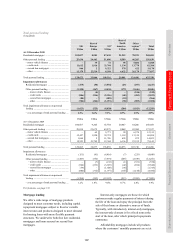

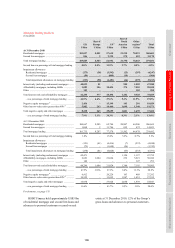

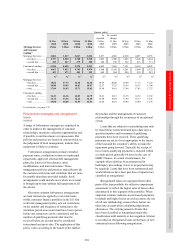

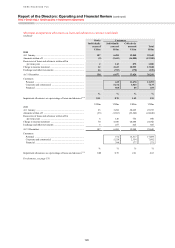

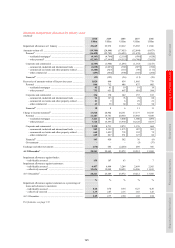

Mortgage lending

In 2010, we reduced our non-prime mortgage

exposure as balances continued to run-off in our

Consumer Lending and Mortgage Services portfolios

in HSBC Finance. At 31 December 2010, residential

mortgage lending balances were US$58bn, a decline

of 12% compared with the end of 2009.

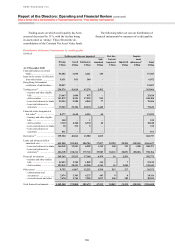

In both our Consumer Lending and Mortgage

Services mortgage portfolios, two months or more

delinquent balances declined as balances ran-off and

economic conditions improved. In addition, written-

off balances were replaced with lower levels of new

delinquency volumes as the portfolios continue to

season. First lien two months or more delinquent

balances in our Consumer Lending portfolio declined

from US$5.4bn at 31 December 2009 to US$4.9bn at

31 December 2010 and, in our Mortgage Services

portfolio, from US$3.1bn at 31 December 2009 to

US$2.8bn at 31 December 2010. In each case, lending

balances liquidated at a faster pace than delinquency.

As a result, two months or more delinquency rates on

first lien loans in our Consumer Lending portfolio

increased from 15.4% at 31 December 2009 to 16.2%,

while in our Mortgage Services portfolio, two months

or more delinquency rates increased from 16.5% to

18.0%.

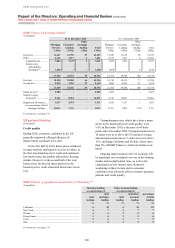

At HSBC Bank USA, we continued to sell the

majority of new mortgage loan originations to the

secondary markets. These decreases were partly offset

by increases to the portfolio from new lending to our

Premier relationship customers. Two months or more

delinquency rates decreased from 8.6% to 7.9% at

31 December 2010, while delinquent balances

remained flat at US$1.0bn.

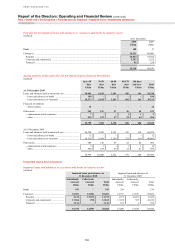

Second lien mortgage loans have a risk profile

characterised by higher loan-to-value ratios because,

in the majority of cases, the loans were taken out to

complete the refinancing or purchase of properties.

Loss experience on default of second lien loans has

typically approached 100% of the amount owed, as

any equity in the property is initially applied to the

first lien loan. In the Mortgage Services second lien

portfolio, outstanding balances declined by 26% to

US$2.3bn and two months or more delinquency rates

decreased to 10.8% at 31 December 2010. In the

Consumer Lending second lien portfolio, outstanding

balances declined by 28% to US$3.3bn, and two

months or more delinquency rates decreased to 12.7%

at 31 December 2010.

At HSBC Bank USA, second lien balances

declined by 10% to US$3.7bn, and two months or

more delinquency rates increased from 4.0% at

31 December 2009 to 4.8% at 31 December 2010 due

to the effects of high unemployment levels.

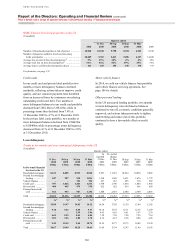

Stated-income mortgages are underwritten on the

basis of borrowers’ representations of annual income

and are not verified by supporting documents and, as

a result, represent a higher than average level of risk.

Stated income balances in HSBC Finance declined

from US$3.9bn to US$2.9bn as the portfolio

continued to run off. Two months or more

delinquency rates increased to 24.0% at 31 December

2010. In HSBC Bank USA, stated-income balances

were unchanged at US$2.1bn while delinquency rates

decreased from 11.1% at 31 December 2009 to 10.6%

at 31 December 2010.

At 31 December 2010, HSBC Finance had

US$7.6bn of affordability mortgages, a decline

of 24% compared with 31 December 2009, as the

portfolio continued to run off. At HSBC Bank USA,

affordability mortgage balances of US$10.9bn at

31 December 2010 compared with US$11.1bn at

31 December 2009.

Real estate markets in the majority of the US

have been and will continue to be, affected by

stagnation or declines in property values. As a result,

loan-to-value ratios for our real estate secured loans

have generally deteriorated since origination. Loans

with a loan-to-value of 100% or more have

historically had a greater likelihood of becoming

delinquent. At 31 December 2010 loans in negative

equity were US$14bn, compared with US$19bn at the

end of 2009.

At HSBC Finance, the number of foreclosed

properties at 31 December 2010 increased compared

with the end of 2009. The rise reflected the

improvement in the processing of foreclosures as

backlogs and action taken by local governments and

certain states had lengthened proceedings in previous

years. The average loss on sale of foreclosed

properties decreased compared with 2009 though the

average loss increased in the second half of 2010,

as house prices in many markets showed signs of

deterioration due to a rise in the number of foreclosed

properties and the expiration of the homebuyer tax

credit. We continued to assist customers in

restructuring their debts to avoid foreclosure, including

by modifying their loans when it was decided that they

could be serviced on revised terms. For more details

on the investigation into US foreclosure practices, see

page 83.