HSBC 2010 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

105

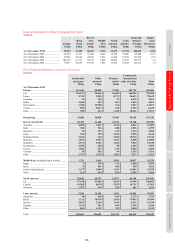

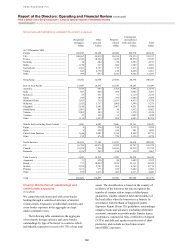

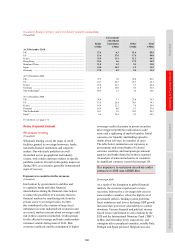

Overview Operating & Financial Review Governance Financial Statements Shareholder Information

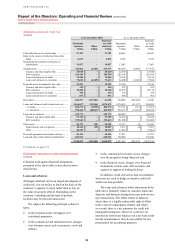

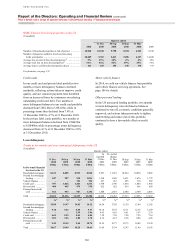

European banks

In May 2010, an FSB review indicated that European

banks would have to make additional loan impairment

charges of up to US$143bn in 2011. Following the

publication of this report, bond spreads on both

European and US banks widened. The size of the

financial sector’s exposure to sovereign debt and

doubts about economic conditions in parts of the

eurozone raised fresh concerns about banks’ credit

ratings. In addition, uncertainty over liquidity,

solvency, funding, changing regulation, capital

requirements and taxation, and speculation over the

stability of the euro, continued to cloud the future for

European banking.

The banking sector in the eurozone remains

under stress, mainly as a consequence of

governments having to finance large budget deficits,

troubles in property markets and weak credit growth.

The Ireland bailout was a direct consequence of the

failure of the Irish banking sector, largely driven by

the domestic property price crash. Worries about the

size and quality of eurozone banks’ exposure to

weaker eurozone countries are entwined with

concerns about their ability to fund themselves.

European banks share nearly three quarters of the

public and private sector debt in Belgium, Greece,

Ireland, Italy, Portugal and Spain. The regional and

local banks in the eurozone are considered more

vulnerable than well-diversified global banks.

During 2010, we were subject to the Committee

of European Banking Supervisors (now the European

Banking Authority) coordinated stress test of 91 EU

financial institutions. Banks were required to meet a

6% minimum tier 1 target under stress. We passed the

test satisfactorily, with a post-stress tier 1 ratio of

10.2% placing us in the top quartile of the institutions

tested. Further stress testing is due to take place in

2011.

We expect that the pace of reforms outlined

by various policymakers will gather speed in 2011,

most notably the Basel III proposals. These regulations

will require banks to hold more capital and a higher

quality of capital and implement new liquidity rules,

and are likely to result in a rise in the cost of funding

and put pressure on credit pricing.

We continue to closely monitor and manage

eurozone bank exposures, and are cautious in lending

to this sector. We regularly update our assessment of

higher-risk eurozone banks and adjust our risk appetite

accordingly. We also, where possible, seek to play a

positive role in maintaining credit and liquidity supply.

Middle East and North Africa

In 2009, Dubai World requested a standstill agreement

with creditors in respect of the indebtedness of certain

Dubai World group companies. The market disruption

that ensued cut would-be borrowers off from the

capital markets, although continued restructuring

efforts throughout 2010 saw the return of significant

positive sentiment from investors. As one of the long-

term bankers to Dubai World and the various entities

related to the Government of Dubai, the Group has

worked closely during 2010 to address the prevailing

issues. In October 2010, Dubai World obtained an

agreement to restructure US$25bn of its debt subject

to final documentation expected to be signed in the

first half of 2011. The arrangement extends loan

maturities for five to eight years at discounted rates,

allowing Dubai World time to sell off its non-core

assets while focusing on its core earnings. The

Group’s exposure to Dubai is primarily spread across

operating companies within the emirate.

Political developments in the region are being

monitored closely and action taken to mitigate their

impact. It is too early to foresee how events may

unfold; hitherto, our business in the region has for

the most part operated without serious disruption. In

the medium term, economic growth in the region

may be adversely affected, with wider implications

if the prices of oil, food and commodities rise

significantly.

Commercial real estate

Our exposure in the commercial real estate sectors is

concentrated in the UK, North America and Hong

Kong. While there were some positive signs of

recovery in markets in the UK and the US, in part

supported by the low levels of interest rates, the

slow speed of the recovery meant that financing and

re-financing activity in the sector remained subdued.

In Hong Kong, the economy recovered robustly

and the market was relatively buoyant in 2010,

characterised by strong demand and continuing

credit appetite.

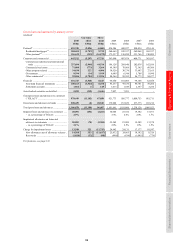

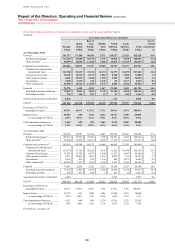

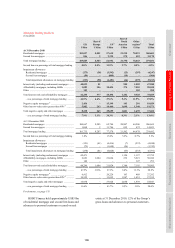

On a constant currency basis, the aggregate of

our commercial real estate and other property-related

lending of US$107bn at 31 December 2010 was 7%

higher than at 31 December 2009 and represented

11% of total loans and advances to customers. The

increase in exposure was largely in Hong Kong,

offset by a reduction in North America. In 2010,

credit quality across this sector generally showed

signs of stabilising but remained under stress in

certain markets.