HSBC 2010 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

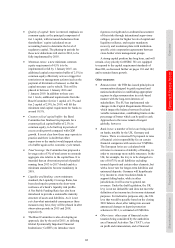

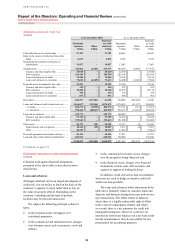

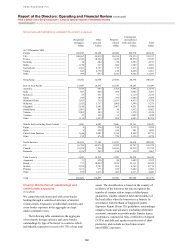

Risk > Credit risk > Credit exposure

98

Derivatives

(Unaudited)

Derivative assets at 31 December 2010 were

US$261bn, a rise of 4% from 31 December 2009.

Our single largest exposure was to interest rate

derivatives, and this balance increased in 2010

reflecting downward shifts in yield curves, partly

offset by higher netting from increased trading with

clearing houses. The notional value of outstanding

contracts also rose, reflecting an increase in the

number of open transactions compared with 2009. In

addition our exposure to exchange rate derivatives

rose as a result of increased volatility.

Loans and advances

(Unaudited)

On a reported basis, gross loans and advances to

customers (excluding the financial sector) at

31 December 2010 increased by US$52bn or 6%

from 31 December 2009. On a constant currency

basis the increase was 7%. The rise was primarily

due to growth in Asia, mainly in trade-related

lending and, to a lesser extent, our commercial real

estate and personal lending portfolios, as the region

prospered.

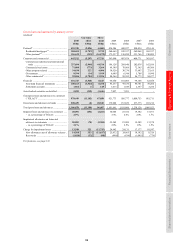

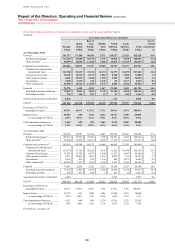

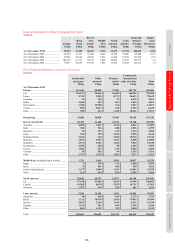

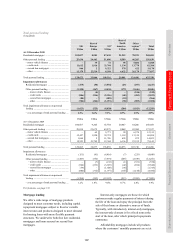

Summary of gross loans and advances to customers

(Unaudited)

425 446

102

6

434

383

97

8

0

100

200

300

400

500

Personal Corporate and

commercial

Financial ABSs

reclassified

2010 2009

(US$bn)

Reported basis

The following commentary is on a constant

currency basis:

Personal lending was US$425bn, a decline of

2% compared with the end of 2009 as growth in

residential mortgage lending was more than offset

by lower other personal lending balances. Personal

lending represented 43% of our total lending to

customers. At US$269bn, residential mortgage

lending constituted the Group’s largest concentration

in a single exposure type. In 2010, residential

mortgage lending increased by 4%, reflecting strong

growth in new mortgage sales in Hong Kong and the

UK. This was partly offset by a 12% decline in the

US, mainly due to the continued run-off of our

Consumer Lending and Mortgage Services

portfolios.

Corporate and commercial lending was 46%

of gross lending to customers at 31 December

2010, comprising our largest lending category.

Commercial, industrial and international trade

represented the largest portion of this category and

this increased by 23% in the year, reflecting the

growth in trade activity, particularly in Asia.

Commercial real estate lending, which represented

7% of total gross lending to customers, increased by

5% due to strong growth in Hong Kong.

In the financial category, our largest exposure

was to non-bank financial institutions; this largely

comprised secured lending on trading accounts,

mainly repo facilities.

Loans and advances to banks were widely

distributed across major institutions in 2010 and

increased by 16% as placements with central

and commercial banks in Europe, Asia and Latin

America rose.

The following tables analyse loans by industry

sector and by the location of the principal operations

of the lending subsidiary or, in the case of the

operations of The Hongkong and Shanghai Banking

Corporation, HSBC Bank, HSBC Bank Middle East

and HSBC Bank USA, by the location of the lending

branch.