HSBC 2010 Annual Report Download - page 144

Download and view the complete annual report

Please find page 144 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Risk > Liquidity and funding > The management of liquidity risk / Contingent liquidity risk

142

according to their contractual maturities. The

undiscounted cash flows potentially payable under

financial guarantees and similar contracts are

classified on the basis of the earliest date they can be

called.

Cash flows payable in respect of customer

accounts are primarily contractually repayable on

demand or at short notice. However, in practice, short-

term deposit balances remain stable as inflows and

outflows broadly match and a significant portion of

loan commitments expire without being drawn upon.

The management of liquidity risk

(Audited)

We use a number of principal measures to manage

liquidity risk, as described below.

Advances to core funding ratio

We emphasise the importance of core customer

deposits as a source of funds to finance lending to

customers, and discourage reliance on short-term

professional funding. This is achieved by placing

limits on banking entities which restrict their ability

to increase loans and advances to customers without

corresponding growth in their core customer deposits

or long-term debt funding. This measure is referred

to as the ‘advances to core funding’ ratio. Previously,

we utilised the ‘advances to deposits’ ratio.

Advances to core funding ratio limits are set

by the Risk Management Meeting and monitored by

Group Finance. The ratio expresses current loans and

advances to customers as a percentage of the total of

core customer deposits and term funding with a

remaining term to maturity in excess of one year.

Loans and advances to customers which are part of

reverse repurchase arrangements, and where we

receive securities which are deemed to be liquid, are

excluded from the advances to core funding ratio.

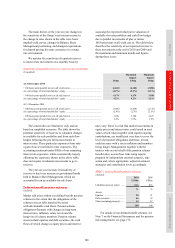

The three principal banking entities listed in the

table below represented 62% of our total core

deposits at 31 December 2010 (31 December 2009:

63%). The table shows that loans and advances to

customers in our principal banking entities are

overwhelmingly financed by reliable and stable

sources of funding. We would meet any unexpected

net cash outflows by selling securities and accessing

additional funding sources such as interbank or

collateralised lending markets.

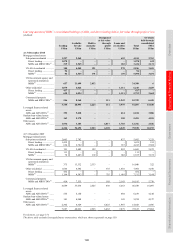

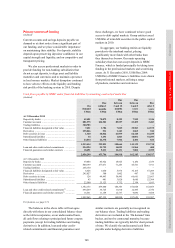

HSBC’s principal banking entities – the management of liquidity risk

(Audited)

Advances to core funding

ratio during:

Stressed one month coverage

ratio during:

2010

2009

2010

2009

%

%

%

%

HSBC Bank plc55

Year-end ................................................................................ 103.0

105.0

111.1

103.2

Maximum ............................................................................. 109.7

116.0

111.3

108.1

Minimum .............................................................................. 102.6

105.0

103.2

101.3

Average ................................................................................. 106.0

110.6

108.2

103.9

The Hongkong and Shanghai Banking Corporation55

Year-end ................................................................................ 70.3

55.5

144.6

153.2

Maximum ............................................................................. 70.3

62.0

165.4

153.2

Minimum .............................................................................. 55.5

55.5

132.6

134.3

Average ................................................................................. 63.6

57.5

148.8

144.8

HSBC Bank USA

Year-end ................................................................................ 98.3

101.0

108.5

105.3

Maximum ............................................................................. 104.3

111.1

118.5

128.0

Minimum .............................................................................. 94.2

99.5

105.3

105.3

Average ................................................................................. 98.0

106.1

112.3

118.7

Total of HSBC’s other principal banking entities56

Year-end ................................................................................ 89.1

85.9

119.6

124.8

Maximum ............................................................................. 89.1

89.2

126.5

124.8

Minimum .............................................................................. 85.7

81.2

118.1

116.3

Average ................................................................................. 87.0

85.9

122.2

120.5

For footnotes, see page 174.

Stressed one month coverage ratio

The stressed one month coverage ratios tabulated

above are derived from these scenario analyses, and

express the stressed cash inflows as a percentage of

stressed cash outflows over a one month time

horizon. Our entities are required to target a ratio

of 100% or greater.

Projected cash flow scenario analysis

We use a number of standard projected cash flow