HSBC 2010 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

137

Overview Operating & Financial Review Governance Financial Statements Shareholder Information

Student loan-related assets

Our holdings in student loan-related assets were

US$5.5bn (2009: US$5.1bn). No impairments were

recorded on student loan-related assets in 2010

(2009: nil).

Transactions with monoline insurers

(Audited)

HSBC’s exposure to derivative transactions

entered into directly with monolines

Our principal exposure to monolines is through a

number of OTC derivative transactions, mainly

credit default swaps (‘CDS’s). We entered into these

CDSs primarily to purchase credit protection against

securities held at the time within the trading

portfolio.

During 2010, the notional value of derivative

contracts with monolines and our overall credit

exposure to monolines decreased as a number of

transactions were commuted, others matured, and

credit spreads narrowed. The table below sets out the

fair value, essentially the replacement cost, of the

remaining derivative transactions at 31 December

2010, and hence the amount at risk if the CDS

protection purchased were to be wholly ineffective

because, for example, the monoline insurer was

unable to meet its obligations. In order to further

analyse that risk, the value of protection purchased

is shown subdivided between those monolines

that were rated by S&P at ‘BBB- or above’ at

31 December 2010, and those that were ‘below

BBB–’ (BBB– is the S&P cut-off for an investment

grade classification). The ‘Credit risk adjustment’

column indicates the valuation adjustment taken

against the net exposures, and reflects our best

estimate of the likely loss of value on purchased

protection arising from the deterioration in

creditworthiness of the monolines. These valuation

adjustments, which reflect a measure of the

irrecoverability of the protection purchased, have

been charged to the income statement. During 2010,

the credit risk adjustment on derivative contracts

with monolines decreased as a number of

transactions commuted and others matured.

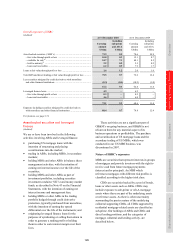

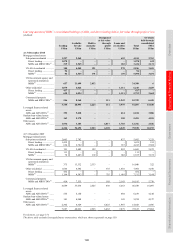

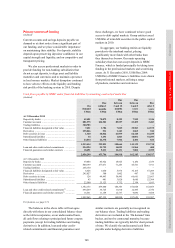

HSBC’s exposure to derivative transactions entered into directly with monoline insurers

(Audited)

Notional

amount

Net exposure

before credit

risk adjustment51

Credit risk

adjustment52

Net exposure

after credit

risk adjustment

US$m US$m US$m US$m

At 31 December 2010

Derivative transactions with monoline counterparties

Monoline – investment grade (BBB– or above) .............. 5,179 876 (88) 788

Monoline – sub-investment grade (below BBB–) ........... 2,290 648 (431) 217

7,469 1,524 (519) 1,005

At 31 December 2009

Derivative transactions with monoline counterparties

Monoline – investment grade (BBB– or above) .............. 5,623 997 (100) 897

Monoline – sub-investment grade (below BBB–) ........... 4,400 1,317 (909) 408

10,023 2,314 (1,009) 1,305

For footnotes, see page 174.

The above table can be analysed as follows.

HSBC has derivative transactions referenced to

underlying securities with a notional value of

US$7.5bn (2009: US$10.0bn), whose value at

31 December 2010 indicated a potential claim

against the protection purchased from the

monolines of some US$1.5bn (2009: US$2.3bn).

On the basis of a credit assessment of the

monolines, a provision of US$519m has been taken

(2009: US$1.0bn), leaving US$1.0bn exposed

(2009: US$1.3bn), of which US$788m is

recoverable from monolines rated investment grade

at 31 December 2010 (2009: US$897m). The

provisions taken imply in aggregate that 90 cents in

the dollar will be recoverable from investment

grade monolines and 33 cents in the dollar from

non-investment grade monolines (2009: 90 cents

and 31 cents, respectively).

For the CDSs, market prices are generally not

readily available. Therefore the CDSs are valued on

the basis of market prices of the referenced

securities.

The credit risk adjustment against monolines is

determined by one of a number of methodologies,

dependent upon the internal credit rating of the

monoline. Our assignment of internal credit ratings

is based upon detailed credit analysis, and may

differ from external ratings.