ADT 2011 Annual Report Download - page 126

Download and view the complete annual report

Please find page 126 of the 2011 ADT annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

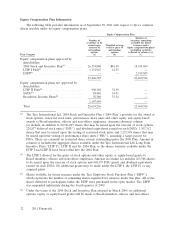

|

|

Examinations and audits by tax authorities, including the Internal Revenue Service, could result in

additional tax payments for prior periods.

The Company and its subsidiaries’ income tax returns periodically are examined by various tax

authorities. In connection with these examinations, tax authorities, including the IRS, have raised issues

and proposed tax adjustments, in particular, with respect to tax years preceding the 2007 Separation.

We are reviewing and contesting certain of the proposed tax adjustments. Although we expect to

resolve a substantial number of the proposed tax adjustments with the IRS, a few significant items are

expected to remain open with respect to the audit of the 1997 through 2004 years. As of the date

hereof, it is unlikely that we will be able to resolve these open items, which primarily involve the

treatment of certain intercompany transactions during the period related to the audits, through the IRS

appeals process. As a result, we may be required to litigate these matters. The calculation of our tax

liabilities involves dealing with uncertainties in the application of complex tax regulations in a multitude

of jurisdictions across our global operations. We recognize potential liabilities and record tax liabilities

for anticipated tax audit issues in the United States and other tax jurisdictions based on our estimate of

whether, and the extent to which, additional income taxes will be due. These tax liabilities are reflected

net of related tax loss carryforwards. We adjust these liabilities in light of changing facts and

circumstances. We have assessed our obligations under the Tax Sharing Agreement and determined that

the recorded liability is sufficient to cover the indemnifications made by us under such agreement.

However, such amount could differ materially from amounts that are actually determined to be due,

and any such difference could materially adversely affect our financial position, results of operations or

cash flows.

If the distribution of Covidien and TE Connectivity common shares to our shareholders or certain

internal transactions undertaken in connection with the 2007 Separation are determined to be taxable for U.S.

federal income tax purposes, we could incur significant U.S. federal income tax liabilities.

We have received private letter rulings from the IRS regarding the U.S. federal income tax

consequences of the distribution of Covidien and TE Connectivity common shares to our shareholders

substantially to the effect that the distribution of such shares, except for cash received in lieu of

fractional shares, will qualify as tax-free under Sections 355 and 368(a)(1)(D) of the Code. The private

letter rulings also provided that certain internal transactions undertaken in anticipation of the

2007 Separation would qualify for favorable treatment under the Code. The private letter rulings relied

on certain facts and assumptions, and certain representations and undertakings, from Tyco, Covidien

and TE Connectivity regarding the past and future conduct of our respective businesses and other

matters. Notwithstanding the private letter rulings and the opinions, the IRS could determine on audit

that the distribution or the internal transactions should be treated as taxable transactions if it

determines that any of these facts, assumptions, representations or undertakings are not correct or have

been violated, or that the distributions should be taxable for other reasons, including as a result of

significant changes in stock or asset ownership after the distribution. If the distribution ultimately is

determined to be taxable, we would recognize a gain in an amount equal to the excess of the fair

market value of the Covidien and TE Connectivity common shares distributed to our shareholders on

June 29, 2007 over our tax basis in such common shares, but such gain, if recognized, generally would

not be subject to U.S. federal income tax. However, we would incur significant U.S. federal income tax

liabilities if it ultimately is determined that certain internal transactions undertaken in connection with

the 2007 Separation should be treated as taxable transactions.

2011 Financials 23