Travelers 2006 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2006 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

|

|

22

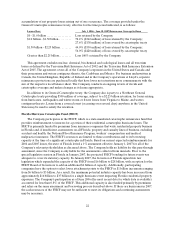

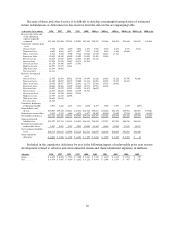

accumulation of net property losses arising out of one occurrence. The coverage provided under the

General Catastrophe reinsurance treaty, effective for the time period indicated, is as follows:

Layer of Loss July 1, 2006 - June 30, 2007 Reinsurance Coverage In-Force

$0 - $1.0 billion .................. Loss retainedby the Company

$1.0 billion - $1.50 billion .........72 .4% ($362 million) of loss retained by the Company;

27.6% ($138 million) of loss covered by catastrophe treaty

$1.50 billion - $2.25 billion ........ 44.0% ($330 million) of loss retained by the Company;

56.0% ($420 million) of loss covered by catastrophe treaty

Greater than $2.25 billion. ........ Loss 100% retained by theCompany

This agreement excludes nuclear, chemical, biochemical and radiological losses and all terrorism

losses as defined by the Terrorism Risk Insurance Act of 2002 and the Terrorism Risk Insurance Extension

Act of 2005. The agreement covers all of the Company’s exposures in the United States and Canada and

their possessions and waters contiguous thereto, the Caribbean and Mexico. For business underwritten in

Canada, the United Kingdom, Republic of Ireland and in the Company’s operations at Lloyd’s, separate

reinsurance protections are purchased locally that have lower net retentions more commensurate with the

size of the respective local balance sheet.The Company conducts an ongoing review of i ts risk and

catastrophe coverages andmakes changes as it deems appropriate.

In addition to its General Catastrophe treaty, the Company also is party to a Northeast General

Catastrophe treaty providing $500 million of coverage, subject to a $2.25 billion retention, for losses arising

from hurricanes, earthquakes and winter storm or freeze losses from Virginia to Maine, and waters

contiguous thereto. Losses from a covered event (occurring over several days) anywhere in the United

States may beused to satisfy the retention.

Florida Hurricane Catastrophe Fund (FHCF)

The Company participates in the FHCF, which is a state-mandated catastrophe reinsurance fund that

provides reimbursement to insurers for a portion of their residential catastrophic hurricane losses. The

FHCF isprimarily funded by premiums from insurance companies that write residential property business

in Florida and, if insufficient, assessments on all Florida property and casualty lines of business, excluding

accident and health, the National Flood Insurance Program, workers’ compensation and medical

malpractice insurance. The FHCF’s resources are limited to these contributions and to its borrowing

capacity at the time of a significant catastrophe in Florida. Based on current expected reimbursements for

2004 and 2005 losses, the state of Florida levied a 1% assessment effective January 1, 2007 for all of the

Company’s relevant policyholders as discussed above. The Company holds no liability for this pass-through

assessment, since the Company is only liable for the assessments collected from insureds. Prior to the

special legislative session in Florida in January 2007, the projected FHCF bonding for future events was

adequate to cover its statutory capacity. In January 2007, the Governor of Florida signed into law

legislation which expanded the capacity of the FHCF from $16 billion to $28 billion, with an option for the

FHCF Board of Governors to add an additional$4 billion of capacity. Additionally, participating

companies have the option to select lower attachment points to the FHCF in $1 billion increments ranging

from $6 billion to$3 billion. As a result, the maximum potential industry capacity has been increased from

approximately $16 billion to $35 billion for a single hurricane event impacting Florida residential property

exposures. The Company’s participation as of June 2006 (the most recent date for which data is available)

accounted for less than 0.8% of the FHCF. This additional capacity is also funded primarily by premiums

and relies on the same assessment and borrowing process described above. If there are hurricanes in 2007,

the cash resources of the FHCF may not be sufficient to meet its obligations and continuing assessments

may be necessary.