Travelers 2006 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2006 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

|

|

117

severity of individual claims, the determination of occurrence date for a claim and reporting lags (the time

between the occurrence of the policyholder event and when it is actually reported to the insurer). Informed

judgment is applied throughout the process. The Company continually refines its loss reserve estimates in a

regular ongoing process as historical loss experience develops and additional claims are reported and

settled. The Company rigorously attempts to consider all significant facts and circumstances known at the

time loss reserves are established. Due to the inherent uncertainty underlying loss reserve estimates

including but not limited to the future settlement environment, final resolution of the estimated liability

will be different from that anticipated at the reporting date. Therefore, actual paid losses in the future may

yield a materially different amountthan currently reserved—favorable or unfavorable.

Becauseestablishment of loss reserves is an inherently uncertain process involving estimates, currently

established reserves may change. The Company reflects adjustments to reserves in the results of operations

in the period the estimates are changed.

There are also risks which impact the estimation of ultimate costs for catastrophes. For example, the

estimation of reserves related to hurricanes can be affected by the inability by the Company and its

insureds to access portions of the impacted areas, the complexity of factors contributing to the losses, the

legal and regulatory uncertainties and the nature of the information available to establish the reserves.

Complex factors include, but are not limited to, determining whether damage was caused by flooding

versus wind; evaluating general liability andpollution exposures; estimating additional living expenses; and

estimating the impact of demand surge, infrastructure disruption, fraud, theeffect of mold damage and

business interruption costs and reinsurance collectibility. The timing of a catastrophe’s occurrence, such as

at or near the end of a reporting period, can also affect the information available to us in estimating

reserves for that reporting period. The estimates related to catastrophes are adjusted as actual claims

emerge.

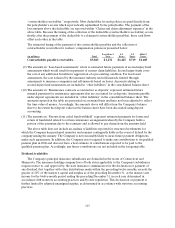

A portion of the Company’s loss reserves are for asbestos and environmental claims and related

litigation which totaled $4.47 billion at December 31, 2006. While the ongoing study of asbestos claims and

associated liabilities and of environmental claims considers theinconsistencies of court decisions as to

coverage, plaintiffs’ expanded theories of liability and the risks inherent in complex litigation and other

uncertainties, in the opinion of the Company’s management, it is possible that the outcome of the

continued uncertainties regarding these claims could result in liability in future periods that differs from

current reserves by an amount that could be material to the Company’s future operating results. See the

preceding discussion of “Asbestos Claims and Litigation” and “Environmental Claims and Litigation.”

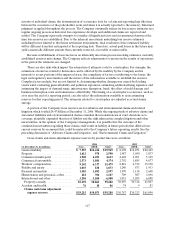

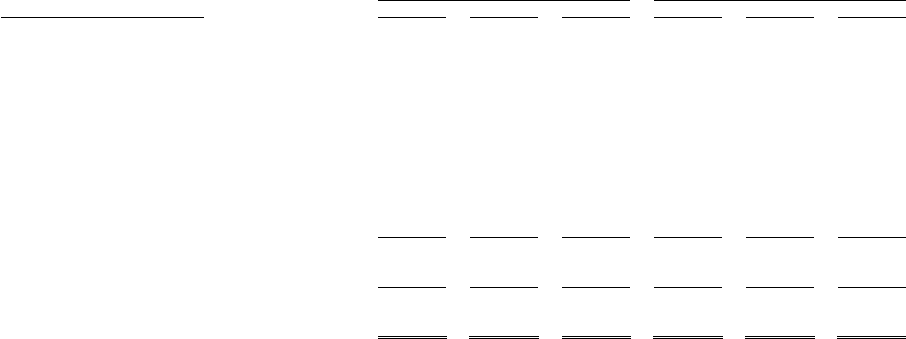

Gross claims and claim adjustment expense reserves by product line were as follows:

2006 2005

(at December 31, in millions) Case IBNR TotalCase IBNR Total

General liability ..................... $ 7,555 $12,414 $ 1 9,969 $ 8,198 $12,251 $20,449

Property ............................ 1,612 978 2,590 1,987 1,050 3,037

Commercial multi-peril............... 1,940 2,693 4,633 2,448 2,901 5,349

Commercial automobile .............. 2,573 1,801 4,374 2,792 1,885 4,677

Workers’ compensation. .............. 9,142 6,33715,479 8,816 6,374 15,190

Fidelity and surety ................... 1,035 838 1,873 1,240 673 1,913

Personal automobile................. 1,505 1,092 2,597 1,470 1,138 2,608

Homeowners and personal—other ..... 481 706 1,187 709 987 1,696

International and other ............... 3,296 3,204 6,500 3,033 3,055 6,088

Property-casualty .................. 29,139 30,063 59,202 30,693 30,314 61,007

Accident and health .................. 76 10 86 74 9 83

Claims and claim adjustment

expense reserves................. $ 2 9,215 $30,073 $ 5 9,288 $30,767 $ 30,323 $ 61,090