Travelers 2006 Annual Report Download - page 200

Download and view the complete annual report

Please find page 200 of the 2006 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

|

|

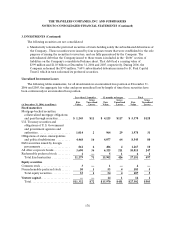

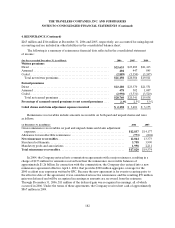

THE TRAVELERS COMPANIES, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

188

6. INSURANCE CLAIM RESERVES (Continued)

changes in claim handling practices. These changes included practices which have allowed case reserves to

be established more accurately earlier in the claim settlement process, thereby changing historical loss

development patterns. In addition, industry and Company initiatives to fight fraud in several states led to a

decrease in the total number of claims and a change in historical loss development patterns. In the

Homeowners and Other line of business, favorable prior year reserve development was partially driven by

a significant decrease in the number of claims, attributable to changes in the marketplace, including higher

deductibles and fewer small-dollar claims. These changes also resulted in a change in historical loss

development patterns. In addition, non-catastrophe Homeowners and Other loss experience was favorable

due to continued evidence of a less than expected impact from “demand surge,” which refers to significant

short-term increases in building material and labor costs due to a sharp increase in demandfor those

materials and services. Included in net favorable prior year reserve development in 2006 was a reduction in

loss estimates for catastrophes incurred in 2005, primarily due to lower than expected additional living

expense losses related to Hurricane Katrina.

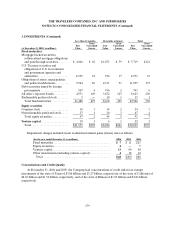

2005.

In 2005, estimated claims and claim adjustment expenses for claims arising in prior years totaled a net

$260 million, including $325 million of net unfavorable prior year reserve developmentimpacting the

Company’s results of operations which excludes $59 million of accretion ofdiscount. In 2005, estimated

claims and claim adjustment expenses for claims arising in prior years included $30 million of net favorable

loss development on Business Insurance loss sensitive policies in various lines; however, since the business

to which itrelates was subject to premium adjustments, there was no impact on results of operations.

Business Insurance. Net unfavorable prior year reserve development in 2005 was $757 million, which

included the asbestos and environmental changes that are discussed in more detail in the following

“Asbestos and Environmental Reserves” section, and reserve strengthening for assumed reinsurance,

which is in runoff. Those increases were partially offset by favorable prior year reserve development from

lower frequency and severity for both casualty and property-related lines of business. Drivers of the

reduction in both frequency and severity were increasingly favorable legal and judicial environments,

coupled with better than expected results from changes in policy provisions as well as underwriting and

pricing criteria. Company initiatives relating to claims handling, which affected claims staffing and

workflows, also are believed to have contributed to the emergence of favorable severity experience in 2005.

Financial, Professional & International Insurance.Net favorable prior year reserve development

totaled $72 million in 2005, attributable to the better than anticipated favorable impact from changes in

underwriting and pricing strategies for International property-related exposures.

Personal Insurance.Net favorable prior year reserve development in 2005 totaled $360 million. In

the automobile line of business, the improvement was driven by betterthan expected results from changes

in claim handling practices. These changes included practices which have allowed case reserves to be

established more accurately earlier in the claim settlement process, thereby changing historical loss

development patterns. In addition, both industry and internal initiatives to fight fraud in several states

caused a decrease in the total number of claims, as well as a change in the historical loss development

patterns. In the homeowners line of business, the improvement was driven primarily by a significant

decrease in the number of claims, attributable to changes in the marketplace, including higher deductibles