Travelers 2006 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2006 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

|

|

91

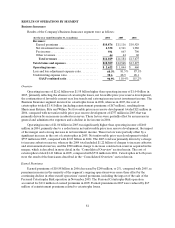

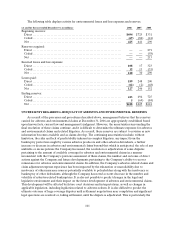

Earned Premiums

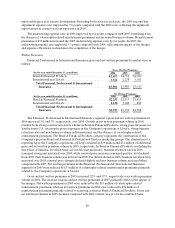

Earned premiums of $6.56billion in 2006 increased 9% over the 2005 total of $6.03 billion, primarily

due to significant new business volume, renewal price increases and continued strong business retention

rates over the prior twelve months. Earned premiums in 2005 were reduced by $21 million of catastrophe-

related reinstatement premiums. Earnedpremiums of $6.03 billion in 2005 increased $448 million, or 8%,

over 2004 earned premiums of $5.58 billion, reflecting continued strong business retention levels, new

business volumes and renewal price increases over the prior twelve months.

Net Investment Income

Refer to the “Net Investment Income” section of the “Consolidated Results of Operations” discussion

herein for a description of the factors contributing to the increase in the Company’s net investment income

in 2006 and 2005.

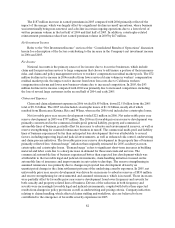

Claims and Expenses

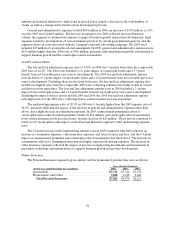

Claims and claim adjustment expenses in 2006 totaled $3.60 billion, compared with $3.75 billion in

2005. The $154 million decline primarily reflected a reduction in catastrophe losses, which was partially

offset by the impact of higher business volume in 2006. Catastrophe losses totaled $103 million in 2006,

down significantly from the 2005 total of $547 million.

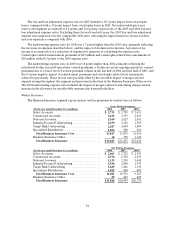

Net favorable prior year reserve development in 2006 and 2005 was $359 million and $360 million,

respectively. The net favorable prior year reserve development in 2006 was driven by better than expected

loss experience in the auto bodily injury andnon-catastrophe related Homeowners and Other lines of

business, and a reduction in loss estimates for the 2005 hurricanes. In the Automobile line of business, for

2006 and 2005, the improvement was partially driven by better than expected results from changes in claim

handling practices. These changes included practices which have allowed case reserves to be established

more accurately earlier in the claim settlement process, thereby changinghistorical loss development

patterns. In addition, for both years, industry and Company initiatives to fight fraud in several states led to

a decrease in the total number of claims and a change in historical loss development patterns. In the

Homeowners and Other line of business, favorable prior year reserve development in 2006 and 2005 was

partially driven by a significant decrease in the number of claims, attributable to changes in the

marketplace, including higher deductibles and fewer small-dollar claims. These changes also resulted in a

change in historical loss development patterns. In addition, for 2006, non-catastrophe related Homeowners

and Other loss experience was favorable due to continued evidenceof a less than expected impact from

“demandsurge,” which refers to significant short-term increases in building material and labor costs due to

a sharp increase in demand for those materials and services. Approximately $100 million of net favorable

prior year reserve development in 2006 resulted from a reduction in loss estimates for catastrophes

incurred in2005, primarily due to lower than expected additional living expense losses related to

Hurricane Katrina.

In 2005, claims and claim adjustment expenses included catastrophe losses of $547 million, compared

with $189 million in 2004. Catastrophe losses in both years were primarily the result of hurricanes. Net

favorable prior year reserve development in 2005 was $360 million, as described above, compared with net

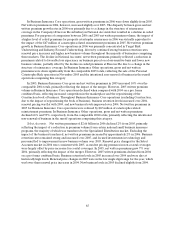

favorable prior year reserve development of $378 million in 2004. In 2004, net favorable prioryear reserve

developmentin theHomeowners and Other line of business was driven by a significant decrease in the

number of claims, attributable to changes in the marketplace, including higher policy deductible levels and

fewer small-dollar claims. These changes resulted in a change in the historical loss development patterns.

Net favorable prior year reserve development in the Automobile line of business was driven by better than

expected frequency andseverity which is believed to have been caused by societal trends. In addition, both