Travelers 2006 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2006 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

|

|

15

customer relationships, as well as its ability to offer its customers a full range ofproducts, provides Bond &

Financial Products an advantage over many of its competitors and enables it to compete effectively in a

complex, dynamic marketplace. The ability of Bond & Financial Products to cross-sell its products to

customers of the Business Insurance and Personal Insurance segments provides further competitive

advantages for the Company.

International competes with numerous international and local country insurers in the United

Kingdom, Canada and the Republic of Ireland.Companies compete on the basis of price,product

offerings and the level of claim and risk management services provided. The Company has developed

expertise in various markets in these countries similar to those served in the United States and provides

both property and casualty coverage for these markets. Products are generally distributed through a

relatively small broker base whose customer groups align with the Company’s targeted markets.

At Lloyd’s, the Company competes with other syndicates operating in the Lloyd’s market as well as

international and domestic insurers in the various markets where the Company writes business worldwide.

Lloyd’s syndicates are increasingly capitalized by corporate capital, much of which is provided by large

international insurance enterprises. Competition is again based on price and product offerings. The

Company has an exclusive focus on lines it believes it can underwrite effectively and profitably with an

emphasis on short-tail insurance lines. The Company underwrites through four principal lines of business

at Lloyd’s: aviation, marine,global property, and accident andspecial risks.

PERSONAL INSURANCE

Personal Insurance writes virtually all types of property and casualty insurance covering personal risks.

The primary coverages in Personal Insurance are automobile and homeowners insurance sold to

individuals. These products are distributed through independent agents, sponsoring organizations such as

employee and affinity groups, and joint marketing arrangements with other insurers.

In January 2007, the Company reached a definitive agreement to sell its subsidiary, Mendota

Insurance Company and its wholly-owned subsidiaries, Mendakota Insurance Company and Mendota

Insurance Agency, Inc. These subsidiaries primarily offered nonstandard automobile coverage and

accounted for approximately $187 million of net written premium volume in 2006. The sale is not expected

to be material to the Company’s results of operations orfinancial condition.

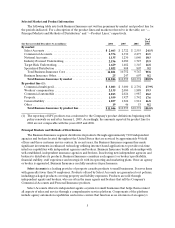

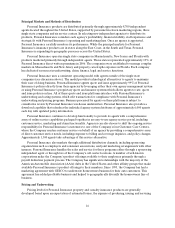

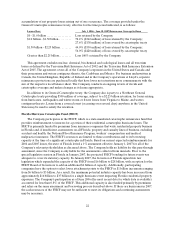

Selected Product and Distribution Channel Information

The following table sets forth net written premiums for Personal Insurance by product line for the

periods indicated. For a description of the product lines referred to in the accompanying table, see “—

Product Lines.” In addition, see “—Principal Markets and Methods of Distribution” for a discussion of

distribution channels for Personal Insurance’s product lines.

(for the year ended December 31, in millions) 2006 2005 2004

% of Total

2006

By product line:

Personal automobile............................. $ 3 ,692 $ 3 ,477 $3,433 55.0 %

Homeowners and other.......................... 3,019 2,751 2,496 45.0

Total Personal Insurance....................... $ 6 ,711 $ 6 ,228 $5,929 100.0 %