The Hartford 2009 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2009 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

|

|

41

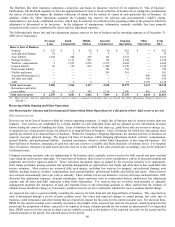

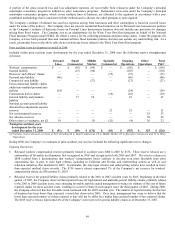

In addition to the expected loss ratio, the actuarial techniques or methods used primarily include paid and reported loss development and

frequency / severity techniques as well as the Bornhuetter-Ferguson method (a combination of the expected loss ratio and paid

development or reported development method). Within any one line of business, the methods that are given more influence vary based

primarily on the maturity of the accident year, the mix of business and the particular internal and external influences impacting the

claims experience or the methods. The output of the reserve reviews are reserve estimates that are referred to herein as the “actuarial

indication”.

Provided below is a general discussion of which methods are preferred by line of business. Because the actuarial estimates are

generated at a much finer level of detail than line of business (e.g., by distribution channel, coverage, accident period), this description

should not be assumed to apply to each coverage and accident year within a line of business. Also, as circumstances change, the

methods that are given more influence will change.

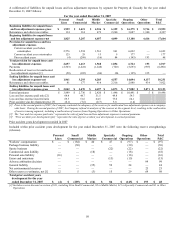

Property and Auto Physical Damage. These lines are fast-developing and paid and reported development techniques are used as these

methods use historical data to develop paid and reported loss development patterns, which are then applied to current paid and reported

losses by accident period to estimate ultimate losses. The Company relies primarily on reported development techniques although a

review of frequency and severity and the initial loss expectation based on the expected loss ratio is used for the most immature accident

months. The advantage of frequency / severity techniques is that frequency estimates are generally easier to predict and external

information can be used to supplement internal data in making severity estimates.

Auto Liability – Personal Lines. For auto liability, and bodily injury in particular, the Company performs a greater number of

techniques than it does for property and auto physical damage. In addition, because the paid development technique is affected by

changes in claim closure patterns and the reported development method is affected by changes in case reserving practices, the Company

uses Berquist-Sherman techniques which adjust these patterns to reflect current settlement rates and case reserving techniques. The

Company generally uses the reported development method for older accident years as a higher percentage of ultimate losses are

reflected in reported losses than in cumulative paid losses and the frequency/severity and Berquist-Sherman methods for more recent

accident years. Recent periods are influenced by changes in case reserve practices and changing disposal rates; the frequency/severity

techniques are not affected as much by these changes and the Berquist-Sherman techniques specifically adjust for these changes.

Auto Liability – Commercial Lines and Short-Tailed General Liability. As with Personal Lines auto liability, the Company performs a

variety of techniques, including the paid and reported development methods and frequency / severity techniques. For older, more

mature accident years, management finds that reported development techniques are best. For more recent accident years, management

typically prefers frequency / severity techniques that make separate assumptions about loss activity above and below a selected capping

level.

Long-Tailed General Liability, Fidelity and Surety and Large Deductible Workers’ Compensation. For these long-tailed lines of

business, the Company generally relies on the expected loss ratio and reported development techniques. Management generally weights

these techniques together, relying more heavily on the expected loss ratio method at early ages of development and more on the reported

development method as an accident year matures.

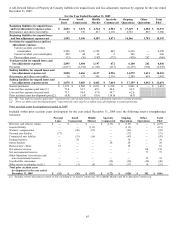

Workers’ Compensation. Workers’ compensation is the Company’ s single largest reserve line of business so a wide range of methods

are reviewed in the reserve analysis. Methods performed include paid and reported development, variations on expected loss ratio

methods, and an in-depth analysis on the largest states. Paid development patterns are historically very stable in the Company’ s

workers’ compensation business, so paid techniques are preferred for older accident periods. For more recent periods, paid techniques

are less predictive of the ultimate liability since such a low percentage of ultimate losses are paid in early periods of development.

Accordingly, for more recent accident periods, the Company generally relies more heavily on a state-by-state analysis and the expected

loss ratio approach.

Professional Liability. Reported and paid loss developments patterns for this line tend to be volatile. Therefore, the Company typically

relies on frequency and severity techniques.

Assumed Reinsurance and All Other within Other Operations. For these lines, management tends to rely on the reported development

techniques. In assumed reinsurance, assumptions are influenced by information gained from claim and underwriting audits.

Allocated Loss Adjustment Expenses (ALAE). For some lines of business (e.g., professional liability and assumed reinsurance), ALAE

and losses are analyzed together. For most lines of business, however, ALAE is analyzed separately, using paid development

techniques and an analysis of the relationship between ALAE and loss payments.

Unallocated Loss Adjustment Expense (ULAE). ULAE is analyzed separately from loss and ALAE. For most lines of business,

incurred ULAE costs to be paid in the future are projected based on an expected cost per claim year and the anticipated claim closure

pattern and the ratio of paid ULAE to paid loss.

The final step in the reserve review process involves a comprehensive review by senior reserving actuaries who apply their judgment

and, in concert with senior management, determine the appropriate level of reserves based on the information that has been

accumulated. Numerous factors are considered in this process including, but not limited to, the assessed reliability of key loss trends

and assumptions that may be significantly influencing the current actuarial indications, the maturity of the accident year, pertinent trends

observed over the recent past, the level of volatility within a particular line of business, and the improvement or deterioration of actuarial

indications in the current period as compared to the prior periods. Total recorded net reserves excluding asbestos and environmental

were 3.8% higher than the actuarial indication of the reserves as of December 31, 2009 and December 31, 2008.

See the Reserve Development Section for a discussion of changes to reserve estimates recorded in 2009.