The Hartford 2009 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2009 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

|

|

115

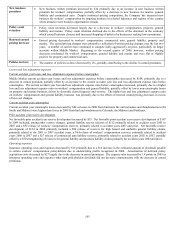

The Texas Windstorm Insurance Association (“TWIA”)

The Texas Windstorm Insurance Association provides hail and windstorm coverage to Texas residents of 14 counties along the Texas

Gulf coast who are unable to obtain insurance from other carriers. Insurance carriers who write property insurance in the state of Texas,

including The Hartford, are required to be members of TWIA and are obligated to pay assessments in the event that TWIA losses exceed

funds on hand, the available funds in the Texas Catastrophe Reserve Trust Fund (“CRTF”) and any available reinsurance. Assessments

are allocated to carriers based on their share of premium writings in the state of Texas, as defined.

During 2008, the board of directors of TWIA notified its member companies that it would assess them $430 to cover TWIA losses from

hurricane Ike. In the third quarter of 2008, the Company accrued a liability of $27 for its estimate of assessments it would ultimately get

from TWIA. In the first quarter of 2009, the Company reduced its estimated assessments by $14, from $27 to $13, resulting in a

reduction in insurance operating costs and expenses. The Company estimates that of the $13 of accrued assessments for Ike, it will

ultimately be able to recoup $8 through premium tax credits.

Florida Citizens Assessments

Citizens Property Insurance Corporation in Florida (“Citizens”) provides property insurance to Florida homeowners and businesses that

are unable to obtain insurance from other carriers, including for properties deemed to be “high risk”. Citizens maintains a Personal

Lines account, a Commercial Lines account and a High Risk account. If Citizens incurs a deficit in any of these accounts, Citizens may

impose a “regular assessment” on other insurance carriers in the state to fund the deficits, subject to certain restrictions and subject to

approval by the Florida Office of Insurance Regulation. Carriers are then permitted to surcharge policyholders to recover the

assessments over the next few years. Citizens may also opt to finance a portion of the deficits through issuing bonds and may impose

“emergency assessments” on other insurance carriers to fund the bond repayments. Unlike with regular assessments, however,

insurance carriers only serve as a collection agent for emergency assessments and are not required to remit surcharges for emergency

assessments to Citizens until they collect surcharges from policyholders. Under U.S. GAAP, the Company is required to accrue for

regular assessments in the period the assessments become probable and estimable and the obligating event has occurred. Surcharges to

recover the amount of regular assessments may not be recorded as an asset until the related premium is written. Emergency assessments

that may be levied by Citizens are not recorded in the income statement.

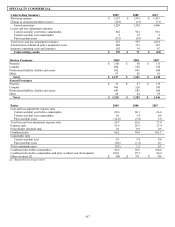

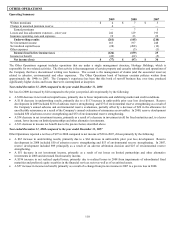

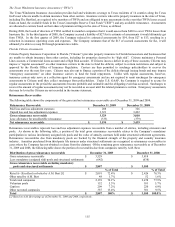

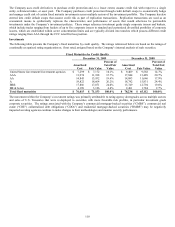

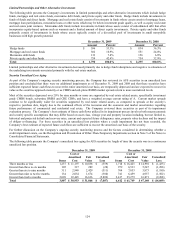

Reinsurance Recoverables

The following table shows the components of the gross and net reinsurance recoverable as of December 31, 2009 and 2008:

Reinsurance Recoverable December 31, 2009 December 31, 2008

Paid loss and loss adjustment expenses $ 208 $ 326

Unpaid loss and loss adjustment expenses 3,321 3,492

Gross reinsurance recoverable 3,529 3,818

Less: allowance for uncollectible reinsurance (335) (379)

Net reinsurance recoverable $ 3,194 $ 3,439

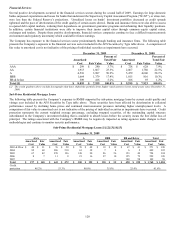

Reinsurance recoverables represent loss and loss adjustment expenses recoverable from a number of entities, including reinsurers and

pools. As shown in the following table, a portion of the total gross reinsurance recoverable relates to the Company’ s mandatory

participation in various involuntary assigned risk pools and the value of annuity contracts held under structured settlement agreements.

Reinsurance recoverables due from mandatory pools are backed by the financial strength of the property and casualty insurance

industry. Annuities purchased from third-party life insurers under structured settlements are recognized as reinsurance recoverables in

cases where the Company has not obtained a release from the claimant. Of the remaining gross reinsurance recoverable as of December

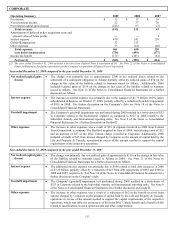

31, 2009 and 2008, the following table shows the portion of recoverables due from companies rated by A.M. Best.

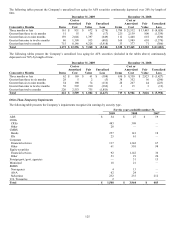

Distribution of gross reinsurance recoverable December 31, 2009 December 31, 2008

Gross reinsurance recoverable $ 3,529 $ 3,818

Less: mandatory (assigned risk) pools and structured settlements (642) (638)

Gross reinsurance recoverable excluding mandatory

pools and structured settlements $ 2,887

$3,180

% of Total % of Total

Rated A- (Excellent) or better by A.M. Best [1] $ 2,091 72.4% $ 2,426 76.3%

Other rated by A.M. Best 48 1.7% 52 1.6%

Total rated companies 2,139 74.1% 2,478 77.9%

Voluntary pools 152 5.3% 181 5.7%

Captives 209 7.2% 220 6.9%

Other not rated companies 387 13.4% 301 9.5%

Total $ 2,887 100% $ 3,180 100.0%

[1] Based on A.M. Best ratings as of December 31, 2009 and 2008, respectively.