The Hartford 2009 Annual Report Download - page 134

Download and view the complete annual report

Please find page 134 of the 2009 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

|

|

134

CAPITAL RESOURCES AND LIQUIDITY

Capital resources and liquidity represent the overall financial strength of The Hartford and the Life and Property & Casualty insurance

operations and their ability to generate cash flows from each of their business segments, borrow funds at competitive rates and raise new

capital to meet operating and growth needs over the next twelve months.

Liquidity Requirements and Sources of Capital

The Hartford Financial Services Group, Inc. (Holding Company)

The liquidity requirements of the holding company of The Hartford Financial Services Group, Inc. (“HFSG Holding Company”) have

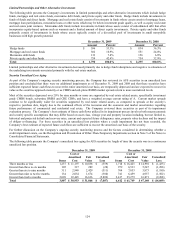

been and will continue to be met by HFSG Holding Company’ s fixed maturities, short-term investments, and cash of $2.2 billion at

December 31, 2009, dividends from the Life and Property & Casualty insurance operations, as well as the issuance of common stock,

debt or other capital securities and borrowings from its credit facilities. Expected liquidity requirements of the HFSG Holding Company

for the next twelve months include interest on debt of approximately $450, maturity of senior notes of $275, common stockholder

dividends, subject to the discretion of the Board of Directors, of approximately $80, and preferred stock dividends of approximately

$170.

Debt

HFSG Holding Company’ s debt maturities over the next twelve months include $275 aggregate principal amount of its 7.9% senior

notes that mature in June 2010. In addition, HLI has a capital lease obligation of $73, which was paid in January 2010. For additional

information regarding debt, see Notes 12 and 14 in the Notes to Consolidated Financial Statements.

Dividends

On February 18, 2010, The Hartford’ s Board of Directors declared a quarterly dividend of $0.05 per common share payable on April 1,

2010 to common shareholders of record as of March 1, 2010.

Pension Plans and Other Postretirement Benefits

While the Company has significant discretion in making voluntary contributions to the U. S. qualified defined benefit pension plan, the

Employee Retirement Income Security Act of 1974, as amended by the Pension Protection Act of 2006 and further amended by the

Worker, Retiree, and Employer Recovery Act of 2008, and Internal Revenue Code regulations mandate minimum contributions in

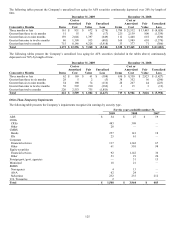

certain circumstances. The Company made contributions to its pension plans of $201, $2, and $158 in 2009, 2008 and 2007,

respectively, and contributions to its other postretirement plans of $46 in 2007. No contributions were made to the other postretirement

plans in 2009 and 2008. The Company’ s 2009 required minimum funding contribution was immaterial. The Company presently

anticipates contributing approximately $200 to its pension plans and other postretirement plans in 2010, based upon certain economic

and business assumptions. These assumptions include, but are not limited to, equity market performance, changes in interest rates and

the Company’ s other capital requirements. The Company does not have a required minimum funding contribution for the U.S. qualified

defined benefit pension plan for 2010 and the funding requirements for all of the pension plans is expected to be immaterial.

Dividends from Insurance Subsidiaries

Dividends to the HFSG Holding Company from its insurance subsidiaries are restricted. The payment of dividends by Connecticut-

domiciled insurers is limited under the insurance holding company laws of Connecticut. These laws require notice to and approval by

the state insurance commissioner for the declaration or payment of any dividend, which, together with other dividends or distributions

made within the preceding twelve months, exceeds the greater of (i) 10% of the insurer’ s policyholder surplus as of December 31 of the

preceding year or (ii) net income (or net gain from operations, if such company is a life insurance company) for the twelve-month period

ending on the thirty-first day of December last preceding, in each case determined under statutory insurance accounting principles. In

addition, if any dividend of a Connecticut-domiciled insurer exceeds the insurer’ s earned surplus, it requires the prior approval of the

Connecticut Insurance Commissioner. The insurance holding company laws of the other jurisdictions in which The Hartford’ s

insurance subsidiaries are incorporated (or deemed commercially domiciled) generally contain similar (although in certain instances

somewhat more restrictive) limitations on the payment of dividends. Dividends paid to HFSG Holding Company by its insurance

subsidiaries are further dependent on cash requirements of HLI and other factors. The Company’ s property-casualty insurance

subsidiaries are permitted to pay up to a maximum of approximately $1.4 billion in dividends to HFSG Holding Company in 2010

without prior approval from the applicable insurance commissioner. Statutory dividends from the Company’ s life insurance subsidiaries

in 2010 require prior approval from the applicable insurance commissioner. The aggregate of these amounts, net of amounts required by

HLI, is the maximum the insurance subsidiaries could pay to HFSG Holding Company in 2010. In 2009, HFSG Holding Company and

HLI received $700 in dividends from the life insurance subsidiaries representing the movement of a life subsidiary to HFSG Holding

Company, and HFSG Holding Company received $251 in dividends from its property-casualty insurance subsidiaries.

Other Sources of Capital for the HFSG Holding Company

The Hartford endeavors to maintain a capital structure that provides financial and operational flexibility to its insurance subsidiaries,

ratings that support its competitive position in the financial services marketplace (see the “Ratings” section below for further

discussion), and shareholder returns. As a result, the Company may from time to time raise capital from the issuance of stock, debt or

other capital securities and is continuously evaluating strategic opportunities. The issuance of common stock, debt or other capital

securities could result in the dilution of shareholder interests or reduced net income due to additional interest expense.