The Hartford 2009 Annual Report Download - page 191

Download and view the complete annual report

Please find page 191 of the 2009 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

|

|

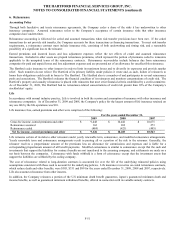

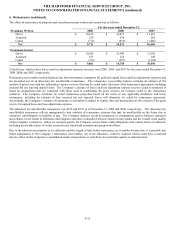

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued)

F-42

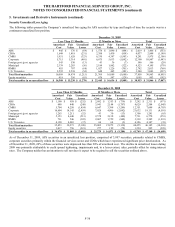

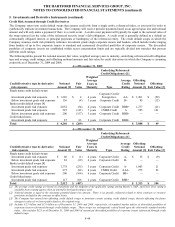

5. Investments and Derivative Instruments (continued)

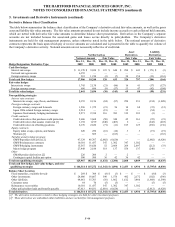

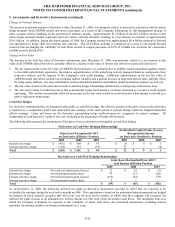

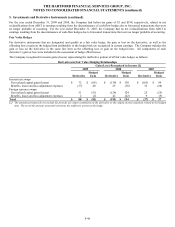

Non-qualifying strategies

Interest rate swaps, caps, floors, and futures

The Company uses interest rate swaps, caps, floors, and futures to manage duration between assets and liabilities in certain investment

portfolios. In addition, the Company enters into interest rate swaps to terminate existing swaps, thereby offsetting the changes in value

of the original swap. As of December 31, 2009 and 2008, the notional amount of interest rate swaps in offsetting relationships was $7.3

billion and $6.8 billion, respectively.

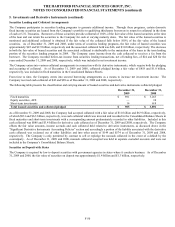

Foreign currency swap and forwards

The Company enters into foreign currency swaps and forwards to convert the foreign currency exposures to U.S. dollars in certain of its

foreign denominated fixed maturity investments. The Company also enters into foreign currency forward contracts that convert Euros

to Yen in order to economically hedge the foreign currency risk associated with certain assumed Japanese variable annuity products.

Japan 3Win related foreign currency swaps

During the first quarter of 2009, the Company entered into foreign currency swaps to hedge the foreign currency exposure related to the

Japan 3Win product guaranteed minimum income benefit (“GMIB”) fixed liability payments.

Japanese fixed annuity hedging instruments

The Company enters into currency rate swaps and forwards to mitigate the foreign currency exchange rate and Yen interest rate

exposures associated with the Yen denominated individual fixed annuity product.

Credit derivatives that purchase credit protection

Credit default swaps are used to purchase credit protection on an individual entity or referenced index to economically hedge against

default risk and credit-related changes in value on fixed maturity securities. These contracts require the Company to pay a periodic fee

in exchange for compensation from the counterparty should the referenced security issuers experience a credit event, as defined in the

contract.

Credit derivatives that assume credit risk

Credit default swaps are used to assume credit risk related to an individual entity, referenced index, or asset pool, as a part of replication

transactions. These contracts entitle the Company to receive a periodic fee in exchange for an obligation to compensate the derivative

counterparty should the referenced security issuers experience a credit event, as defined in the contract. The Company is also exposed

to credit risk due to embedded derivatives associated with credit linked notes.

Credit derivatives in offsetting positions

The Company enters into credit default swaps to terminate existing credit default swaps, thereby offsetting the changes in value of the

original swap going forward.

Equity index swaps, options, and futures

The Company offers certain equity indexed products, which may contain an embedded derivative that requires bifurcation. The

Company enters into S&P index swaps, futures and options to economically hedge the equity volatility risk associated with these

embedded derivatives. In addition, the Company is exposed to bifurcated options embedded in certain fixed maturity investments.

Warrants

During the fourth quarter of 2008, the Company issued warrants to purchase the Company's Series C Non-Voting Contingent

Convertible Preferred Stock, which were required to be accounted for as a derivative liability at December 31, 2008. For further

discussion of Allianz SE's investment in The Hartford, see Note 21. As of March 31, 2009, the warrants were no longer required to be

accounted for as derivatives and were reclassified to equity.

GMWB product derivatives

The Company offers certain variable annuity products with a GMWB rider in the U.S. and formerly in the U.K. and Japan. The GMWB

is a bifurcated embedded derivative that provides the policyholder with a GRB if the account value is reduced to zero through a

combination of market declines and withdrawals. The GRB is generally equal to premiums less withdrawals. Certain contract

provisions can increase the GRB at contractholder election or after the passage of time. The notional value of the embedded derivative

is the GRB balance.