The Hartford 2009 Annual Report Download

Download and view the complete annual report

Please find the complete 2009 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

|

|

1

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2009

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to ______________

Commission file number 001-13958

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

(Exact name of registrant as specified in its charter)

Delaware 13-3317783

(State or other jurisdiction of (I.R.S. Employer

incorporation or organization) Identification No.)

One Hartford Plaza, Hartford, Connecticut 06155

(Address of principal executive offices) (Zip Code)

(860) 547-5000

(Registrant’ s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: the following, all of which are listed on the New York Stock Exchange, Inc.

Common Stock, par value $0.01 per share

6.1% Notes due October 1, 2041

Securities registered pursuant to Section 12(g) of the Act:

7.9% Notes due June 15, 2010 5.375% Notes due March 15, 2017

5.25% Notes due October 15, 2011 6.3% Notes due March 15, 2018

4.625% Notes due July 15, 2013 6.0% Notes due January 15, 2019

4.75% Notes due March 1, 2014 5.95% Notes due October 15, 2036

7.3% Debentures due November 1, 2015 8.125% Junior Subordinated Debentures due June 15, 2068

5.5% Notes due October 15, 2016

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [X] No [ ]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934

during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing

requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File

required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to

the best of registrant’ s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any

amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company.

See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer [X] Accelerated filer [ ] Non-accelerated filer [ ] Smaller Reporting Company [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

The aggregate market value of the shares of Common Stock held by non-affiliates of the registrant as of June 30, 2009 was approximately $3.9 billion,

based on the closing price of $11.87 per share of the Common Stock on the New York Stock Exchange on June 30, 2009.

As of February 15, 2010, there were outstanding 384,128,538 shares of Common Stock, $0.01 par value per share, of the registrant.

Documents Incorporated by Reference

Portions of the registrant’ s definitive proxy statement for its 2010 annual meeting of shareholders are incorporated by reference in Part III of this Form

10-K.

Table of contents

-

Page 1

... One Hartford Plaza, Hartford, Connecticut 06155 (Address of principal executive offices) (Zip Code) (860) 547-5000 (Registrant' s telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: the following, all of which are listed on the New York Stock Exchange... -

Page 2

... Market Risk...Financial Statements and Supplementary Data...Changes in and Disagreements With Accountants on Accounting and Financial Disclosure...Controls and Procedures...Other Information...Part III Directors, Executive Officers and Corporate Governance of The Hartford...Executive Compensation... -

Page 3

... execution of steps to realign our business and reposition our investment portfolio, including the potential need to adjust our plans to take other restructuring actions, such as divestitures; market risks associated with our business, including changes in interest rates, credit spreads, equity... -

Page 4

... changes to statutory reserves and/or risk-based capital requirements related to secondary guarantees under universal life and variable annuity products; the Company' s ability to distribute its products through distribution channels, both current and future; the uncertain effects of emerging claim... -

Page 5

... assets under management, account values, fully insured ongoing premiums, life insurance in-force and net investment spread, see Part II, Item 7, MD&A, Key Performance Measures and Ratios and the respective segment discussions. Life provides investment products for approximately 7 million customers... -

Page 6

Life Principal Products Retail provides variable and fixed individual annuities with living and death benefit guarantees, mutual funds and 529 plans in the United States. In October 2009, the Company launched a new variable annuity product designed to meet customer needs for growth and income within... -

Page 7

... as investment performance, company credit ratings, perceived financial strength, product design, marketplace visibility, distribution capabilities, fees, credited rates, and customer service. In 2009, ratings agency downgrades, as well as changes in the Company' s strategic business model, limited... -

Page 8

...s individualized risk characteristics. Workers' compensation insurance accounts for the largest share of the written premium in the Middle Market segment. Small Commercial businesses generally represent companies with up to $5 in annual payroll, $15 in annual revenues or $15 in total property values... -

Page 9

Both Small Commercial and Middle Market provide insurance products and services through the Company' s home office located in Hartford, Connecticut, and multiple domestic regional office locations and insurance centers. The segments market their products nationwide utilizing brokers and independent ... -

Page 10

... from estimated net premiums to be received and with interest on such reserves compounded annually at certain assumed rates, are expected to be sufficient to meet Life' s policy obligations at their maturities or in the event of an insured' s disability or death. Other insurance liabilities include... -

Page 11

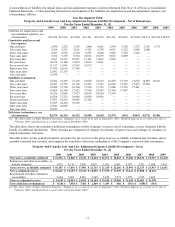

... to Consolidated Financial Statements. A table depicting the historical development of the liabilities for unpaid losses and loss adjustment expenses, net of reinsurance, follows. Loss Development Table Property And Casualty Loss And Loss Adjustment Expense Liability Development - Net of Reinsurance... -

Page 12

... mature claims in both general liability and workers' compensation. Reserve releases for accident year 2002 during calendar years 2003 and 2004 come largely from short-tail lines of business, where results emerge quickly and actual reported losses are predictive of ultimate losses. Reserve increases... -

Page 13

... Small Commercial package business claims as reported losses have emerged favorably to previous expectations. In 2007 through 2009, the Company released reserves for Middle Market general liability claims due to the favorable emergence of losses for high hazard and umbrella general liability claims... -

Page 14

... on investments; establishing premium rates; claim handling and trade practices; restrictions on the size of risks which may be insured under a single policy; deposits of securities for the benefit of policyholders; approval of policy forms; periodic examinations of the affairs of companies; annual... -

Page 15

... insurance products, as well as their profitability in some cases. Our results, financial condition and statutory capital remain sensitive to equity and credit market performance, and we expect that market volatility will continue to pressure returns in our life and property and casualty investment... -

Page 16

... capital losses. Due to the long-term nature of the liabilities associated with certain of our Life businesses, such as structured settlements and guaranteed benefits on variable annuities, sustained declines in long-term interest rates may subject us to reinvestment risks and increased hedging... -

Page 17

...and casualty companies. The RBC formula for life companies establishes capital requirements relating to insurance, business, asset and interest rate risks, including equity, interest rate and expense recovery risks associated with variable annuities and group annuities that contain death benefits or... -

Page 18

.... For securitized financial assets with contractual cash flows, the Company currently uses its best estimate of cash flows over the life of the security. In addition, estimating future cash flows involves incorporating information received from third-party sources and making internal assumptions and... -

Page 19

... natural resources; unfavorable changes in forecasted cash flows on mortgage-backed and asset-backed securities; for mortgage-backed and asset-backed securities, commercial and residential property value declines that vary by property type and location and average cumulative collateral loss rates... -

Page 20

...DAC and increase reserves for guaranteed minimum death and income benefits, which could have a material adverse effect on our results of operations and financial condition. The Company defers acquisition costs associated with the sales of its universal and variable life and variable annuity products... -

Page 21

... to pay premiums on our insurance policies or make deposits on our investment products. Our liquidity could be constrained by a catastrophe, or multiple catastrophes, which could result in extraordinary losses. In addition, in part because accounting rules do not permit insurers to reserve for... -

Page 22

..., securities firms, investment advisers, mutual funds, banks and other financial institutions. In recent years, there has been substantial consolidation and convergence among companies in the insurance and financial services industries resulting in increased competition from large, well-capitalized... -

Page 23

... a liability insurer defending or providing indemnity for third-party claims brought against insureds and as an insurer defending coverage claims brought against it. The Hartford accounts for such activity through the establishment of unpaid loss and loss adjustment expense reserves. The Company is... -

Page 24

... policies such that insurance premiums and future net investment income earned on premiums received will provide for an acceptable profit in excess of underwriting expenses and the cost of paying claims. State insurance departments that regulate us often propose premium rate changes for the benefit... -

Page 25

..., including, without limitation, providing insurance quotes, processing premium payments, making changes to existing policies, filing and paying claims, administering variable annuity products and mutual funds, providing customer support and managing our investment portfolios. Systems failures... -

Page 26

... infringed a third-party patent or other intellectual property rights, we could incur substantial liability, and in some circumstances could be enjoined from providing certain products or services to our customers or utilizing and benefiting from certain methods, processes, copyrights, trademarks... -

Page 27

... The Hartford' s insurance subsidiaries may extend credit, pay dividends or otherwise provide funds to The Hartford Financial Services Group, Inc. as discussed in Part II, Item 7, MD&A - Capital Resources and Liquidity - Liquidity Requirements and Sources of Capital. See Part III, Item 12, Security... -

Page 28

... Hartford' s annual percentage return and five-year total return on its common stock including reinvestment of dividends in comparison to the S&P 500 and the S&P Insurance Composite Index. Annual Return Percentage Company/Index The Hartford Financial Services Group, Inc. S&P 500 Index S&P Insurance... -

Page 29

...-for-sale and other Equity securities, trading Total net investment income (loss) Net realized capital gains (losses) [1] Other revenues Total revenues Benefits, losses and loss adjustment expenses Benefits, losses and loss adjustment expenses - returns credited on International variable annuities... -

Page 30

......Life Other...Personal Lines...Small Commercial...Middle Market...Specialty Commercial...Other Operations...Corporate...Property & Casualty Underwriting Risk Management Strategy...Investment Credit Risk...Capital Markets Risk Management...Capital Resources and Liquidity...Impact of New Accounting... -

Page 31

... [1] Includes investment income and mark-to-market effects of equity securities, trading, supporting the international variable annuity business, which are classified in net investment income with corresponding amounts credited to policyholders within benefits, losses and loss adjustment expenses... -

Page 32

... Plans International Institutional Other Total Life Property & Casualty Ongoing Operations Underwriting results Personal Lines Small Commercial Middle Market Specialty Commercial Ongoing Operations underwriting results Net servicing income [1] Net investment income Net realized capital losses... -

Page 33

... Company including payments from its separate account assets. The separate account foreign tax credit is estimated for the current year using information from the most recent filed return, adjusted for the change in the allocation of separate account investments to the international equity markets... -

Page 34

...on the GMWB hedging program, see the Life Equity Product Risk Management section within Capital Markets Risk Management. The Company' s fixed annuity sales have declined throughout 2009 as a result of lower interest rates and the transition to a new product. Management expects fixed annuity sales to... -

Page 35

... policies, while retaining less of the overall risk associated with individual insured lives. This new reinsurance structure will help balance the overall profitability of Individual Life' s business. The financial results of this change in the reinsurance structure will be recognized over time... -

Page 36

... Company' s core business model. Several lines - institutional mutual funds, private placement life insurance, income annuities and certain institutional annuities will continue to be managed for growth. The private placement life insurance industry (including the corporate-owned and bank-owned life... -

Page 37

...declines in 2009. Like in the Personal Lines and Small Commercial market segments, current economic conditions (lower payrolls, declines in production, lower sales, etc.) have reduced written premium growth opportunities in Middle Market. In 2010, management will seek to compete for new business and... -

Page 38

... liability lines renewed in July 2009 with a change in structure from primarily an excess of loss program to a variable quota share arrangement. This change was market driven and consistent with the Company' s expectations. This will have the impact of depressing the net written premium growth... -

Page 39

... change over time because of changes in internal company operations. Potential internal factors include (1) periodic changes in claims handling procedures, (2) growth in new lines of business where exposure and loss development patterns are not well established or (3) changes in the quality of risk... -

Page 40

... each individual claim and are adjusted as new information becomes known during the course of handling the claim. Lines of business for which loss data (e.g., paid losses and case reserves) emerge (i.e., is reported) over a long period of time are referred to as long-tail lines of business. Lines of... -

Page 41

...is that frequency estimates are generally easier to predict and external information can be used to supplement internal data in making severity estimates. Auto Liability - Personal Lines. For auto liability, and bodily injury in particular, the Company performs a greater number of techniques than it... -

Page 42

... to the new business. In both Small Commercial and Middle Market, workers' compensation is the Company' s single biggest line of business and the line of business with the longest pattern of loss emergence. Reserve estimates for workers' compensation are particularly sensitive to changes in medical... -

Page 43

... of similar claims, dismissal rates, allocated loss adjustment expense, and potential bankruptcy impact. Similarly, a ground-up exposure review approach is used to establish environmental reserves. The Company' s evaluation of its insureds' estimated liabilities for environmental claims involves... -

Page 44

... of management, based upon the known facts and current law, the reserves recorded for the Company' s property and casualty businesses at December 31, 2009 represent the Company' s best estimate of its ultimate liability for losses and loss adjustment expenses related to losses covered by policies... -

Page 45

... 31, 2009 Personal Small Middle Specialty Lines Commercial Market Commercial Beginning liabilities for unpaid losses and loss adjustment expenses-gross Reinsurance and other recoverables Beginning liabilities for unpaid losses and loss adjustment expenses-net Provision for unpaid losses and loss... -

Page 46

... Operations is recorded within the Specialty Commercial segment. Strengthened reserves for liability claims under Small Commercial package policies by $38 in 2009, primarily related to allocated loss adjustment expenses for accident years 2000 to 2005 and 2007 and 2008. During the first quarter... -

Page 47

...Personal Small Middle Specialty Ongoing Other Lines Commercial Market Commercial Operations Operations Gross incurred claim and claim adjustment expenses for current accident year catastrophes $ 260 Ceded claim and claim adjustment expenses 2 for current accident year catastrophes Net incurred claim... -

Page 48

... - Small Commercial $ (92) (15) - - - Middle Market $ (64) (90) - - (27) Specialty Commercial $ - - (75) - - Ongoing Operations $ (156) (105) (75) (46) (27) Other Operations Total P&C $ (156) (105) (75) (46) (27) Workers' compensation General liability Directors' and officers' claims Personal auto... -

Page 49

... net reserves for general liability claims as of December 31, 2007. Strengthened reserves for allocated loss adjustment expenses on national account general liability claims within Specialty Commercial by $25. Allocated loss adjustment expense reserves on general liability excess and umbrella claims... -

Page 50

... Other Operations 99 - 25 69 Total P&C $ (97) (30) (22) (18) (16) (15) 99 24 25 98 Workers' compensation Package business liability Surety business Commercial auto liability Personal auto liability Errors and omissions Adverse arbitration decision General liability Net environmental reserves Other... -

Page 51

... for Small Commercial workers' compensation claims as of December 31, 2006. Released reserves for Middle Market general liability claims related to the 2003 to 2006 accident years by $49. Beginning in the third quarter of 2007, the Company observed that reported losses for high hazard and umbrella... -

Page 52

.... Reported losses on general and products liability claims have been emerging unfavorably to previous expectations and loss adjustment expenses have been higher than expected on late emerging claims. The $34 reserve strengthening represented 3% of the Company' s net reserves for Specialty Commercial... -

Page 53

...) if the future annual claim payments were consistent with the calculated historical average. In the fourth quarters of 2009, 2008 and 2007, the Company completed evaluations of certain of its non-asbestos and non-environmental reserves, including its assumed reinsurance liabilities. Based on this... -

Page 54

... year gross survival ratio of 4.9. During the second quarters of 2009, 2008 and 2007, the Company completed its annual ground-up asbestos reserve evaluations. As part of these evaluations, the Company reviewed all of its open direct domestic insurance accounts exposed to asbestos liability, as well... -

Page 55

... of the reserve evaluation completed in the second quarter of 2009. [3] "All Time Paid" represents the total payments with respect to the indicated claim type that have already been made by the Company as of the indicated balance sheet date. "All Time Ultimate" represents the Company's estimate, as... -

Page 56

... limited to a relatively small percentage of a total contract placement. Claims are reported, via a broker, to the "lead" underwriter and, once agreed to, are presented to the following markets for concurrence. This reporting and claim agreement process makes estimating liabilities for this business... -

Page 57

... further discussion of the potential for variability in recorded loss reserves. Personal Lines Range of prior accident year unfavorable (favorable) development for the five years ended December 31, 2009 [1] Small Commercial Middle Market Specialty Ongoing Other Commercial Operations Operations Total... -

Page 58

... of Assets and Liabilities Associated with Variable Annuity and Other Universal Life-Type Contracts Estimated gross profits ("EGPs") are used in the amortization of: Life' s deferred policy acquisition cost ("DAC") asset, which includes the present value of future profits; sales inducement assets... -

Page 59

... impairment associated with the decision to suspend sales in the U.K. variable annuity business. For the year ended 2008: Death and Other Insurance Benefit Reserves[1] (75) - (3) (90) - (168) Segment After-tax (charge) benefit Retail Retirement Plans Individual Life International Corporate Total... -

Page 60

... base lapse rate assumption changes resulted in an approximate benefit of $40, after-tax, for U.S. variable annuities. Other-Than-Temporary Impairments and Valuation Allowances on Investments The Company has a monitoring process overseen by a committee of investment and accounting professionals... -

Page 61

... changed its estimate of the Credit Standing Adjustment to incorporate observable Company and reinsurer credit default spreads from capital markets, adjusted for market recoverability. Prior to the first quarter of 2009, the Company calculated the Credit Standing Adjustment by using default rates... -

Page 62

...As of December 31, 2008, the Company had goodwill allocated to the following reporting units: Other Retail Retirement Plans Institutional Solutions Group Individual Life Group Benefits Personal Lines Hartford Financial Products within Specialty Commercial Total Segment Goodwill $ 159 79 - 224 - 119... -

Page 63

... certain life and annuity deferred policy acquisition costs and reserve adjustments. The equity investments associated with the variable annuity products offered in Japan are recorded at fair value and are classified as "trading" with changes in fair value recorded in net investment income. Policy... -

Page 64

... 480 Short-term investments 6,846 3,511 - 10,357 Total $ 7,631 $ 61,785 $ 13,315 $ 82,731 % of Total 9.2% 74.7% 16.1% 100.0% [1] Represents securities for which adjustments were made to reduce prices received from third parties and certain private equity investments that are carried at the Company... -

Page 65

... directors providing for unfunded supplemental pension benefits. In addition, the Company provides certain health care and life insurance benefits for eligible retired employees. The Company maintains international plans which represent an immaterial percentage of total pension assets, liabilities... -

Page 66

... years, future taxable income and tax planning strategies that include holding debt securities with market value losses until recovery, selling appreciated securities to offset capital losses, and sales of certain corporate assets. Such tax planning strategies are viewed by management as prudent and... -

Page 67

..., insurance benefits provided, amortization of deferred policy acquisition costs, expenses related to selling and servicing the various products offered by the Company, dividends to policyholders, and other general business expenses. Life' s financial results in its variable annuity, mutual fund and... -

Page 68

...traditional insurance type products generally use a loss ratio which is expressed as the amount of benefits incurred during a particular period divided by total premiums and other considerations, as a key indicator of underwriting performance. Since Group Benefits occasionally buys a block of claims... -

Page 69

...parties and net realized capital gains and losses. Premiums charged for insurance coverages are earned principally on a pro rata basis over the terms of the related policies in-force. Service fees principally include revenues from third-party claims administration services provided by Specialty Risk... -

Page 70

Net income is a measure of profit or loss used in evaluating the performance of Total Property & Casualty and the Ongoing Operations and Other Operations segments. Within Ongoing Operations, the underwriting segments of Personal Lines, Small Commercial, Middle Market and Specialty Commercial are ... -

Page 71

... timing of expected claim settlements and the targeted returns set by management based on the competitive environment. The loss and loss adjustment expense ratio is affected by claim frequency and claim severity, particularly for shorter-tail property lines of business, where the emergence of claim... -

Page 72

...-tax profitability derived from underwriting activities, which are managed separately from the Company' s investing activities. Within Ongoing Operations, the underwriting segments of Personal Lines, Small Commercial, Middle Market and Specialty Commercial are evaluated by management primarily based... -

Page 73

KEY PERFORMANCE MEASURES AND RATIOS Life Management evaluates the rates of return various businesses can provide as an input in determining where additional capital should be invested to increase net income and shareholder returns. The Company uses the return on assets for the Individual Annuity, ... -

Page 74

... comprised of mutual fund assets and assets under management as opposed to traditional annuity contracts. Also contributing to the decrease was lower yields on fixed maturity investments and a decline in limited partnership and other alternative investment income, higher service and technology costs... -

Page 75

... Combined ratio Other Operations net income (loss) Year ended December 31, 2009 compared to the year ended December 31, 2008 Ongoing Operations earned premium growth Personal Lines Small Commercial Middle Market Earned premium grew 1% in 2009, primarily due to new business growth on both AARP and... -

Page 76

... as the effects of a lower loss and loss adjustment expense ratio for Small Commercial and Middle Market workers' compensation claims, lower claim frequency on Personal Lines auto claims and lower noncatastrophe losses on Small Commercial package business were partially offset by earned pricing... -

Page 77

...improved market performance of the underlying investment funds supporting the Japanese variable annuity product. Total net investment income, excluding equity securities, trading, decreased primarily due to lower income on fixed maturities resulting from a decline in average rates and fixed maturity... -

Page 78

... investment funds supporting the Japanese variable annuity product due to negative market performance year over year. Total net investment income, excluding equity securities, trading, decreased primarily due to lower income on limited partnerships and other alternative investments and fixed... -

Page 79

... credit risk due to credit spread tightening, as well as $140 from a change in spot rates related to transactional foreign currency predominately on the internal reinsurance of the Japan variable annuity business, which is offset in accumulated other comprehensive income (loss) ("AOCI"). Other, net... -

Page 80

...benefit) Net income (loss) [2] Assets Under Management Individual variable annuity account values Individual fixed annuity and other account values Other retail products account values Total account values [3] Retail mutual fund assets under management Other mutual fund assets under management Total... -

Page 81

... ratio was 43.3%. The 61.6% ratio in 2009 reflects lower EGPs driven by lower fee income due to declines in average account value and lower net investment income due to a greater percentage of fixed maturities being held in short-term investment and lower returns on investments in limited... -

Page 82

..., 2007 Net income decreased primarily as a result of increased realized capital losses, the impact of the 2008 Unlock charge, the impairment of goodwill attributed to the individual annuity line of business and the effect of equity market declines on variable annuity and mutual fund fee income. For... -

Page 83

INDIVIDUAL LIFE Operating Summary Fee income and other Earned premiums Net investment income Net realized capital losses Total revenues Benefits, losses and loss adjustment expenses Insurance operating costs and other expenses Amortization of deferred policy acquisition costs and present value of ... -

Page 84

... lower net realized capital losses. The following other factors contributed to the changes in net income: Fee income and other • Fee income and other increased primarily due to the impact of the 2009 Unlock "amortization of" unearned revenue reserves of $83 and increased cost of insurance charges... -

Page 85

... offset by growth in general account values. The decrease in net investment spread was attributable to lower limited partnership returns of 52 bps and lower fixed maturity income returns, partially offset by a reduction in the credited rate of 23 bps. Net realized capital losses increased primarily... -

Page 86

... products and services, including voluntary benefits, and group retiree health. The Company also offers disability underwriting, administration, claims processing services and reinsurance to other insurers and self-funded employer plans. Group Benefits has a block of financial institution business... -

Page 87

...Net realized capital losses Loss ratio Expense ratio Income tax expense (benefit Premiums and other considerations increased largely due to business growth driven by new sales and persistency over the last twelve months. Net investment income decreased primarily as a result of lower yields on fixed... -

Page 88

RETIREMENT PLANS Operating Summary Fee income and other $ Earned premiums Net investment income Net realized capital losses Total revenues Benefits, losses and loss adjustment expenses Insurance operating costs and other expenses Amortization of deferred policy acquisition costs and present value of... -

Page 89

... contributed to the changes in net loss: Fee income and other • Fee income and other decreased primarily due to lower average account values. Despite equity market improvements during the last nine months of 2009, account values have not returned to early 2008 levels. Net flows in group annuities... -

Page 90

INTERNATIONAL Operating Summary Fee income Earned premiums Net investment income Net realized capital gains (losses) Total revenues [1] Benefits, losses and loss adjustment expenses Insurance operating costs and other expenses Amortization of deferred policy acquisition costs Total benefits, losses ... -

Page 91

...' s average variable annuity account value. Average variable annuity account value declined due to net outflows driven by the suspension of new sales in the second quarter of 2009 as well as the effect of equity market declines in 2008 and the first quarter 2009. Benefits, losses and loss adjustment... -

Page 92

... Notes to Consolidated Financial Statements. The following other factors contributed to the changes in net income: Fee income • Fee income increased primarily due to growth in Japan' s variable annuity average assets under management. The increase in average assets under management over the prior... -

Page 93

... historically provided customized investment, insurance and income solutions to select markets through a broad range of products including PPLI owned by corporations and high net worth individuals, institutional annuities, mutual funds owned by institutional investors, structured settlements, stable... -

Page 94

... portfolios in the form of short-term investments and U.S. Treasuries, and 55 bps attributable to negative limited partnership returns. In both periods, the drop in variable rate yields was partially offset by lower credited rates on floating rate liabilities. Net realized capital losses were higher... -

Page 95

... of equity securities, trading, supporting the international variable annuity business, which are classified in net investment income with corresponding amounts credited to policyholders within benefits, losses and loss adjustment expenses. Life includes in Other its leveraged PPLI product line of... -

Page 96

... accident years Total losses and loss adjustment expenses Amortization of deferred policy acquisition costs Insurance operating costs and expenses Underwriting results Written Premiums Business Unit AARP Agency Other Total Product Line Automobile Homeowners Total Earned Premiums Business Unit AARP... -

Page 97

...• • AARP earned premiums grew $66 in 2009, reflecting an increase in new business written premium over the first nine months of 2009, driven by increased direct marketing spend, higher auto policy conversion rates and cross-selling homeowners' insurance to insureds who have auto policies. Agency... -

Page 98

... 2009. AARP new business written premium increased for both auto and home primarily due to increased direct marketing spend, higher auto policy conversion rates and cross-selling homeowners' insurance to insureds who have auto policies. Agency new business written premium increased for both auto and... -

Page 99

... to stop renewing Florida homeowners' policies sold through agents. Auto renewal earned pricing increases of 4% represent the portion of the 4% increase in renewal written pricing for 2008 that is reflected in earned premium. In 2008, the Company increased auto insurance rates in certain states... -

Page 100

... $16 release of reserves for loss and allocated loss and loss adjustment expenses on Personal Lines auto liability claims for accident years 2002 to 2006. Operating expenses Amortization of deferred policy acquisition costs increased by $16, driven primarily by the increase in earned premium and the... -

Page 101

... accident year catastrophes Prior accident years Total losses and loss adjustment expenses Amortization of deferred policy acquisition costs Insurance operating costs and expenses Underwriting results Premium Measures New business premium Policy count retention Renewal written pricing increase... -

Page 102

... classes of risks have contributed to the decrease in earned premiums in 2009. New business premium • New business written premium was up $36, or 8%, in 2009 primarily driven by an increase in workers' compensation business and the impact from the rollout of a new business owners policy product... -

Page 103

... use of lower pricing on targeted accounts and an increase in commissions paid to agents. New business written premium for workers' compensation was up modestly. Policy count retention decreased in all lines of business. Renewal earned pricing decreased for workers' compensation and commercial auto... -

Page 104

... combined ratio of 4.9 points. Earned premiums Earned premiums for the Middle Market segment decreased by $198 in 2009, primarily driven by decreases in general liability and commercial auto due to earned pricing decreases and the effect of non-renewals outpacing new business. Middle Market workers... -

Page 105

... Middle Market. Beginning in the second quarter of 2009, however, written pricing decreases moderated for workers' compensation, general liability and marine and were flat or slightly positive for property and commercial auto. The number of policies in-force decreased by 2%, partially contributing... -

Page 106

...in new business for general liability, marine and commercial auto. While continued price competition and the effect of some state-mandated rate reductions in workers' compensation has lessened the attractiveness of new business in certain lines and regions, the Company has increased new business for... -

Page 107

... policy acquisition costs Insurance operating costs and expenses Underwriting results Written Premiums Property Casualty Professional liability, fidelity and surety Other Total Earned Premiums Property Casualty Professional liability, fidelity and surety Other Total Ratios Loss and loss adjustment... -

Page 108

... premiums Earned premiums for the Specialty Commercial segment decreased by $154 due to decreases in all lines of business. • Property earned premiums decreased by $66 primarily due to the sale of the Company' s core excess and surplus lines property business. Effective March 31, 2009, the Company... -

Page 109

... higher loss and loss adjustment expense ratio for directors and officers insurance in professional liability, driven by earned pricing decreases, and a lower mix of property business which has a lower loss and loss adjustment ratio than other businesses within Specialty Commercial. Current accident... -

Page 110

... in unearned premium reserve Earned premiums Losses and loss adjustment expenses - prior year Insurance operating costs and expenses Underwriting results Net investment income Net realized capital losses Other expenses Income (loss) before income taxes Income tax benefit Net income (loss) $ 2009... -

Page 111

... Fee income Net investment income Net realized capital gains (losses) Total revenues Amortization of deferred policy acquisition costs and present value of future profits Interest expense Goodwill impairment Other expenses Total expenses Loss before income taxes Income tax benefit Net loss [1] 2009... -

Page 112

... products are used as part of the Company' s risk management strategy, including excess of loss occurrence-based products that protect property and workers' compensation exposures, and individual risk or quota share arrangements, that protect specific classes or lines of business. The Company... -

Page 113

... that a catastrophe loss exhausts limits on one or more layers under the treaties. In addition to the reinsurance protection provided by The Hartford' s traditional property catastrophe reinsurance program described above, the Company has fully collateralized reinsurance coverages from Foundation Re... -

Page 114

...to purchase insurance coverage, makes predicting long-term development of the terrorism risk market difficult, and that there is likely little potential for future market development for NBCR coverage. A December 2008 study by the U.S. Government Accountability Office ("GAO") found that property and... -

Page 115

... premium tax credits. Florida Citizens Assessments Citizens Property Insurance Corporation in Florida ("Citizens") provides property insurance to Florida homeowners and businesses that are unable to obtain insurance from other carriers, including for properties deemed to be "high risk". Citizens... -

Page 116

... effect on the Company' s consolidated results of operations or cash flows in a particular quarterly or annual period. Annually, the Company completes an evaluation of the reinsurance recoverable asset associated with older, long-term casualty liabilities reported in the Other Operations segment. As... -

Page 117

... credit default swaps to manage credit exposure. Credit default swaps involve a transfer of credit risk of one or many referenced entities from one party to another in exchange for periodic payments. The party that purchases credit protection will make periodic payments based on an agreed upon rate... -

Page 118

... asset pool. The Company purchases credit protection through credit default swaps to economically hedge and manage credit risk of certain fixed maturity investments across multiple sectors of the investment portfolio. The Company has also entered into credit default swaps that assume credit risk as... -

Page 119

... 31, 2009, 79% of these senior secured bank loan collateralized loan obligations ("CLOs") were rated AA and above with an average subordination of 29%. [2] Represents securities with pools of loans by the Small Business Administration whose issued loans are backed by the full faith and credit of the... -

Page 120

... the Federal Reserve' s projections. Unrealized losses on banks' investment portfolios decreased as credit spreads tightened and the pace of deterioration of the credit quality of certain assets slowed. Banks and insurance firms were also able to access re-opened debt capital markets, reducing their... -

Page 121

...any equity interest or property value in excess of outstanding debt. The ratings associated with the Company' s CMBS and CRE CDOs may be negatively impacted as rating agencies continue to make changes to their methodologies and monitor security performance. CMBS - Bonds [1] [2] December 31, 2009 AAA... -

Page 122

..., primarily from collateral maturities. The increase in the 2008 and 2009 vintage years represents reinvestment under these CRE CDOs. [4] The credit qualities above include downgrades that have shifted the portfolio from higher rated assets to lower rated assets since December 31, 2008. CMBS... -

Page 123

... were primarily comprised of general obligation securities. Certain of the Company' s municipal bonds were enhanced by third-party insurance for the payment of principal and interest in the event of an issuer default. Excluding the benefit of this insurance, the average credit rating was AA- and AA... -

Page 124

...-based options such as warrants and a limited amount of direct equity investments. Private equity and other funds primarily consist of investments in funds whose assets typically consist of a diversified pool of investments in small non-public businesses with high growth potential. December 31, 2009... -

Page 125

... the Company' s impairments recognized in earnings by security type. For the years ended December 31, 2009 2008 2007 54 $ 27 $ 19 483 28 257 25 137 61 92 53 - 18 4 62 232 2 1,508 398 - - - ABS CDOs CREs Other CMBS Bonds IOs Corporate Financial services Other Equity securities Financial services... -

Page 126

... after the securities were purchased. In general, larger liquidity premiums and wider credit spreads are the result of deterioration of the underlying collateral performance of the securities, as well as the risk premium required to reflect future uncertainty in the real estate market. Future... -

Page 127

... use of derivatives, see Note 5 of the Notes to Consolidated Financial Statements. Market Risk The Company is exposed to market risk, primarily relating to the market price and/or cash flow variability associated with changes in interest rates, credit spreads including issuer defaults, equity prices... -

Page 128

.... Rate increases are expected to provide additional net investment income, increase sales of fixed rate Life investment products, reduce the cost of the variable annuity hedging program, limit the potential risk of margin erosion due to minimum guaranteed crediting rates in certain Life products and... -

Page 129

... the equity method and generally lack sensitivity to interest rate changes. Separate account assets and liabilities, equity securities, trading and the corresponding liabilities associated with the variable annuity products sold in Japan are excluded from the analysis because gains and losses in... -

Page 130

... from invested assets. The Company' s primary exposure to equity risk relates to the potential for lower earnings associated with certain of the Life' s businesses such as variable annuities where fee income is earned based upon the fair value of the assets under management. During 2009, Life' s fee... -

Page 131

... products include variable annuity contracts, mutual funds, and variable life insurance. Generally, declines in equity markets will reduce the value of assets under management and the amount of fee income generated from those assets; reduce the value of equity securities, trading, for international... -

Page 132

... Company manages the equity market, interest rate and foreign currency exchange risks embedded in its products through product design, reinsurance, customized derivatives, and dynamic hedging and macro hedging programs. The Company recently launched a new variable annuity product with reduced equity... -

Page 133

... 4a of the Notes to Consolidated Financial Statements for description and impact of the Company' s credit spread and liability model assumption changes. Equity Risk Impact on Statutory Capital and Risk Based Capital See Statutory Surplus within the Capital Resources and Liquidity section of the MD... -

Page 134

... and liquidity represent the overall financial strength of The Hartford and the Life and Property & Casualty insurance operations and their ability to generate cash flows from each of their business segments, borrow funds at competitive rates and raise new capital to meet operating and growth needs... -

Page 135

... the second and third quarter of 2009 and could require further contributions of capital to FTB in the future. In addition, The Hartford has contributed $1.7 billion of the CPP funds to its indirect wholly-owned subsidiary Hartford Life Insurance Company and used $500 to purchase a surplus note from... -

Page 136

... its commercial paper program are $2.0 billion, the Company is dependent upon market conditions to access short-term financing through the issuance of commercial paper to investors. As of December 31, 2009, the Company has no commercial paper outstanding. The revolving credit facility provides for... -

Page 137

...' s short-term investments would be satisfied with current operating funds, including premiums received or through the sale of invested assets. A sale of invested assets could result in significant realized losses. Life Life' s total general account contractholder obligations are supported by Life... -

Page 138

... general account option for Retirement Plans' annuities and universal life contracts sold by Individual Life may be funded through operating cash flows of Life, available short-term investments, or Life may be required to sell fixed maturity investments to fund the surrender payment. Sales of fixed... -

Page 139

... Company, these include claim settlements with permanently disabled claimants. As of December 31, 2009, the total property and casualty reserves in the above table are gross of a reserve discount of $511. Estimated life, annuity and disability obligations include death and disability claims, policy... -

Page 140

... in investment in The Hartford by Allianz SE, increased transfers from the separate account to the general account for investment and universal life-type contracts and net issuances of long-term debt and consumer notes, offset by treasury stock acquired and dividends paid. Operating cash flows... -

Page 141

... Accident Insurance Company Hartford Life and Annuity Insurance Company Other Ratings: The Hartford Financial Services Group, Inc.: Senior debt Commercial paper Junior subordinated debentures Hartford Life, Inc.: Senior debt Hartford Life Insurance Company: Short term rating Consumer notes A.M. Best... -

Page 142

... securities and certain lower rated bonds required by the NAIC to be recorded at the lower of amortized cost or fair value. U.S. STAT for life insurance companies establishes a formula reserve for realized and unrealized losses due to default and equity risks associated with certain invested assets... -

Page 143

...capital and RBC ratios associated with changes in the equity markets. The Company also continues to explore other solutions for mitigating the capital market risk effect on surplus, such as internal and external reinsurance solutions, migrating towards a more statutory based hedging program, changes... -

Page 144

... on the insurance business. These proposals and initiatives include, or could include, new taxes or assessments on large financial institutions, changes pertaining to the income tax treatment of insurance companies and life insurance products and annuities, repeal or reform of the estate tax and... -

Page 145

... and operating effectiveness of internal control based on the assessed risk, and performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion. A company's internal control over financial reporting is a process... -

Page 146

... for personal lines operations and multi-line business development in the Caribbean. Mr. Andrade began his career as a presidential management intern and went on to work on national security and foreign policy issues within the executive branch and the Executive Office of The President. BETH... -

Page 147

...actuarial, risk management and Hartford Life's information technology area. In February 2006, she was named president of International Wealth Management and Group Benefits and from June 11, 2007 until May 1, 2008 she served as Executive Vice President of the Company and co-chief operating officer of... -

Page 148

... insurance agent who is an exclusive agent of the Company or who derives more than 50% of his or her annual income from the Company is eligible. Terms of options - Nonqualified stock options ("NQSOs") to purchase shares of common stock are available for grant under the PLANCO Plan. The administrator... -

Page 149

...Governance of the Company" and is incorporated herein by reference. Item 14. PRINCIPAL ACCOUNTING FEES AND SERVICES The information called for by Item 14 will be set forth in the Proxy Statement under the caption "Audit Committee Charter and Report Concerning Financial Matters - Fees to Independent... -

Page 150

THE HARTFORD FINANCIAL SERVICES GROUP, INC. INDEX TO CONSOLIDATED FINANCIAL STATEMENTS AND SCHEDULES Report of Independent Registered Public Accounting Firm...Consolidated Statements of Operations - For the Years Ended December 31, 2009, 2008 and 2007...Consolidated Balance Sheets - As of December ... -

Page 151

... audited the accompanying consolidated balance sheets of The Hartford Financial Services Group, Inc. and its subsidiaries (collectively, the "Company") as of December 31, 2009 and 2008, and the related consolidated statements of operations, changes in equity, comprehensive income (loss), and cash... -

Page 152

... FINANCIAL SERVICES GROUP, INC. Consolidated Statements of Operations (In millions, except for per share data) For the years ended December 31, 2009 2008 2007 Revenues Earned premiums Fee income Net investment income (loss): Securities available-for-sale and other Equity securities, trading Total... -

Page 153

... investments Cash Premiums receivable and agents' balances, net Reinsurance recoverables, net Deferred policy acquisition costs and present value of future profits Deferred income taxes, net Goodwill Property and equipment, net Other assets Separate account assets Total assets Liabilities Reserve... -

Page 154

... treasury stock Return of shares to treasury stock under incentive and stock compensation plans Balance at end of year Accumulated Other Comprehensive Loss, Net of Tax Balance at beginning of year Cumulative effect of accounting change, net of tax Total other comprehensive income (loss) Balance at... -

Page 155

...(loss) on securities Change in other-than-temporary impairment losses recognized in other comprehensive income (loss) Change in net gain (loss) on cash-flow hedging instruments Change in foreign currency translation adjustments Changes in pension and other postretirement plan adjustments Total other... -

Page 156

... and stock compensation plans and excess tax benefit Treasury stock acquired Dividends paid on preferred stock Dividends paid on common stock Changes in bank deposits and payments on bank advances Net cash provided by financing activities Foreign exchange rate effect on cash Net increase (decrease... -

Page 157

... of Presentation and Accounting Policies Basis of Presentation The Hartford Financial Services Group, Inc. is a financial holding company for a group of subsidiaries that provide investment products and life and property and casualty insurance to both individual and business customers in the United... -

Page 158

... December 31, 2009. The Company has investments in mutual funds, limited partnerships and other alternative investments including hedge funds, mortgage and real estate funds, mezzanine debt funds, and private equity and other funds which may be VIEs. The accounting for these investments will remain... -

Page 159

... Accounts Sales Inducements Reserve for Future Policy Benefits and Unpaid Losses and Loss Adjustment Expenses Contingencies Income Tax Pension Plans and Postretirement Healthcare and Life Insurance Benefit Plans Dividends to Policyholders Policyholder dividends are paid to certain life and property... -

Page 160

...Fee income for universal life-type contracts consists of policy charges for policy administration, cost of insurance charges and surrender charges assessed against policyholders' account balances and are recognized in the period in which services are provided. Unearned revenue reserves, representing... -

Page 161

... for the stock compensation plans include option exercise price payments, unamortized stock compensation expense and tax benefits realized in excess of the tax benefit recognized in net income. The difference between the number of shares assumed issued and number of shares purchased represents the... -

Page 162

... product line of business; corporate items not directly allocated to any of its reportable operating segments; intersegment eliminations and the mark-to-mark adjustment for the International variable annuity assets that are classified as equity securities, trading, reported in net investment income... -

Page 163

... and retention Personal Lines Small Commercial Middle Market Specialty Commercial Total Financial Measures and Other Segment Information One of the measures of profit or loss used by The Hartford' s management in evaluating the performance of its Life segments is net income. Net income is also... -

Page 164

THE HARTFORD FINANCIAL SERVICES GROUP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued) 3. Segment Information (continued) Revenues by Product Line Life Earned premiums, fees, and other considerations Retail Individual annuity: Individual variable annuity Fixed / MVA annuity Retail mutual... -

Page 165

... Information (continued) Revenues by Product Line (continued) Property & Casualty Ongoing Operations Earned premiums Personal Lines Automobile Homeowners Total Personal Lines Small Commercial Workers' Compensation Package Business Automobile Total Small Commercial Middle Market Workers' Compensation... -

Page 166

... [1] Total Life Property & Casualty Ongoing Operations Underwriting Results Personal Lines Small Commercial Middle Market Specialty Commercial Total Ongoing Operations underwriting results Net servicing income [2] Net investment income Net realized capital losses Other expenses Income before income... -

Page 167

...SERVICES GROUP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued) 3. Segment Information (continued) Income tax expense (benefit) Life Retail Individual Life Group Benefits Retirement Plans International Institutional Other Total Life Property & Casualty Ongoing Operations Other Operations... -

Page 168

...quoted prices for identical assets or liabilities in active markets that the Company has the ability to access at the measurement date. Level 1 securities include highly liquid U.S. Treasuries, money market funds and exchange traded equity, open-ended mutual funds reported in separate account assets... -

Page 169

...fixed maturities Equity securities, trading Equity securities, AFS Derivative assets [1] Short-term investments Separate account assets [2] Total assets accounted for at fair value on a recurring basis Liabilities accounted for at fair value on a recurring basis Other policyholder funds and benefits... -

Page 170

...Fixed maturities Equity securities, trading Equity securities, AFS Derivative assets [1] Short-term investments Separate account assets [2] Total assets accounted for at fair value on a recurring basis Liabilities accounted for at fair value on a recurring basis Other policyholder funds and benefits... -

Page 171

... limited to, current market inputs, such as credit loss assumptions, estimated prepayment speeds and market risk premiums. The Company has analyzed the third-party pricing services' valuation methodologies and related inputs, and has also evaluated the various types of securities in its investment... -

Page 172

... in mutual funds but also have investments in fixed maturity and equity securities. The separate account investments are valued in the same manner, and using the same pricing sources and inputs, as the fixed maturity, equity security, and short-term investments of the Company. Assets and Liabilities... -

Page 173

... market observable information and re-evaluation of the observability of pricing inputs primarily for certain long-dated corporate bonds and preferred stocks. [4] Derivative instruments are reported in this table on a net basis for asset/(liability) positions and reported in the Consolidated Balance... -

Page 174

... account liabilities, which results in a net zero impact on net income for the Company. [5] Transfers in and/or (out) of Level 3 are attributable to a change in the availability of market observable information for individual securities within the respective categories. [6] These amounts represent... -

Page 175

... on variable annuities, group accident and health and universal life insurance contracts, including corporate owned life insurance. [2] Included in short-term debt in the Consolidated Balance Sheets. As of December 31, 2009, The Hartford has no commercial paper outstanding. [3] Included in long-term... -

Page 176

... benefits International other guaranteed living benefits Variable annuity hedging derivatives Macro hedge program Total liabilities accounted for at fair value on a recurring basis $ $ 600 1,302 1,902 December 31, 2008 Quoted Prices in Active Significant Markets for Observable Identical Assets... -

Page 177

... in net realized capital gains and losses. The excess of fees collected from the contract holder over the Attributed Fees are associated with the host variable annuity contract and reported in fee income. U.S. GMWB Reinsurance Derivative The Company has reinsurance arrangements in place to transfer... -

Page 178

... and interest rate, currency and credit default swaps classified as Level 2. [4] Disclosure of changes in unrealized gains (losses) are not required for Levels 1 and 2. Information presented is for Level 3 only. [5] The variable annuity hedging derivatives and the macro hedge program derivatives are... -

Page 179

... interest rate, currency and credit default swaps classified as Level 2. [6] The variable annuity hedging derivatives and the macro hedge program derivatives are reported in this table on a net basis for asset/(liability) positions and reported on the consolidated balance sheet in other investments... -

Page 180

... life and annuity deferred policy acquisition costs and reserve adjustments. The equity investments associated with the variable annuity products offered in Japan are recorded at fair value and are classified as trading with changes in fair value recorded in net investment income. Policy loans... -

Page 181

...and 2007. Net investment income on equity securities, trading, includes dividend income and the changes in market value of the securities associated with the variable annuity products sold in Japan and the United Kingdom. The returns on these policyholder-directed investments inure to the benefit of... -

Page 182

... variability in cash flows of a forecasted transaction or of amounts to be received or paid related to a recognized asset or liability ("cash flow" hedge), (3) a hedge of a net investment in a foreign operation ("net investment" hedge) or (4) held for other investment and/or risk management purposes... -

Page 183

... as net realized capital gains and losses. Periodic derivative net coupon settlements are recorded in the line item of the consolidated statements of operations in which the cash flows of the hedged item are recorded. Other Investment and/or Risk Management Activities The Company' s other investment... -

Page 184

... Periodic net coupon settlements on credit derivatives/Japan Fair value measurement transition impact Results of variable annuity hedge program GMWB derivatives, net Macro hedge program Total results of variable annuity hedge program Other, net [2] Net realized capital losses adjustment for changes... -

Page 185

THE HARTFORD FINANCIAL SERVICES GROUP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued) 5. Investments and Derivative Instruments (continued) Sales of Available-for-Sale Securities 2009 Fixed maturities Sale proceeds Gross gains Gross losses Equity securities, AFS Sale proceeds Gross ... -

Page 186

... Chase & Co., Bank of America Corporation and Wells Fargo & Co. which each comprised less than 0.5% of total invested assets. As of December 31, 2008, the Company' s only exposure to any credit concentration risk of a single issuer greater than 10% of the Company' s stockholders' equity other than... -

Page 187

THE HARTFORD FINANCIAL SERVICES GROUP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued) 5. Investments and Derivative Instruments (continued) Security Unrealized Loss Aging The following tables present the Company' s unrealized loss aging for AFS securities by type and length of time the ... -

Page 188

...held at Federal Trust Corporation as of December 31, 2009. [2] Primarily represents multi-regional properties. Agricultural Industrial Lodging Multifamily Office Residential Retail Other Total mortgage loans Mortgage Loans by Property Type December 31, 2009 Carrying Percent of Value Total $ 596 10... -

Page 189

... capital loss and is the consolidated assets at cost net of liabilities. The CDO represents a cash flow CLO for which the Company provides collateral management services, earns a fee for those services and also holds investments in the debt issued by the CLO. Limited partnerships represent hedge... -

Page 190

... hedge funds, mortgage and real estate funds, mezzanine debt funds, and private equity and other funds (collectively, "limited partnerships"). These investments are accounted for under the equity method and the Company' s maximum exposure to loss as of December 31, 2009 is limited to the total... -

Page 191

... associated with the Yen denominated individual fixed annuity product. Credit derivatives that purchase credit protection Credit default swaps are used to purchase credit protection on an individual entity or referenced index to economically hedge against default risk and credit-related changes... -

Page 192

... at the current foreign spot exchange rate as of the reporting period date. Contingent capital facility put option The Company entered into a put option agreement that provides the Company the right to require a third-party trust to purchase, at any time, The Hartford' s junior subordinated notes in... -

Page 193

...annuity hedging instruments Credit contracts Credit derivatives that purchase credit protection Credit derivatives that assume credit risk [1] Credit derivatives in offsetting positions Equity contracts Equity index swaps, options, and futures Warrants [1] Variable annuity hedge program GMWB product... -

Page 194

... is based on the anticipated interest payments on hedged investments in fixed maturity securities that will occur over the next twelve months, at which time the Company will recognize the deferred net gains (losses) as an adjustment to interest income over the term of the investment cash flows... -

Page 195

... in Income [1] 2009 2008 2007 Hedged Hedged Hedged Derivative Derivative Derivative Item Item Item Interest rate swaps Net realized capital gains (losses) Benefits, losses and loss adjustment expenses Foreign currency swaps Net realized capital gains (losses) Benefits, losses and loss adjustment... -

Page 196

... that assume credit risk Equity contracts Equity index swaps, options, and futures Warrants Variable annuity hedge program GMWB product derivatives GMWB reinsurance contracts GMWB hedging instruments Macro hedge program Other GMAB product derivatives Contingent capital facility put option Total $ 31... -

Page 197

... underlying actively managed funds as compared to their respective indices, partially offset by gains in the fourth quarter related to liability model assumption updates for lapse rates. The net loss on credit default swaps was primarily due to losses on credit derivatives that assume credit risk as... -

Page 198

... SERVICES GROUP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued) 5. Investments and Derivative Instruments (continued) Credit Risk Assumed through Credit Derivatives The Company enters into credit default swaps that assume credit risk from a single entity, referenced index, or asset... -

Page 199

... to generate additional income. Through these programs, certain domestic fixed income securities are loaned from the Company' s portfolio to qualifying third-party borrowers in return for collateral in the form of cash or U.S. Treasuries. Borrowers of these securities provide collateral of 102... -

Page 200

THE HARTFORD FINANCIAL SERVICES GROUP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued) 6. Reinsurance Accounting Policy Through both facultative and treaty reinsurance agreements, the Company cedes a share of the risks it has underwritten to other insurance companies. Assumed reinsurance... -

Page 201

... the terms of the reinsurance agreements, including incurred but not reported unpaid losses. The Company' s estimate of losses and loss adjustment expense reserves ceded to reinsurers is based on assumptions that are consistent with those used in establishing the gross reserves for business ceded... -

Page 202

..., sales inducement assets ("SIA") and unearned revenue reserves ("URR"). Components of EGPs are used to determine reserves for universal life type contracts (including variable annuities) with death or other insurance benefits such as guaranteed minimum death, guaranteed minimum income and universal... -

Page 203

THE HARTFORD FINANCIAL SERVICES GROUP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued) 7. Deferred Policy Acquisition Costs and Present Value of Future Profits (continued) Results Changes in the DAC balance are as follows: Balance, January 1 Cumulative effect of accounting change, pre-... -

Page 204

... Individual Life Retirement Plans Total Life Property & Casualty Personal Lines Specialty Commercial Total Property & Casualty Corporate Total Goodwill $ 581 224 87 892 119 30 149 940 1,981 Gross 581 224 79 884 119 30 149 772 1,805 $ $ $ $ $ $ The Company's goodwill impairment test performed... -

Page 205

...right to market certain Property & Casualty insurance business to AARP members for the period January 1, 2007 to January 1, 2020. These costs were capitalized as an intangible asset and are being amortized over the thirteen year period the asset is expected to contribute to the Company' s cash flows... -

Page 206

...SERVICES GROUP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued) 9. Separate Accounts, Death Benefits and Other Insurance Benefit Features Accounting Policy The Company records the variable portion of individual variable annuities, 401(k), institutional, 403(b)/457, private placement life... -

Page 207

... HARTFORD FINANCIAL SERVICES GROUP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued) 9. Separate Accounts, Death Benefits and Other Insurance Benefit Features (continued) The following table summarizes GMDBs and GMIBs as of December 31, 2009: Individual Variable and Group Annuity Account... -

Page 208

THE HARTFORD FINANCIAL SERVICES GROUP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued) 10. Sales Inducements Accounting Policy The Company offers enhanced crediting rates or bonus payments to contract holders on certain of its individual and group annuity products. The expense associated... -

Page 209

... HARTFORD FINANCIAL SERVICES GROUP, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued) 11. Reserves for Future Policy Benefits and Unpaid Losses and Loss Adjustment Expenses (continued) Life Reserve Development Life' s reserve development resulting primarily from group disability products... -

Page 210

... FINANCIAL STATEMENTS (continued) 11. Reserves for Future Policy Benefits and Unpaid Losses and Loss Adjustment Expenses (continued) Property and Casualty Accounting Policy The Hartford establishes property and casualty reserves to provide for the estimated costs of paying claims under insurance... -

Page 211

... current law, the reserves recorded for The Hartford' s property and casualty businesses at December 31, 2009 represent the Company' s best estimate of its ultimate liability for losses and loss adjustment expenses related to losses covered by policies written by the Company. Based on information or... -

Page 212

... of claims or improper underwriting practices in connection with various kinds of insurance policies, such as personal and commercial automobile, property, life and inland marine; improper sales practices in connection with the sale of life insurance and other investment products; and improper fee... -

Page 213

... would have been had the customer had a more favorable credit report. The Company paid approximately $84.3 to eligible claimants and their counsel in connection with the settlement, and sought reimbursement from the Company' s Excess Professional Liability Insurance Program for the portion of the... -

Page 214

... cover asbestos and environmental claims. First, the Company wrote primary policies providing the first layer of coverage in an insured' s liability program. Second, the Company wrote excess policies providing higher layers of coverage for losses that exhaust the limits of underlying coverage. Third... -

Page 215

... and individual annuities used to fund structured settlements, and marketing and sale of individual and group variable annuity products and (ii) the previously disclosed investigation by the New York Attorney General' s Office of aspects of the Company' s variable annuity and mutual fund operations... -

Page 216

..., members of the funds are assessed to pay certain claims of the insolvent insurer. A particular state' s fund assesses its members based on their respective written premiums in the state for the classes of insurance in which the insolvent insurer was engaged. Assessments are generally limited for... -