Rogers 2013 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2013 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

MANAGEMENT’S DISCUSSION AND ANALYSIS

The March 6, 2013 termination is related to Debt Derivatives hedging

the US $350 million senior notes due 2038 (2038 Notes). The Debt

Derivatives that were terminated on March 6, 2013 were not

designated as effective hedges for accounting purposes and had an

original term of 10 years to August 15, 2018. The new Debt Derivatives

hedge the foreign exchange risk associated with the principal and

interest obligations on the 2038 Notes to their maturity at market rates

on the respective dates of the transactions and are designated as

effective hedges for accounting purposes.

The September 27, 2013 termination is related to Debt Derivatives

hedging senior notes scheduled to mature in 2014 and 2015. Only the

fixed foreign exchange rate was changed for the new Debt Derivatives.

All other terms are the same as the terminated Debt Derivatives they

replaced. Before the Debt Derivatives were terminated on

September 27, 2013, changes in their fair value were recorded in other

comprehensive income and were periodically reclassified to net income

to offset foreign exchange gains or losses on the related debt or to

modify interest expense to its hedged amount. On the termination date,

the balance in the hedging reserve related to these Debt Derivatives was

a $10 million loss. $1 million of this related to future periodic

exchanges of interest and will be recorded in net income over the

remaining life of the related debt securities. The remaining $8 million,

net of income taxes of $1 million, will remain in the hedging reserve

until such time as the related debt is settled.

Debt Derivatives Settled at Maturity

In June 2013, when we repaid and bought our US $350 million ($356

million) senior notes due 2013, the associated Debt Derivatives were

settled at maturity, resulting in total payments of approximately $104

million.

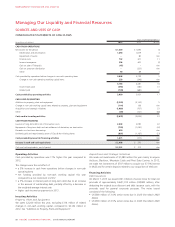

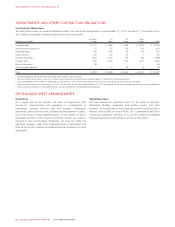

At December 31, 2013, we had US$6.4 billion of US dollar

denominated senior notes and debentures, all of which had been

hedged using Debt Derivatives.

(In millions of dollars) December 31, 2013 December 31, 2012

US dollar denominated long-term debt US$ 6,380 US$ 4,230

Hedged with Debt Derivatives US$ 6,380 US$ 4,230

Hedged exchange rate 1.0447 1.1340

Percent hedged 1100.0%100.0%

Amount of long-term debt at fixed rates 2

Total long-term debt Cdn$ 13,315 Cdn$ 11,447

Total long-term debt at fixed rates Cdn$ 13,315 Cdn$ 11,447

Percent of long-term debt fixed 100%100%

Weighted average interest rate on debt 5.5%6.1%

Weighted average term to maturity 311.3 Years 9.2 Years

1Pursuant to the requirements for hedge accounting under IAS 39, Financial

Instruments: Recognition and Measurement, on December 31, 2013, and

December 31, 2012, RCI accounted for 100%of its Debt Derivatives as hedges

against designated US dollar-denominated debt. As a result, on December 31, 2013,

100%of US dollar-denominated debt is hedged for accounting purposes compared to

100%on an economic basis.

2Long-term debt includes the effect of the Debt Derivatives.

3Weighted average term to maturity excludes US$1.1 billion senior notes due March

2014.

Expenditure Derivatives

We use foreign currency forward contracts (Expenditure Derivatives), to

hedge the foreign exchange risk on the notional amount of certain

forecasted expenditures. We use Expenditure Derivatives for risk-

management purposes only.

In 2013, we:

• entered into US$955 million of Expenditure Derivatives maturing

from April 2013 through December 2014 at an average rate of

$1.0341/US$1

• settled US$435 million of Expenditure Derivatives for $430 million

At December 31, 2013, we had US$900 million of Expenditure

Derivatives outstanding with terms to maturity ranging from January

2014 to December 2014 at an average rate of 1.0262/US$, all of which

have been designated as hedges for accounting purposes.

Equity Derivatives

We use stock-based compensation derivatives (Equity Derivatives), to

hedge the market price appreciation risk of the RCI Class B Non-Voting

shares granted under our stock-based compensation programs. We use

Equity Derivatives for risk-management purposes only.

In 2013 we entered into Equity Derivatives for 5.7 million RCI Class B

Non-Voting shares with a weighted average price of $50.37. These

Equity Derivatives have not been designated as hedges for accounting

purposes, so we record changes in their fair value as a stock-based

compensation expense and offset a portion of the impact of changes in

the market price of RCI Class B Non-Voting shares in the accrued value

of the stock-based compensation liability for our stock-based

compensation programs.

2013 ANNUAL REPORT ROGERS COMMUNICATIONS INC. 63