Rogers 2013 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2013 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

The Rogers First Rewards Credit Card program (operated through a

100% owned subsidiary of RCI) is regulated by the Office of the

Superintendent of Financial Institutions, which requires that a minimum

level of regulatory capital be maintained. Rogers is in compliance with

that requirement as at December 31, 2013. This program was launched

in the fourth quarter of 2013 and the capital requirements are not

material as at December 31, 2013.

With the exception of Rogers First Rewards Credit Card program, we

are not subject to externally imposed capital requirements. Our overall

strategy for capital risk management has not changed since

December 31, 2012.

NOTE 20: FINANCIAL RISK MANAGEMENT AND FINANCIAL

INSTRUMENTS

We are exposed to credit risk, liquidity risk and market risk. Our primary

risk management objective is to protect our income and cash flows and,

ultimately, shareholder value. We design and implement the risk

management strategies discussed below to ensure our risks and the related

exposures are consistent with our business objectives and risk tolerance.

Credit Risk

Credit risk represents the financial loss we could experience if a

counterparty to a financial instrument, in which we have an amount

owing from the counterparty, failed to meet its obligations under the

terms and conditions of its contracts with us.

Our credit risk is primarily attributable to our accounts receivable. Our

broad customer base limits the concentration of this risk. Our accounts

receivable in the consolidated statements of financial position are net of

allowances for doubtful accounts, which management estimates based

on prior experience and an assessment of the current economic

environment. Management uses estimates to determine the allowance

for doubtful accounts, taking into account factors such as our

experience in collections and write-offs, the number of days the

counterparty is past due and the status of the account. We believe that

our allowance for doubtful accounts sufficiently reflects the related

credit risk associated with our accounts receivable.

At December 31, 2013, we had accounts receivable of $1,509 million

(December 31, 2012 – $1,536 million), net of an allowance for doubtful

accounts of $104 million (December 31, 2012 – $119 million). At

December 31, 2013, $452 million (December 31, 2012 – $492 million)

of accounts receivable are considered past due, which is defined as

amounts outstanding beyond normal credit terms and conditions for

the respective customers.

We use various internal controls, such as credit checks, deposits on

account and billing in advance, to mitigate credit risk, and will suspend

services when customers have fully used their approved credit limits or

violated established payment terms. While our credit controls and

processes have been effective in managing credit risk, they cannot

eliminate credit risk and there can be no assurance that these controls

will continue to be effective or that our current credit loss experience

will continue.

Credit risk related to our Debt Derivatives, Expenditure Derivatives and

Equity Derivatives (Derivatives) arises from the possibility that the

counterparties to the agreements may default on their obligations. We

assess the creditworthiness of the counterparties to minimize the risk of

counterparty default, and do not require collateral or other security to

support the credit risk associated with these Derivatives. The entire

portfolio of our Derivatives is held by financial institutions with a

Standard & Poor’s rating (or the equivalent) ranging from A- to AA-.

Liquidity Risk

Liquidity risk is the risk that we will not be able to meet our financial

obligations as they fall due. We manage liquidity risk by managing our

commitments and maturities, capital structure and financial leverage, as

outlined in note 19. We also manage liquidity risk by continually

monitoring actual and projected cash flows to ensure that we will have

sufficient liquidity to meet our liabilities when due, under both normal

and stressed conditions, without incurring unacceptable losses or

risking damage to our reputation.

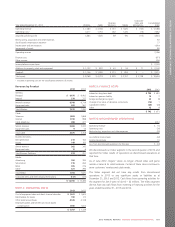

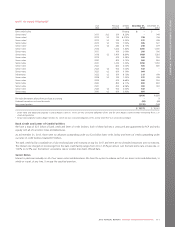

The tables below sets out the undiscounted contractual maturities of our financial liabilities and the receivable components of our derivatives at

December 31, 2013 and 2012.

December 31, 2013

Carrying

amount

Contractual

cash flows

Less than

1 year

1to3

years

4to5

years

More than

5 years

Short-term borrowings $ 6501$ 6501$ 6501$–$–$ –

Accounts payable and accrued liabilities 2,344 2,344 2,344 – – –

Long-term debt 13,343 13,436 1,170 1,883 1,989 8,394

Other long-term financial liabilities 38 38 – 14 18 6

Expenditure Derivative instruments:

Cash outflow (Canadian dollar) – 923 923 – – –

Cash inflow (Canadian dollar equivalent of US dollar) – (957) (957) – – –

Equity Derivative instruments – 13 13 – – –

Debt Derivative instruments:

Cash outflow (Canadian dollar) – 6,665 1,183 905 1,435 3,142

Cash inflow (Canadian dollar equivalent of US dollar) – (6,786)2(1,170)2(883)2(1,489)2(3,244)2

Net carrying amount of Derivatives (asset) (75)

$ 16,300 $ 16,326 $ 4,156 $ 1,919 $ 1,953 $ 8,298

1The terms of our accounts receivable securitization program are committed until it expires on December 31, 2015.

2Represents Canadian dollar equivalent amount of US dollar inflows matched to an equal amount of US dollar maturities in long-term debt for Debt Derivatives.

2013 ANNUAL REPORT ROGERS COMMUNICATIONS INC. 113