PNC Bank 2002 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2002 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

92

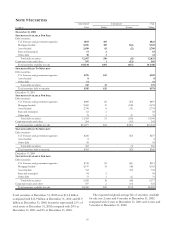

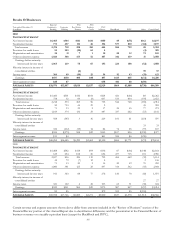

Fair Value Assumptions

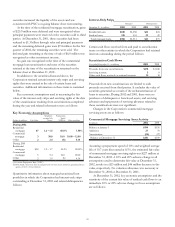

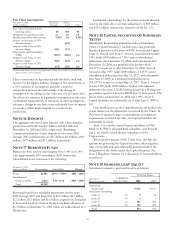

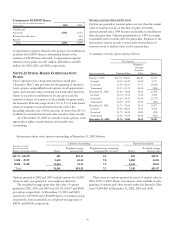

December 31, 2002

Dollars in millions

Residential

Mortgages

Student

Loans Other

Fair value of retained interest

(carrying value) $9 $65 $3

Weighted-average life (in years) 1.1 1.6 1.8

Residual cash flows discount rate 7.50% 3.6 4.14%

Impact on fair value of 10%

adverse change $(.9)

Impact on fair value of 20%

adverse change $(.1) (1.7)

Prepayment speed assumption

(CPR) 60.0% 20.8% (a)

Impact on fair value of 10%

adverse change $(.8) $(.8) (a)

Impact on fair value of 20%

adverse change (1.4) (1.6) (a)

(a) Historically, there have been no prepayments on these loans, which are guaranteed by an

agency of the U. S. Government.

These sensitivities are hypothetical and should be used with

caution. As the figures indicate, changes in fair value based on

a 10% variation in assumptions generally cannot be

extrapolated because the relationship of the change in

assumption to the change in fair value may not be linear. Also,

the effect of a variation in a particular assumption on fair value

is calculated independently of variations in other assumptions,

whereas a change in one factor may realistically have an impact

on another, which might magnify or counteract the

sensitivities.

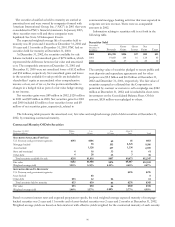

NOTE 16 DEPOSITS

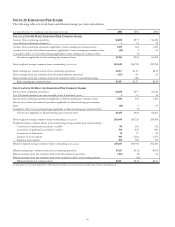

The aggregate amount of time deposits with a denomination

greater than $100,000 was $2.7 billion and $4.0 billion at

December 31, 2002 and 2001, respectively. Remaining

contractual maturities of time deposits for the years 2003

through 2007 and thereafter are $5.7 billion, $2.4 billion, $947

million, $473 million and $1.1 billion, respectively.

NOTE 17 BORROWED FUNDS

Bank notes have interest rates ranging from 1.46% to 6.14%

with approximately 60% maturing in 2003. Senior and

subordinated notes consisted of the following:

December 31, 2002

Dollars in millions Outstanding Stated Rate Maturity

Senior $2,546 1.93% – 7.00% 2003 – 2006

Subordinated

Nonconvertible 2,423 6.13 – 8.25 2003 – 2009

Total $4,969

Borrowed funds have scheduled repayments for the years

2003 through 2007 and thereafter of $3.1 billion, $2.1 billion,

$1.1 billion, $1.2 billion and $1.6 billion, respectively. Included

in borrowed funds are Federal Home Loan Bank advances of

$1.3 billion at December 31, 2002 which are collateralized by a

blanket lien.

Included in outstandings for the senior and subordinated

notes in the table above are basis adjustments of $93 million

and $212 million, respectively, related to SFAS No. 133.

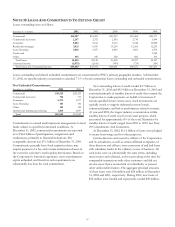

NOTE 18 CAPITAL SECURITIES OF SUBSIDIARY

TRUSTS

Mandatorily Redeemable Capital Securities of Subsidiary

Trusts (“Capital Securities”) include nonvoting preferred

beneficial interests in the assets of PNC Institutional Capital

Trust A, Trust B and Trust C. Trust A, formed in December

1996, holds $350 million of 7.95% junior subordinated

debentures, due December 15, 2026, and redeemable after

December 15, 2006, at a premium that declines from

103.975% to par on or after December 15, 2016. Trust B,

formed in May 1997, holds $300 million of 8.315% junior

subordinated debentures due May 15, 2027, and redeemable

after May 15, 2007, at a premium that declines from

104.1575% to par on or after May 15, 2017. Trust C, formed

in June 1998, holds $200 million of junior subordinated

debentures due June 1, 2028, bearing interest at a floating rate

per annum equal to 3-month LIBOR plus 57 basis points. The

rate in effect at December 31, 2002 was 1.99%. Trust C

Capital Securities are redeemable on or after June 1, 2008 at

par.

Cash distributions on the Capital Securities are made to the

extent interest on the debentures is received by the Trusts. In

the event of certain changes or amendments to regulatory

requirements or federal tax rules, the Capital Securities are

redeemable in whole.

Trust A is a wholly owned finance subsidiary of PNC

Bank, N.A., PNC’s principal bank subsidiary, and Trusts B

and C are wholly owned finance subsidiaries of the

Corporation.

The respective parents of the Trusts have, through the

agreements governing the Capital Securities, taken together,

fully, irrevocably and unconditionally guaranteed all of the

obligations of the Trusts under the Capital Securities. See

Note 3 Regulatory Matters for a discussion of certain dividend

restrictions.

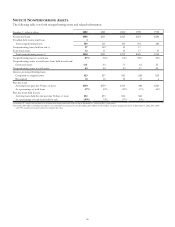

NOTE 19 SHAREHOLDERS’ EQUITY

Information related to preferred stock is as follows:

Preferred Shares

December 31

Shares in thousands

Liquidation

value per share 2002 2001

A

uthorized

$

1

p

ar value 17

,

135 17

,

172

Issued and outstanding

Series A 40 910

Series B 40 33

Series C 20 187 204

Series D 20 273 293

Total 472 510