PNC Bank 2002 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2002 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

42

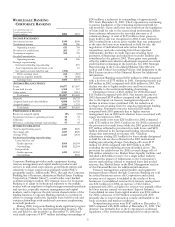

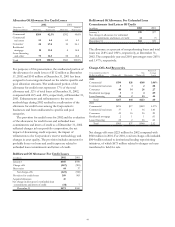

Nonperforming Assets By Type

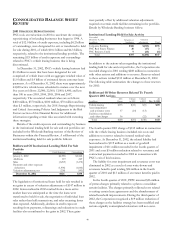

December 31 - dollars in millions 2002 2001

Nonaccrual loans

Commercial $226 $188

Lease financing 57 11

Consumer 11 3

Commercial real estate 74

Residential mortgage 75

Total nonaccrual loans 308 211

Troubled debt restructured 1

Total nonperforming loans 309 211

Nonperforming loans held for sale (a) 97 169

Foreclosed assets

Commercial real estate 1

Residential mortgage 63

Other 67

Total foreclosed assets 12 11

Total nonperforming assets $418 $391

Nonperforming loans to total loans .87% .56%

Nonperforming assets to total loans, loans held

for sale and foreclosed assets 1.13 .93

Nonperforming assets to total assets .63 .56

(a) Includes troubled debt restructured loans held for sale of $17 million and

$6 million as of December 31, 2002 and 2001, respectively.

Of the total nonperforming loans at December 31, 2002 and

2001, approximately 41% and 47%, respectively, are related to

PNC Business Credit. These loans are to borrowers that often

are highly leveraged, experiencing rapid growth, or have

elected to utilize asset-based financing. As a result, the risk

profile of these loans typically reflects a higher risk of default

and a greater proportion of such loans being classified as

nonperforming. Such loans are secured by accounts receivable,

inventory, machinery and equipment, and other collateral. This

secured position helps to mitigate risk of loss on these loans

by reducing the reliance on cash flows for repayment. The

above table excludes $40 million and $18 million of

nonperforming equity management assets carried at estimated

fair value at December 31, 2002 and December 31, 2001 and

included in other assets on the Consolidated Balance Sheet.

Nonperforming equity management assets at December 31,

2002 include $12 million of troubled debt restructured assets.

The amount of nonperforming loans that were current as

to principal and interest was $107 million at December 31,

2002 and $93 million at December 31, 2001. The amount of

nonperforming loans held for sale that were current as to

principal and interest was $46 million at December 31, 2002

and $8 million at December 31, 2001.

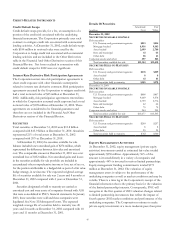

Nonperforming Assets By Business

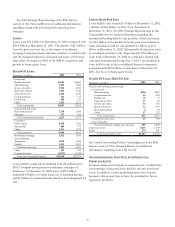

December 31 – in millions 2002 2001

Regional Community Banking $82 $52

Corporate Banking 187 220

PNC Real Estate Finance 2 6

PNC Business Credit 142 109

PNC Advisors 5 4

Total nonperforming assets $418 $391

At December 31, 2002, Corporate Banking and PNC Business

Credit had nonperforming loans held for sale of $83 million

and $14 million, respectively.

Change In Nonperforming Assets

In millions 2002 2001

January 1 $391 $372

Transferred from accrual 887 852

Returned to performing (30) (28)

Principal reductions (421) (278)

Asset sales (181) (27)

Charge-offs and other (228) (500)

December 31 $418 $391

Credit quality was adversely impacted in 2002 and continued

weakness or further weakening of the economy, or other

factors that affect asset quality, could result in an increase in

the number of delinquencies, bankruptcies or defaults, and a

higher level of nonperforming assets, net charge-offs and

provision for credit losses in future periods. See the Forward-

Looking Statements section of this Financial Review for

additional factors that could cause actual results to differ

materially from forward-looking statements or historical

performance.

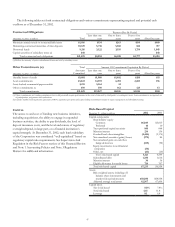

Accruing Loans And Loans Held For Sale Past Due 90

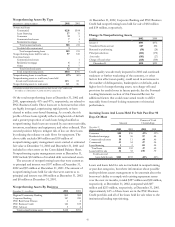

Days Or More

Amount

Percent of Total

Outstandings

December 31

Dollars in millions 2002 2001 2002 2001

Consumer $40 $36 .41% .39%

Residential mortgage 38 56 .97 .88

Commercial real estate 10 11 .44 .46

Commercial 41 54 .27 .36

Lease financing 12.02 .05

Total loans 130 159 .37 .42

Loans held for sale 32 33 1.99 .79

Total loans and

loans held for sale $162 $192 .44% .46%

Loans and loans held for sale not included in nonperforming

or past due categories, but where information about possible

credit problems causes management to be uncertain about the

borrower’s ability to comply with existing repayment terms

over the next six months, totaled $297 million and $38 million,

respectively, at December 31, 2002, compared with $87

million and $213 million, respectively, at December 31, 2001.

Approximately 44% of these loans are in the PNC Business

Credit portfolio and all of the loans held for sale relate to the

institutional lending repositioning.