PNC Bank 2002 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2002 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

87

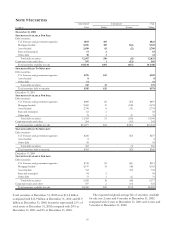

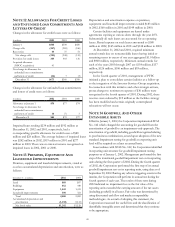

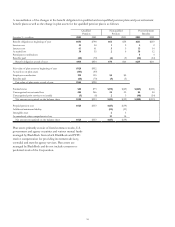

NOTE 10 LOANS AND COMMITMENTS TO EXTEND CREDIT

Loans outstanding were as follows:

December 31 - in millions 2002 2001 2000 1999 1998

Commercial $14,987 $15,205 $21,207 $21,468 $25,177

Commercial real estate 2,267 2,372 2,583 2,730 3,449

Consumer 9,854 9,164 9,133 9,348 10,980

Residential mortgage 3,921 6,395 13,264 12,506 12,253

Lease financing 5,081 5,557 4,845 3,663 2,978

Credit card 2,958

Other 415 445 568 682 392

T

otal loans 36,525 39,138 51,600 50,397 58,187

Unearned income (1,075) (1,164) (999) (724) (554)

Total loans, net of unearned income $35,450 $37,974 $50,601 $49,673 $57,633

Loans outstanding and related unfunded commitments are concentrated in PNC’s primary geographic markets. At December

31, 2002, no specific industry concentration exceeded 7.5 % of total commercial loans outstanding and unfunded commitments.

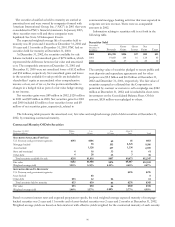

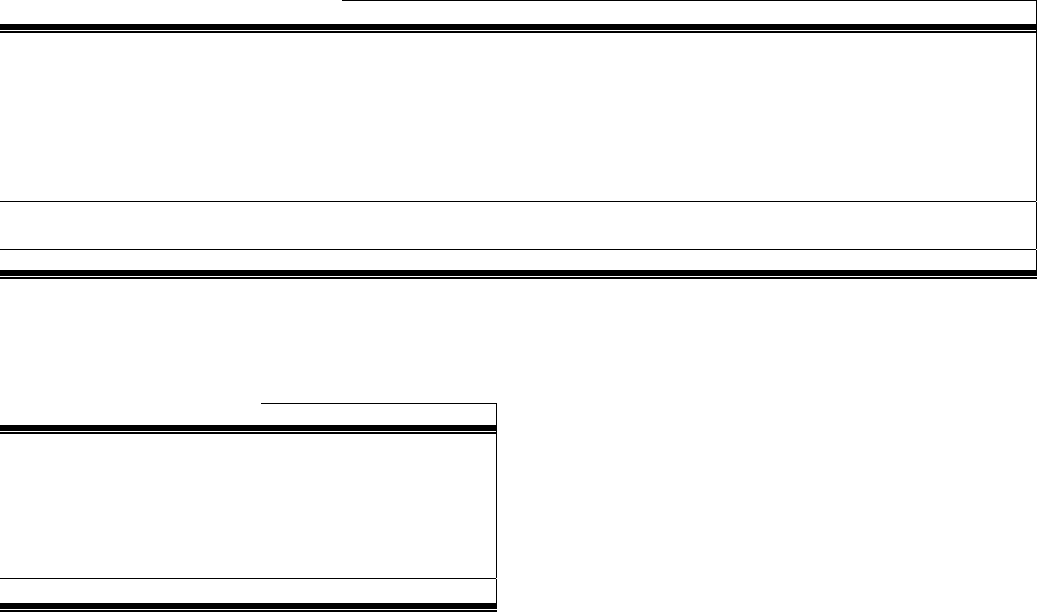

Net Unfunded Commitments

December 31 - in millions 2002 2001

Commercial $19,525 $20,233

Commercial real estate 718 711

Consumer 5,372 4,977

Lease financing 103 146

Other 125 139

Institutional lending repositioning 1,015 4,837

Total $26,858 $31,043

Commitments to extend credit represent arrangements to lend

funds subject to specified contractual conditions. At

December 31, 2002, commercial commitments are reported

net of $6.2 billion of participations, assignments and

syndications, primarily to financial institutions. The

comparable amount was $7.1 billion at December 31, 2001.

Commitments generally have fixed expiration dates, may

require payment of a fee, and contain termination clauses in

the event the customer’s credit quality deteriorates. Based on

the Corporation’s historical experience, most commitments

expire unfunded, and therefore cash requirements are

substantially less than the total commitment.

Net outstanding letters of credit totaled $3.7 billion at

December 31, 2002 and $4.0 billion at December 31, 2001 and

consisted primarily of standby letters of credit that commit the

Corporation to make payments on behalf of customers if

certain specified future events occur. Such instruments are

typically issued to support industrial revenue bonds,

commercial paper, and bid-or-performance related contracts.

At year-end 2002, the largest industry concentration within

standby letters of credit was for real estate projects, which

accounted for approximately 8% of the total. Maturities for

standby letters of credit ranged from 2003 to 2010. See Note

29 Commitments And Guarantees.

At December 31, 2002, $11.6 billion of loans were pledged

to secure borrowings and for other purposes.

Certain directors and executive officers of the Corporation

and its subsidiaries, as well as certain affiliated companies of

these directors and officers, were customers of and had loans

with subsidiary banks in the ordinary course of business. All

such loans were on substantially the same terms, including

interest rates and collateral, as those prevailing at the time for

comparable transactions with other customers and did not

involve more than a normal risk of collectibility or present

other unfavorable features. The aggregate principal amounts

of these loans were $18 million and $24 million at December

31, 2002 and 2001, respectively. During 2002, new loans of

$52 million were funded and repayments totaled $58 million.