PNC Bank 2002 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2002 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

32

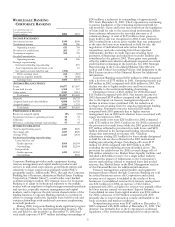

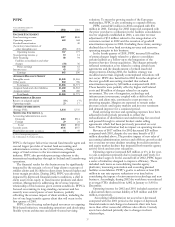

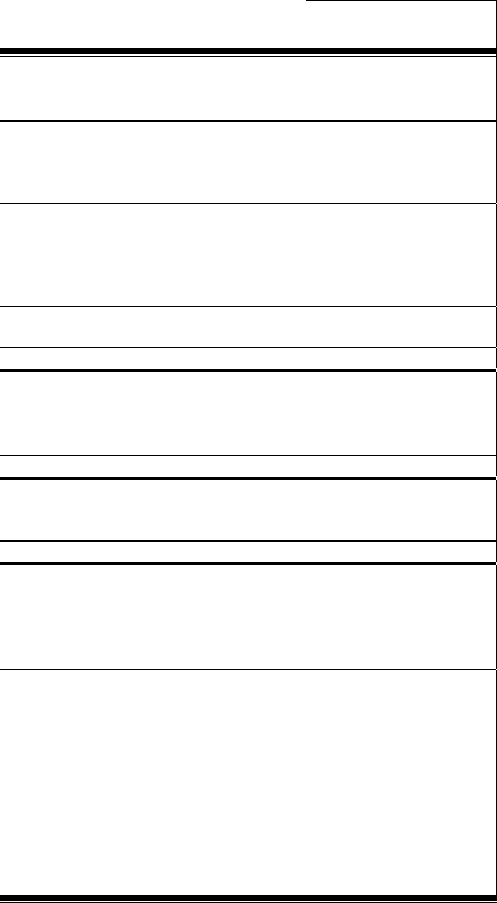

WHOLESALE BANKING

CORPORATE BANKING

Year ended December 31

Taxable-equivalent basis

Dollars in millions 2002 2001

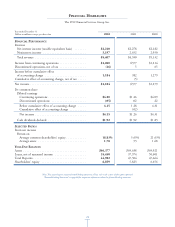

INCOME STATEMENT

Net interest income $349 $508

Noninterest income 282 256

Operating revenue 631 764

Provision for credit losses 203 57

Noninterest expense 359 378

Goodwill amortization 3

O

p

eratin

g

income 69 326

Strategic repositioning:

Institutional lending repositioning 891

Asset impairment and severance costs 16

Net (gains) on loans held for sale (155)

Pretax earnings (loss) 224 (581)

Income tax expense (benefit) 74 (206)

Earnings (loss) $150 $(375)

AVERAGE BALANCE SHEET

Loans $9,477 $13,907

Loans held for sale 1,369 367

Other assets 2,961 2,411

Total assets $13,807 $16,685

Deposits $4,683 $4,729

Assigned funds and other liabilities 8,088 10,705

Assigned capital 1,036 1,251

Total funds $13,807 $16,685

PERFORMANCE RATIOS

Return on assigned capital 14% (30)%

Noninterest income to operating revenue 45 34

Efficiency 46 71

Efficiency, excluding strategic repositioning 57 49

OTHER INFORMATION

Total nonperforming assets $187 $220

Net charge-offs $137 $209

Average FTEs 2,123 2,424

Institutional lending repositioning

Loans held for sale

Credit exposure $564 $4,594

Outstandings $245 $2,294

Exit portfolio

Credit exposure $413 $2,262

Outstandings $192

Corporate Banking provides credit, equipment leasing,

treasury management and capital markets products and

services to mid-sized corporations, government entities and

selectively to large corporations primarily within PNC’s

geographic region. Additionally, PNC, through the Corporate

Banking line of business, administers Market Street Funding

Corporation (“Market Street”), a multi-seller asset-backed

commercial paper conduit. The strategic focus for Corporate

Banking is to adapt its institutional expertise to the middle

market with an emphasis on higher-margin noncredit products

and services, especially treasury management and capital

markets, and to improve the risk/return characteristics of the

lending business. Corporate Banking intends to continue its

efforts to manage credit risk, liquidate loans held for sale and

sustain relationships with traditional customers emphasizing

noncredit products.

During 2002, Corporate Banking made significant progress

in the repositioning of its institutional lending business. The

exit and held for sale portfolios at December 31, 2002 had

total credit exposure of $977 million including outstandings of

$245 million, a reduction in outstandings of approximately

90% from December 31, 2001. The Corporation is continuing

to pursue liquidation of the remaining institutional held for

sale portfolio. Gains and losses may result from the liquidation

of loans held for sale to the extent actual performance differs

from estimates inherent in the recorded amounts or if

valuations change. A total of $155 million of net gains on

loans held for sale was recognized in 2002. Gains realized in

2002 resulted from a more active market than was anticipated

at the time the loans were transferred to held for sale, the

negotiation of individual loan sales rather than bulk

transactions, and sales occurring faster than expected.

Additionally, declines in credit exposure resulting from

payments, refinancings and reductions in credit facilities also

contributed to the gains in 2002. These gains were partially

offset by additional valuation adjustments required on certain

credit facilities remaining in the portfolio. See 2001 Strategic

Repositioning in the Consolidated Balance Sheet Review

section and Critical Accounting Policies And Judgments in the

Risk Factors section of this Financial Review for additional

information.

Corporate Banking earned $150 million in 2002 compared

with a net loss of $375 million in 2001. Operating income was

$69 million in 2002 compared with $326 million in 2001. The

decline was due to higher credit costs and lower revenue

attributable to the institutional lending downsizing.

Operating revenue of $631 million for 2002 decreased

$133 million compared with 2001. Net interest income for

2002 decreased $159 million compared with 2001 primarily

due to the impact on treasury management deposits of a

decline in interest rates combined with the reduction in

average loans resulting from the ongoing institutional lending

downsizing. Noninterest income increased $26 million

compared with 2001 primarily due to higher treasury

management fees in 2002 and valuation losses associated with

equity investments in 2001.

Total credit costs were $203 million for 2002 compared

with $733 million for 2001. Credit costs for 2002 consisted of

the provision for credit losses while the 2001 period included

$57 million reflected in provision for credit losses and $676

million reflected in the institutional lending repositioning

charge that represented net charge-offs. Valuation

adjustments totaling $215 million for loans already designated

as held for sale are also reflected in the 2001 institutional

lending repositioning charge. Net charge-offs were $137

million for 2002 compared with $209 million in 2001

excluding the repositioning amount described above. The

provision for credit losses for 2002 covered charge-offs of

$90 million related to two Market Street liquidity facilities and

included a $24 million reserve for a single airline industry

credit and the impact of refinements to the Corporation’s

reserve methodology related to impaired loans and pooled

reserves. See Market Street in the Risk Management section

of this Financial Review for additional information.

Treasury management, capital markets and equipment

leasing products offered through Corporate Banking are sold

by several businesses across the Corporation and related

revenue net of expense is included in the results of those

businesses. Consolidated revenue from treasury management

was $343 million for 2002, an increase of $12 million

compared with 2001, as higher fee revenue was partially offset

by lower income earned on customers’ deposit balances.

Consolidated revenue from capital markets was $104 million

for 2002, a decrease of $19 million compared with 2001

primarily due to lower transaction volume attributable to the

weak economic and market conditions.

Nonperforming assets were $187 million at December 31,

2002 compared with $220 million at December 31, 2001. The

decrease was primarily due to the Corporation’s continued

liquidation of the institutional lending held for sale portfolio.