Nokia 2011 Annual Report Download - page 232

Download and view the complete annual report

Please find page 232 of the 2011 Nokia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

|

|

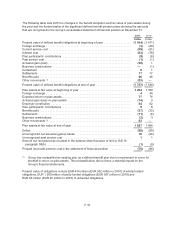

ownership and effective control have ceased, the amount of revenue can be measured reliably, it is

probable that economic benefits associated with the transaction will flow to the Group and the costs

incurred or to be incurred in respect of the transaction can be measured reliably. Sales could materially

change if management’s assessment of such criteria was determined to be inaccurate. The Group

enters into transactions involving multiple components consisting of any combination of hardware,

services and software. The consideration received from these transactions is allocated to each

separately identifiable component based on the relative fair value of each component. The

consideration allocated to each component is recognized as revenue when the revenue recognition

criteria for that component have been met. Determination of the fair value for each component requires

the use of estimates and judgment taking into consideration factors which may have a significant

impact on the timing and amount of revenue recognition. Examples of such factors include price when

the component is sold separately by the Group or the price when a similar component is sold

separately by the Group or a third party.

The Group makes price protection adjustments based on estimates of future price reductions and

certain agreed customer inventories at the date of the price adjustment. Potential changes in these

estimates could result in revisions to the sales in future periods.

Revenue from contracts involving solutions achieved through modification of complex

telecommunications equipment is recognized on the percentage of completion basis when the outcome

of the contract can be estimated reliably. Recognized revenues and profits are subject to revisions

during the project in the event that the assumptions regarding the overall project outcome are revised.

Current sales and profit estimates for projects may materially change due to the early stage of a long-

term project, new technology, changes in the project scope, changes in costs, changes in timing,

changes in customers’ plans, realization of penalties, and other corresponding factors, which may have

a significant impact on the timing and amount of revenue recognition.

Customer financing

The Group has provided a limited number of customer financing arrangements and agreed extended

payment terms with selected customers. Should actual financial position of the customers or general

economic conditions differ from assumptions, the ultimate collectability of such financings and trade

credits may be required to be re-assessed, which could result in a write-off of these balances and thus

negatively impact profits in future periods. From time to time the Group endeavors to mitigate this risk

through transfer of its rights to the cash collected from these arrangements to third party financial

institutions on a non-recourse basis in exchange for an upfront cash payment.

Allowances for doubtful accounts

The Group maintains allowances for doubtful accounts for estimated losses resulting from subsequent

inability of customers to make required payments. If the financial conditions of customers were to

deteriorate, resulting in an impairment of their ability to make payments, additional allowances may be

required in future periods.

Inventory-related allowances

The Group periodically reviews inventory for excess amounts, obsolescence and declines in net

realizable value below cost and records an allowance against the inventory balance for any such

declines. These reviews require management to estimate future demand for products. Possible

changes in these estimates could result in revisions to the valuation of inventory in future periods.

F-22