Nokia 2011 Annual Report Download - page 220

Download and view the complete annual report

Please find page 220 of the 2011 Nokia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

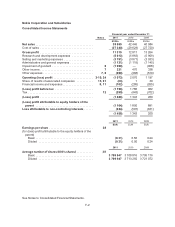

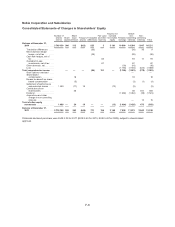

|

|

Principles of consolidation

The consolidated financial statements include the accounts of Nokia’s parent company (“Parent

Company”), and each of those companies over which the Group exercises control. Control over an

entity is presumed to exist when the Group owns, directly or indirectly through subsidiaries, over 50%

of the voting rights of the entity, the Group has the power to govern the operating and financial policies

of the entity through agreement or the Group has the power to appoint or remove the majority of the

members of the board of the entity.

The Group’s share of profits and losses of associates is included in the consolidated income statement

in accordance with the equity method of accounting. An associate is an entity over which the Group

exercises significant influence. Significant influence is generally presumed to exist when the Group

owns, directly or indirectly through subsidiaries, over 20% of the voting rights of the company.

All inter-company transactions are eliminated as part of the consolidation process. Profit or loss and

each component of other comprehensive income are attributed to the owners of the parent and to the

non-controlling interests. In the consolidated statement of financial position, non-controlling interests

are presented within equity, separately from the equity of the owners of the parent.

The entities or businesses acquired during the financial periods presented have been consolidated

from the date on which control of the net assets and operations was transferred to the Group. Similarly,

the result of a Group entity or business divested during an accounting period is included in the Group

accounts only to the date of disposal.

Business Combinations

The acquisition method of accounting is used to account for acquisitions of separate entities or

businesses by the Group. The consideration transferred in a business combination is measured as the

aggregate of the fair values of the assets transferred, liabilities incurred towards the former owners of

the acquired business and equity instruments issued. Acquisition-related costs are recognized as

expense in profit and loss in the periods when the costs are incurred and the related services are

received. Identifiable assets acquired and liabilities assumed by the Group are measured separately at

their fair value as of the acquisition date. Non-controlling interests in the acquired business are

measured separately based on their proportionate share of the identifiable net assets of the acquired

business. The excess of the cost of the acquisition over the interest in the fair value of the identifiable

net assets acquired and attributable to the owners of the parent, is recorded as goodwill.

Assessment of the recoverability of long-lived assets, intangible assets and goodwill

For the purposes of impairment testing, goodwill is allocated to cash-generating units that are expected

to benefit from the synergies of the acquisition in which the goodwill arose.

The Group assesses the carrying amount of goodwill annually or more frequently if events or changes

in circumstances indicate that such carrying amount may not be recoverable. The Group assesses the

carrying amount of identifiable intangible assets and long-lived assets if events or changes in

circumstances indicate that such carrying amount may not be recoverable. Factors that could trigger

an impairment review include significant underperformance relative to historical or projected future

results, significant changes in the manner of the use of the acquired assets or the strategy for the

overall business and significant negative industry or economic trends.

The Group conducts its impairment testing by determining the recoverable amount for the asset or

cash-generating unit. The recoverable amount of an asset or a cash-generating unit is the higher of its

F-10