Nokia 2011 Annual Report Download - page 132

Download and view the complete annual report

Please find page 132 of the 2011 Nokia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

|

|

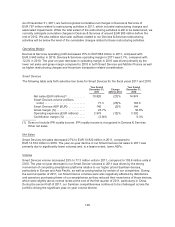

Volume

The following table sets forth our mobile device volumes and year-on-year growth rate by geographic

area for the fiscal years 2010 and 2009.

Year Ended

December 31,

2010

Change

2009 to 2010

Year Ended

December 31,

2009

(Units in millions, except percentage data)

Europe ........................... 112.7 5% 107.0

Middle East & Africa ................ 83.8 8% 77.6

Greater China ...................... 82.5 14% 72.6

Asia-Pacific ........................ 119.1 (4)% 123.5

North America ..................... 11.1 (18)% 13.5

Latin America ...................... 43.7 16% 37.6

Total ............................. 452.9 5% 431.8

Our 5% increase year-on-year in mobile device volumes was driven primarily by an improved demand

environment in 2010, partially offset by the intense competitive environment and shortages of certain

components in the second half of the year. During 2010, we gained device market share in Latin

America. Our device market share decreased in Asia-Pacific, Middle East & Africa, Europe and North

America. Our device market share was flat in Greater China.

Average Selling Price

Our mobile device ASP in 2010 was EUR 64, unchanged from 2009. During the first half of 2010, our

device ASP decreased primarily as a result of general price erosion across our mobile device portfolio

and a higher proportion of lower-priced smartphone sales, offset to some extent by the positive impact

of smartphones representing a higher proportion of our overall mobile device sales compared to 2009.

However, the decrease in our ASP during the first half of 2010 was offset by an increase in our ASP

during the second half of 2010. The increase in our ASP during the second half of 2010 was due

primarily to smartphones representing a higher proportion of our overall Devices & Services sales and

the appreciation of certain currencies against the euro. This increase was offset to some extent by

general price erosion driven by the intense competitive environment and a higher proportion of lower-

priced smartphone sales.

Gross Margin

Devices & Services gross profit decreased 5% to EUR 8 722 million, compared with EUR 9 227 million

in 2009, with a gross margin of 29.9%, compared to 33.1% in 2009. The gross margin decline was

primarily due to general price pressure and product material cost erosion being less than general

product price erosion, offset to some extent by smartphone volumes representing a higher proportion

of overall Devices & Services volumes. Additionally, the gross margin was negatively affected in 2010

by the overall appreciation of certain currencies against the euro and unfavorable foreign currency

hedging compared with 2009. During the first half of 2010, the gross margin was positively impacted by

the depreciation of certain currencies against the euro. However, this positive impact was more than

offset by the appreciation of certain currencies against the euro during the second half of 2010.

Further, during the first half of 2010, the gross margin was negatively affected by unfavorable foreign

currency hedging, which was partially offset by favorable foreign currency hedging impact during the

second half of 2010.

130