IBM 2009 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2009 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

Notes to Consolidated Financial Statements

INTERNATIONAL BUSINESS MACHINES CORPORATION AND SUBSIDIARY COMPANIES

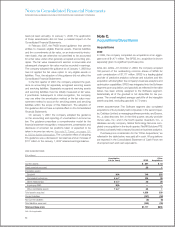

Pre-swap annual contractual maturities of long-term debt out-

standing at December 31, 2009, are as follows:

($ in millions)

2010 $ 2,251

2011 3,953

2012 3,096

2013 3,778

2014 1,516

2015 and beyond 9,414

Total $24,008

Debt Exchange

During the fourth quarter of 2009, the company completed an

exchange of approximately $500 million principal amount of

its 7.125 percent debentures due 2096, $123 million principal

amount of its 7 percent debentures due 2045 and $813 million

principal amount of its 8 percent notes due 2038, for approxi-

mately $1.5 billion of 5.60 percent senior notes due 2039 and

cash of approximately $376 million. The exchange was con-

ducted to retire high coupon long-dated debt in a favorable

interest rate environment.

The debt exchange was accounted for as a non-revolving

debt modification in accordance with U.S. GAAP and therefore

it did not result in any gain or loss recorded in the Consolidated

Statement of Earnings. Cash payments made will be amortized

over the life of the new debt. Upfront fees with third parties in

relation to the exchange were expensed as incurred.

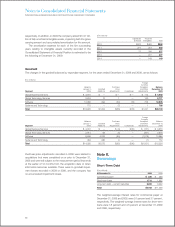

Interest on Debt

($ in millions)

For the year ended December 31: 2009 2008 2007

Cost of financing $ 706 $ 788 $ 811

Interest expense 404 687 753

Net investment derivative activity (1) (13) (142)

Interest capitalized 13 15 9

Total interest paid and accrued $1,122 $1,477 $1,431

Refer to the related discussion on page 124 in note V, “Seg ment

Infor mation,” for total interest expense of the Global Financing

segment. See note L, “Derivatives and Hedging Transactions,”

on pages 92 through 96 for a discussion of the use of currency

and interest rate swaps in the company’s debt risk manage-

ment program.

Lines of Credit

The company maintains a five-year, $10 billion Credit Agreement

(the “Credit Agreement”), which expires on June 28, 2012. The

total expense recorded by the company related to this facility

was $6.3 million in 2009, $6.2 million in 2008 and $6.2 million

in 2007. The amended Credit Agreement permits the company

and its Subsidiary Borrowers to borrow up to $10 billion on a

revolving basis. Borrowings of the Subsidiary Borrowers will be

unconditionally backed by the company. The company may also,

upon the agreement of either existing lenders, or of the additional

banks not currently party to the Credit Agreement, increase the

commitments under the Credit Agreement up to an additional

$2.0 billion. Subject to certain terms of the Credit Agreement,

the company and Subsidiary Borrowers may borrow, prepay

and reborrow amounts under the Credit Agreement at any time

during the Credit Agreement. Interest rates on borrowings under

the Credit Agreement will be based on prevailing market interest

rates, as further described in the Credit Agreement. The Credit

Agreement contains customary representations and warranties,

covenants, events of default, and indemnification provisions.

The company believes that circumstances that might give rise

to breach of these covenants or an event of default, as specified

in the Credit Agreement are remote. The company’s other lines

of credit, most of which are uncommitted, totaled approximately

$9,790 million and $11,031 million at December 31, 2009 and

2008, respectively. Interest rates and other terms of borrowing

under these lines of credit vary from country to country, depend-

ing on local market conditions.

($ in millions)

At December 31: 2009 2008

Unused lines:

From the committed global credit facility $ 9,910 $ 9,888

From other committed and uncommitted lines 7,405 8,376

Total unused lines of credit $17,314 $18,264

Note L.

Derivatives and Hedging Transactions

The company operates in multiple functional currencies and is

a significant lender and borrower in the global markets. In the

normal course of business, the company is exposed to the

impact of interest rate changes and foreign currency fluctua-

tions, and to a lesser extent equity changes and client credit

risk. The company limits these risks by following established

risk management policies and procedures, including the use of

derivatives, and, where cost effective, financing with debt in the

currencies in which assets are denominated. For interest rate

exposures, derivatives are used to better align rate movements

between the interest rates associated with the company’s lease

and other financial assets and the interest rates associated

with its financing debt. Derivatives are also used to manage the

related cost of debt. For foreign currency exposures, derivatives

are used to better manage the cash flow volatility arising from

foreign exchange rate fluctuations.

92