IBM 2009 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2009 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

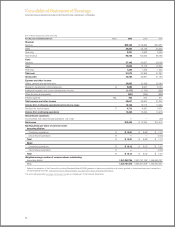

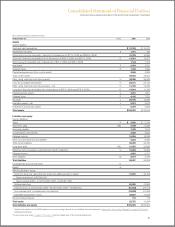

Notes to Consolidated Financial Statements

INTERNATIONAL BUSINESS MACHINES CORPORATION AND SUBSIDIARY COMPANIES

Note A.

Signicant Accounting Policies

Basis of Presentation

The accompanying Consolidated Financial Statements and foot-

notes thereto of the International Business Machines Corpor ation

(IBM and/or the company) have been prepared in accordance

with accounting principles generally accepted in the United States

of America (GAAP).

On December 31, 2002, the company sold its hard disk drive

(HDD) business to Hitachi, Ltd. (Hitachi). The HDD business was

accounted for as a discontinued operation and therefore, the

HDD results of operations and cash flows have been removed

from the company’s results of continuing operations and cash

flows for 2007. There was no activity in 2008 or 2009.

The company evaluated subsequent events through February

23, 2010, which is the date the financial statements were issued.

Within the financial tables presented, certain columns and

rows may not add due to the use of rounded numbers for dis-

closure purposes. Percentages presented are calculated from

the underlying whole-dollar amounts. Certain prior year amounts

have been reclassified to conform to the current year presenta-

tion. This is annotated where applicable.

Principles of Consolidation

The Consolidated Financial Statements include the accounts of

IBM and its controlled subsidiaries, which are generally major-

ity owned. The accounts of variable interest entities (VIEs) are

included in the Consolidated Financial Statements, if required.

Investments in business entities in which the company does not

have control, but has the ability to exercise significant influence

over operating and financial policies, are accounted for using

the equity method and the company’s proportionate share

of income or loss is recorded in other (income) and expense.

The accounting policy for other investments in equity securi-

ties is described on page 78 within “Marketable Securities.”

Equity investments in non-publicly traded entities are primarily

accounted for using the cost method. All intercompany transac-

tions and accounts have been eliminated in consolidation.

Use of Estimates

The preparation of financial statements in conformity with GAAP

requires management to make estimates and assumptions that

affect the amounts of assets, liabilities, revenue, costs, expenses

and other comprehensive income/(loss) that are reported in

the Consol idated Financial Statements and accompanying

disclosures. These estimates are based on management’s best

knowledge of current events, historical experience, actions that

the company may undertake in the future and on various other

assumptions that are believed to be reasonable under the cir-

cumstances. As a result, actual results may be different from

these estimates. See pages 52 to 54 for a discussion of the

company’s critical accounting estimates.

Revenue

The company recognizes revenue when it is realized or realiz-

able and earned. The company considers revenue realized or

realizable and earned when it has persuasive evidence of an

arrangement, delivery has occurred, the sales price is fixed or

determinable and collectibility is reasonably assured. Delivery

does not occur until products have been shipped or services

have been provided to the client, risk of loss has transferred to

the client, and either client acceptance has been obtained, client

acceptance provisions have lapsed, or the company has objec-

tive evidence that the criteria specified in the client acceptance

provisions have been satisfied. The sales price is not considered

to be fixed or determinable until all contingencies related to the

sale have been resolved.

The company recognizes revenue on sales to solution provid-

ers, resellers and distributors (herein referred to as “resellers”)

when the reseller has economic substance apart from the com-

pany, credit risk, title and risk of loss to the inventory, the fee to

the company is not contingent upon resale or payment by the end

user, the company has no further obligations related to bringing

about resale or delivery and all other revenue recognition criteria

have been met.

The company reduces revenue for estimated client returns,

stock rotation, price protection, rebates and other similar allow-

ances. (See Schedule II, “Valuation and Qualifying Accounts and

Reserves” included in the company’s Annual Report on Form

10-K). Revenue is recognized only if these estimates can be

reasonably and reliably determined. The company bases its esti-

mates on historical results taking into consideration the type of

client, the type of transaction and the specifics of each arrange-

ment. Payments made under cooperative marketing programs

are recognized as an expense only if the company receives from

the client an identifiable benefit sufficiently separable from the

product sale whose fair value can be reasonably and reliably

estimated. If the company does not receive an identifiable ben-

efit sufficiently separable from the product sale whose fair value

can be reasonably estimated, such payments are recorded as a

reduction of revenue.

Revenue from sales of third-party vendor products or ser-

vices is recorded net of costs when the company is acting as

an agent between the client and vendor and gross when the

company is a principal to the transaction. Several factors are

considered to determine whether the company is an agent or

principal, most notably whether the company is the primary

obligor to the client, or has inventory risk. Consideration is also

given to whether the company adds meaningful value to the

vendor’s product or service, was involved in the selection of the

vendor’s product or service, has latitude in establishing the sales

price or has credit risk.

70